A Wells Fargo branch on a Tuesday afternoon in suburban Phoenix used to handle roughly eighty walk-in customers a day. Today the same branch averages sixteen. The customers did not stop banking. They moved into mobile apps that did not exist when the branch opened, and most of those apps now sit at fintechs that have only a partner bank’s charter in the background. The migration is more advanced than most US retail bankers admit publicly, and the numbers have started to tell a story the branch maps cannot.

What a US neobank actually is in 2026

The term neobank covers two distinct business models that get treated as one in popular coverage. The first is the BaaS-backed fintech: a company like Chime, Current, Step or Aspiration that holds no charter of its own and partners with a sponsor bank (Bancorp, Stride, Sutton, Cross River) for the underlying account. The second is the chartered digital bank: a company like Varo Money, SoFi, LendingClub or the increasingly digital Discover that holds a national or state banking charter directly.

The business mechanics are different. A BaaS-backed neobank pays a sponsor bank for the deposit infrastructure, shares interchange revenue with the sponsor, and operates inside the sponsor’s compliance perimeter. A chartered digital bank owns the deposits, captures the full margin and is directly regulated. The choice between the two models has been the most consequential strategic decision in US neobanking for the past five years.

The customer rarely sees this distinction. They open an account, get a card, deposit a paycheck, and pay bills through an app that looks roughly identical regardless of which model is underneath. The US payment rails the neobanks ride on are the same rails the incumbents use, which is why the customer experience converges even though the business models do not.

How big the US neobank shift has actually become

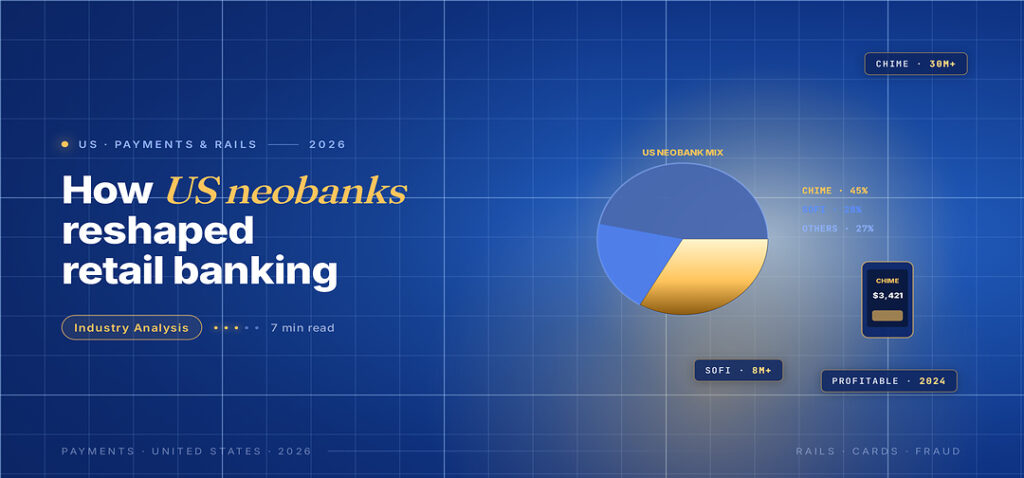

The headline numbers are now large enough to argue with. Chime, Current, Varo, SoFi and the rest of the named US neobanks collectively serve well over fifty million primary checking accounts. The Apple Card account base alone, run by Goldman, crossed twelve million in its peak before the partnership wound down. Cash App, which is not strictly a neobank but functions as one for a meaningful share of its users, runs north of fifty million monthly actives. Together, the digital-first US banking surface now reaches a customer count that is competitive with the largest incumbent retail banks.

The dollar deposits are more concentrated than the account counts suggest. The average BaaS-backed neobank account holds a few hundred dollars at any given time, often the most recent paycheck deposit cycle. The chartered digital banks (SoFi, Varo, Ally) hold balance distributions that look more like a regional bank. The interchange revenue per account, however, remains the dominant economic engine for the BaaS-backed cohort, which is why the CFPB’s posture on overdraft revenue and the OCC’s posture on partner-bank deposit fees have such a large impact on this end of the market.

The talent flow between incumbents and neobanks has reversed in the last two years. Senior risk, compliance and product hires now move more often from large US banks into neobanks than the other way. The salary deltas have narrowed enough that the equity story at a high-growth neobank is competitive. That talent migration is the strongest leading indicator of where US retail banking competence is concentrating.

A scoreboard for US neobank competitiveness in 2025

The composite figures below come from CFPB complaint data, FDIC call reports, sponsor-bank disclosures and individual neobank annual reports. They sketch where US neobanks sit on the metrics that actually determine retail banking outcomes.

The number that surprises most retail bankers is the share of US 18-to-29 primary checking relationships now held at a digital-first provider. The under-thirty cohort is past the tipping point, and the trend is now spreading into the 30-to-44 cohort. Retail banking executives at the largest US incumbents have started planning around this shift in their five-year deposit-growth assumptions. The ACH rails that move paychecks into neobank accounts are now where the deposit war is actually being fought.

Neobank fraud economics deserve a longer look than they usually get. The combination of frictionless account opening, real-time payment rails and high interchange concentration on debit cards has made the under-banked end of the neobank market a target for synthetic-identity fraud and check-kiting rings. The sponsor banks that have built the strongest fraud platforms (Cross River, Column, Lead Bank) charge a premium and tend to keep their fintech partners alive through the cycles. The sponsor banks that have skimped on fraud have produced most of the recent supervisory actions against the BaaS segment.

What incumbents have learned and what they still get wrong

Incumbent US banks have responded to the neobank shift with three patterns. The first is brand acquisitions: BBVA buying Simple before shutting it down, BMO acquiring Bank of the West, Capital One eventually absorbing Discover. The acquisitions have moved deposit balances but rarely transferred the cultural ability to ship product the way the neobanks do.

The second is internal digital builds: Marcus by Goldman, Liberty Bank Direct by US Bank, the Citi self-directed digital experience. These have produced real revenue but have struggled with the operational expense base of the parent company, which is why several have been quietly scaled back or absorbed.

The third is partnership and BaaS sponsorship from the incumbent side. A handful of large US banks have decided that if they cannot beat the neobank model, they should sponsor it. Cross River Bank, Sutton Bank, Stride Bank and the newer entrants (Lead Bank, Column, Synctera-backed sponsors) have built businesses out of this posture. The economic incentives are very different from a traditional retail bank and the talent profile is also different.

What incumbents still get wrong is the role of the mobile experience as the actual product. A bank that treats its app as a delivery channel for an underlying account loses customers to a fintech that treats the app as the product itself. The teams that have understood this distinction inside large US banks have generally been spun out, acquired or recruited away.

Customer service economics still favour incumbents on raw cost-per-call, but the gap has narrowed. Neobank support volume per active account is roughly half the incumbent volume, partly because the products are simpler and partly because the self-service in the app handles more issues. The neobanks that struggle on customer service have almost always tried to scale support too aggressively through chatbots before the underlying flows were stable.

What the next three years of US neobanking will look like

Three storylines will shape US neobanking through 2028. The first is sponsor-bank consolidation. The 2024 Synapse failure and the 2025 supervisory attention on partner-bank programmes have pushed sponsor banks to either invest seriously in compliance infrastructure or exit the business. The number of credible sponsor banks willing to take on new fintech programmes has contracted, which has slowed the launch pace of new BaaS-backed neobanks.

The second is the convergence between neobank and embedded finance. The same infrastructure that powers a Chime checking account also powers a Shopify Capital cash-advance product and a Toast restaurant capital line. The companies that own the underlying ledger and compliance plumbing capture the value as embedded finance grows, regardless of whether the front end is a consumer neobank or a vertical SaaS product.

The third is the international playbook. Several US neobanks have started shipping cross-border features (multi-currency accounts, remittance corridors, US accounts for global users) that put them in direct competition with Wise and Revolut. Banking innovation that scales globally is increasingly being shipped by US neobanks rather than only being received from European fintechs.

The customer migration that started in the mid-2010s is now mature enough that the question is no longer whether neobanks will reshape US retail banking. The question is which model (BaaS-backed, chartered, or hybrid) and which incumbents will adapt fast enough to remain relevant.

The Phoenix branch that handles sixteen customers a day still serves a real purpose. It just is not the front line of US retail banking competition anymore, and the operators who have internalised that shift are designing very different organisations than the ones that built the branch.

For underbanked and unbanked migration data referenced above, see the FDIC National Survey of Unbanked and Underbanked Households.