For most of the 2010s, the most expensive way to read a 10-K filing at a major US asset manager was to have a senior analyst do it personally. The cost was the analyst’s time. By 2026 that workflow has flipped. Most large US asset managers now run every freshly filed 10-K, 10-Q and 8-K through an internal natural language processing pipeline within minutes of the EDGAR drop, surface a structured summary, and only then escalate the document to a human. The change is not subtle. It has reordered how a meaningful share of US finance reads its own primary sources.

What NLP actually does inside US financial firms today

Natural language processing in US finance touches at least six work streams. The first is filings analysis, where models extract material changes, risk factors, related-party disclosures and management language sentiment from SEC and bank regulatory filings. The second is earnings call analysis, where transcripts are processed for tone shifts, guidance changes and named-entity-driven event detection. The third is news and social monitoring for trading signal generation.

The fourth is customer complaint classification, where US banks route CFPB complaint narratives, internal call transcripts and chat sessions through topic models that feed compliance dashboards. The fifth is contract intelligence, where ISDA master agreements, loan covenants and vendor contracts get parsed for repricing triggers, change-of-control clauses and renewal dates. The sixth is fraud-adjacent text analysis, where transaction memo lines and counterparty descriptions get scored for AML risk.

The technology layer has shifted faster than most of US finance has acknowledged. Five years ago the workhorses were word embeddings (Word2Vec, GloVe) combined with bidirectional LSTMs. Three years ago it was BERT and FinBERT. Today it is a mix of fine-tuned open-weights models (Llama 3, Mistral, Falcon), retrieval-augmented architectures over private corpora, and the major commercial APIs from OpenAI, Anthropic and Google. The US payment rails fintechs sit on generate the structured side of the data these models then reason about textually.

Where the highest-value US finance NLP work actually lives

Three areas have delivered the most disclosed economic value. The first is filings extraction. A large US asset manager that automates the extraction of key items from quarterly filings can cut several hundred hours a month of analyst time and route human attention to the documents that matter most. The savings are real and durable.

The second is customer complaint analytics. US banks subject to CFPB complaint monitoring have invested in NLP pipelines that classify complaints into more granular categories than the CFPB taxonomy itself. The output feeds product, compliance and operations dashboards and routinely catches emerging issues weeks before the official complaint volumes spike. ACH-related complaints are a particularly common signal source for retail fintech operators.

The third is contract intelligence. Vendor contracts, loan covenants and trading agreements have become a target for NLP because the cost of missing a clause (auto-renew, repricing trigger, exclusivity restriction) can run into millions of dollars. Specialist vendors (Kira, Evisort, Ironclad) plus the major firms’ internal builds have made contract analysis a normal part of legal operations at large US financial firms.

Inside the largest US banks, the NLP function has organised into a small platform team that owns the retrieval infrastructure and the evaluation harness, and a federated network of domain teams that own the corpora and the prompts for their specific workflows. The platform team’s measure of success is not model accuracy. It is how quickly a domain team can stand up a new NLP application against existing infrastructure, which is now often measured in days rather than quarters.

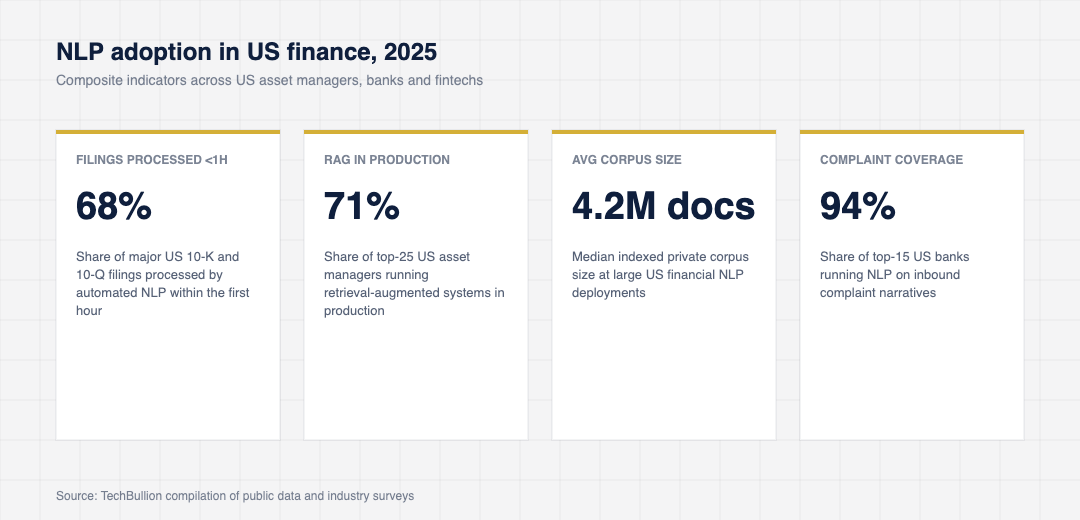

A scoreboard for US finance NLP adoption in 2025

The composite numbers below come from vendor disclosures, US bank technology surveys and the NLP track of recent academic finance conferences. They sketch where the technology has actually taken hold in production.

The figure to watch is the share of US filings now processed by an NLP pipeline inside the first hour of disclosure. Three years ago that share was near zero outside hedge funds. It is now the majority of disclosures at the largest asset managers. The implication for retail investors is that any quick read advantage from a fresh filing has effectively closed, while the structural advantage has shifted to whoever owns the cleanest NLP pipeline.

The compliance posture around NLP in US finance has shifted noticeably. Three years ago, model governance teams treated text models as too opaque to ship into customer-facing flows. The arrival of explainable retrieval (where the model cites the exact passages it used), combined with the OCC’s increasingly settled posture on AI in banking, has lowered the activation energy. Many large US banks now run NLP-driven workflows behind compliance dashboards that show every retrieved citation alongside every model response.

The model and data choices that matter most

The choice between open-weights and commercial API models has become a real strategic question in US finance. Commercial APIs (OpenAI, Anthropic, Google) lead on raw capability and ergonomics. Open-weights models (Llama 3, Mistral, Falcon, the newer Phi models from Microsoft) lead on data residency, cost and control. The largest US banks have largely landed on a hybrid: open-weights for sensitive internal documents, commercial APIs for non-confidential analysis. Smaller US fintechs tend to default to commercial APIs because the engineering cost of operating an open-weights stack at scale is non-trivial.

Retrieval-augmented generation has become the default architecture for any US finance application that needs to ground model output in an internal corpus. The retriever (often a vector database like Pinecone, Weaviate, Qdrant or Postgres with pgvector) sits between the user query and the model, and the model is asked to reason only about the documents the retriever returned. The pattern has cut hallucination rates dramatically and made the regulatory conversation easier.

Evaluation has caught up. A handful of US finance benchmarks (FinBench, FOMC question answering, the contract analysis evaluation suites) now sit alongside the general benchmarks, and serious teams test model performance on these before shipping. Without that discipline, the failure mode is the model that demos beautifully and underperforms on the actual workload three months in. Banking innovation that scales globally nearly always has a serious evaluation harness wrapped around any NLP system that touches customers.

The senior analyst role has also evolved. Rather than reading documents in full, the analyst now reviews the NLP summary, validates a small sample of the model’s claims against the original text, and spends the rest of the time on the higher-order judgement the model cannot replace. Job postings for buy-side analysts in 2025 increasingly require NLP fluency as a baseline, the same way Excel fluency was required twenty years ago.

What US fintech founders should understand about NLP now

Three pieces of advice from US fintechs that have shipped NLP at scale. First, treat the corpus as the moat. The data you fine-tune or retrieve against is the durable asset. A clean, well-indexed private corpus is more valuable than any single model choice, because the model layer will continue to improve and the corpus is what you built.

Second, build the evaluation harness before the model. Most NLP projects in US finance fail because no one defined what good enough looked like before the team started building. A test set with at least several hundred labelled examples from the actual workload, plus an automated metric, is the cheapest hour you will spend.

Third, watch the cost line. Inference cost on production NLP workloads can grow quickly. Caching layer choice, embedding model choice and the decision about whether to run inference on-prem can swing operating costs by an order of magnitude. The teams that watch these levers tend to scale into profitable NLP products. The teams that ignore them tend to discover, four quarters in, that they have built a feature their margins cannot support.

The senior analyst who used to read a 10-K filing alone is still in the room. They are just reading a structured summary, with the original document one click away, and they cover roughly five times as many issuers as they did before. The cost change that produced that shift is the actual story of NLP in US finance.

For the underlying filing infrastructure that NLP pipelines ingest, see SEC EDGAR filing infrastructure.