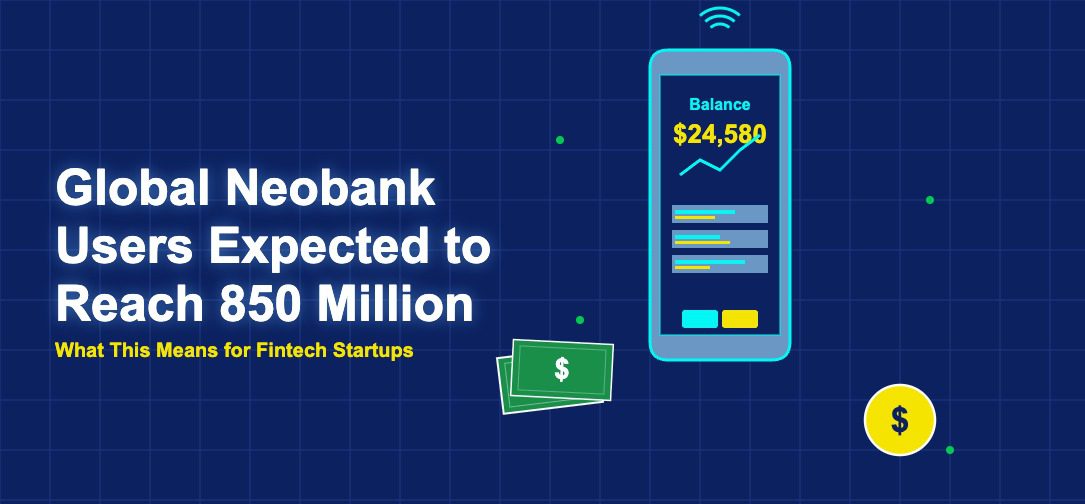

The Scale of Digital-Only Banking Adoption

Digital-only banks, commonly known as neobanks, are approaching a customer base of 850 million users worldwide. This figure, compiled from data reported by major neobanks and projected by industry analysts at firms including Statista and Simon-Kucher, reflects the rapid adoption of banking services delivered entirely through mobile applications without the physical branch infrastructure that defines traditional banking. The growth trajectory shows no signs of slowing, with neobank user numbers increasing by tens of millions annually across virtually every major market.

The 850 million figure encompasses users of both standalone neobanks like Revolut, Nubank, and Chime and digital banking services embedded within super-apps like Grab, GoTo, and WeChat. While the business models and regulatory structures vary considerably across these platforms, they share a common characteristic: banking services delivered digitally, designed for mobile devices, and offered at lower cost than traditional banking alternatives.

Latin America Leading Neobank User Growth

Latin America has become one of the most dynamic neobank markets globally, driven primarily by Nubank&’s extraordinary growth. The Brazilian neobank has attracted over 80 million customers across Brazil, Mexico, and Colombia, making it the largest digital bank outside of China by customer count. The company&’s success in converting a large unbanked and underbanked population to digital banking services has inspired numerous competitors and validated the neobank model in emerging markets.

The Boston Consulting Group projects fintech revenues will reach $1.5 trillion by 2030, with embedded finance and digital lending accounting for the largest share of projected growth.

According to CB Insights’ 2024 fintech report, global fintech funding declined 40 percent between 2022 and 2024, pushing the sector toward consolidation and a sharper focus on profitability over growth at all costs.

Beyond Nubank, companies like Ualá in Argentina, Neon in Brazil, and various regional players are building significant neobank businesses across Latin America. The region&’s combination of a large young population, widespread smartphone adoption, and frustration with expensive traditional banking creates conditions particularly favorable for digital banking growth.

European Neobanks Expanding Internationally

European neobanks have pursued aggressive international expansion strategies that have built customer bases spanning dozens of countries. Revolut, headquartered in London, has grown to serve over 35 million customers across Europe, the United Kingdom, and increasingly in markets beyond, including the United States, Australia, and Japan. N26, based in Berlin, serves millions of customers across European markets. Monzo, originally UK-focused, has expanded to the United States.

The European neobank model has benefited from regulatory frameworks, particularly the EU&’s banking passport system, that enable cross-border expansion within the single market. A banking license obtained in one EU member state allows the holder to offer services across all member states, reducing the regulatory overhead of multi-country expansion. This regulatory advantage has helped European neobanks build geographically diverse customer bases more quickly than neobanks in other regions.

Asia-Pacific Neobanks Serving Massive Populations

The Asia-Pacific region contributes the largest absolute number of neobank users, driven by the enormous populations of China, India, and Southeast Asia. In China, digital banking services embedded within platforms like WeChat and Alipay serve hundreds of millions of users, though these are more accurately described as super-app financial services than standalone neobanks. India&’s growing neobank sector, including platforms like Jupiter, Fi, and Niyo, serves a market where traditional banking leaves hundreds of millions underserved.

Southeast Asian markets have seen rapid neobank growth driven by both homegrown platforms and international entrants. Singapore, Hong Kong, and Malaysia have all issued digital banking licenses to new entrants, creating regulatory frameworks that support neobank development. Companies like Tonik in the Philippines, Bank Jago in Indonesia, and Trust Bank in Singapore are building customer bases in markets with significant financial inclusion gaps.

North American Neobanks in a Competitive Market

In North America, neobanks operate in a more competitive environment where traditional banks have invested heavily in their digital capabilities. Despite this competition, neobanks like Chime, Current, and Varo have attracted millions of customers, primarily by offering free checking accounts, early direct deposit access, and fee-free overdraft protection that appeal to consumers frustrated by traditional bank fee structures.

The North American neobank market is characterized by a focus on specific customer segments rather than mass-market approaches. Some neobanks target specific demographics like freelancers, teenagers, or immigrant communities. Others differentiate through specific features like automated savings tools, cryptocurrency integration, or financial wellness features. This segmentation strategy allows neobanks to build deep loyalty within their target demographics even when competing against well-resourced traditional banks.

Revenue Models Maturing

As neobank user numbers have grown, business models have evolved from customer acquisition-focused approaches to more diversified revenue strategies. Early neobanks often offered free services to attract users and relied on interchange revenue from debit card transactions as their primary income source. This model produced narrow margins and raised questions about long-term sustainability.

Mature neobanks have diversified into lending products, premium subscription tiers, insurance distribution, investment services, and business banking. Nubank now generates significant revenue from its credit card and personal lending products. Revolut offers premium subscription tiers with enhanced features. Chime has expanded into credit building products. This diversification is essential for neobanks to achieve the profitability that public market investors and long-term sustainability require.

Challenges on the Path to 850 Million

Reaching the 850 million user milestone is not without challenges. Customer engagement varies significantly across neobanks, with many users treating their neobank accounts as secondary to their primary bank relationships. Converting secondary account holders into primary banking customers who direct their salaries and main spending through the neobank remains one of the biggest challenges for the industry.

Profitability continues to be a concern for many neobanks. While some have achieved breakeven or profitability, many continue to operate at a loss as they invest in growth and product development. The path to profitability requires either achieving massive scale to make interchange-based models work or successfully cross-selling higher-margin products like loans and insurance to the existing user base.

Regulatory risk also remains relevant. Neobanks that operate through partnerships with licensed banks face the risk that regulatory scrutiny of these partnerships could restrict their operating models. Several jurisdictions have increased oversight of banking-as-a-service relationships, potentially affecting how some neobanks operate.

What 850 Million Users Means for Banking

The approach of 850 million neobank users represents a fundamental shift in global banking. It means that a significant and growing share of the world&’s population is choosing to conduct their banking through institutions that did not exist fifteen years ago. For traditional banks, this represents both a competitive threat and a signal about customer expectations. For regulators, it raises questions about systemic importance, deposit insurance, and consumer protection. And for consumers, it means more choice, lower costs, and better experiences than the banking industry has historically provided.

The 850 million figure will not be the end of the growth story. As smartphone penetration continues to increase, as neobanks expand into new markets, and as younger generations who are digital-native by default enter the banking market, the total number of neobank users will continue climbing. The question is no longer whether neobanks will become a significant part of the global banking landscape. They already are.