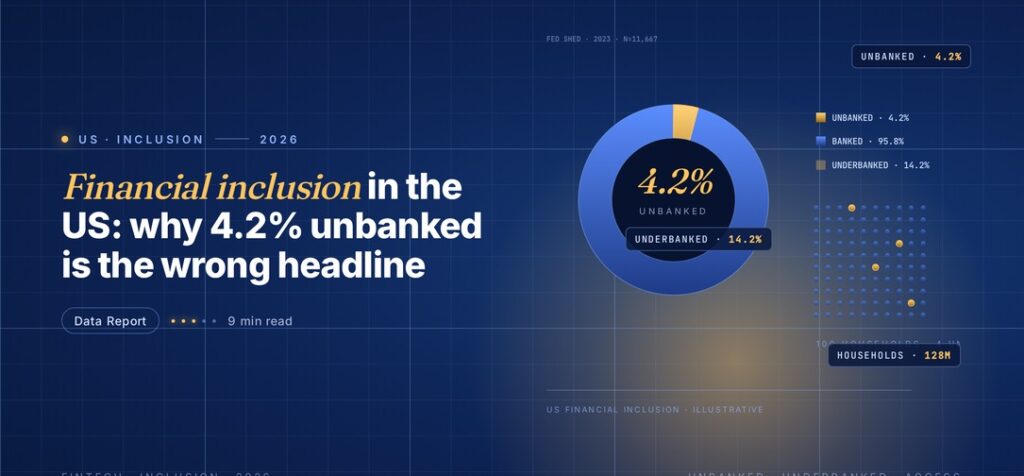

Most Americans last opened a bank account at a branch; a growing share have never set foot in one. In 2023, the FDIC’s National Survey of Unbanked and Underbanked Households found that 4.2 percent of US households, roughly 5.6 million households, had no one with a bank account. It’s the lowest rate since the survey began in 2009, down from 8.2 percent in 2011. But reading the headline as the end of the financial inclusion story misses what has actually changed.

What the 4.2% figure actually covers

The FDIC’s survey counts a household as unbanked if no member has a checking or savings account at an insured institution. By that strict definition, the share is at a record low. The progress is real: the unbanked rate fell by almost half between 2011 and 2023, and the drop has been steepest among Black households (down from 21.4% in 2013 to 10.6% in 2023) and Hispanic households (from 17.9% to 9.5%), although both groups remain roughly three times as likely to be unbanked as the national average.

What the top-line number doesn’t show is how differently banking access looks inside and outside the formal system. Even households with an account increasingly rely on non-bank financial services: the same FDIC survey found 14.2 percent of US households used some form of non-bank credit in 2023, from payday loans and pawn shops to buy-now-pay-later products.

The gap between “banked” and “financially included”

Having an account and being financially included are not the same thing. The Federal Reserve’s 2024 Report on the Economic Well-Being of U.S. Households consistently shows that a meaningful share of Americans with accounts still cannot cover a modest unexpected expense, and the share varies sharply by income and race. Access is a floor; resilience is a ceiling that most Americans still sit well below.

The distinction matters because the frontier for financial inclusion policy has moved. Closing the unbanked gap is now a question of reaching specific, harder-to-serve populations, undocumented workers, people rebuilding credit after bankruptcy, rural households where branch closures have thinned physical access, rather than a broad push across the whole economy.

How fintech changed the distribution

Digital banks, mobile wallets, and prepaid reloadable products have absorbed much of what used to be non-bank activity. A household that in 2015 would have relied on a check casher for every paycheck can now receive direct deposit into a neobank app, pay bills from the same account, and hold a virtual debit card: all without visiting a branch.

This reshaping is visible inside the FDIC data. Mobile banking is now the most common method of account access for banked households, and underbanked households (those with accounts but also using non-bank credit) make up a smaller share than at any point in the survey’s history. The underlying product competition is the subject of our reporting on how fintech is reshaping competition in financial services.

How the US compares globally

The context for US inclusion is that global financial inclusion has moved faster than most observers thought possible. The World Bank’s Global Findex 2025 finds that 79 percent of adults worldwide now have an account, up from 51 percent in 2011. In developing economies, 40 percent of adults saved through a financial account in 2024, a 16-percentage-point jump since 2021, the fastest rise in over a decade.

| Metric | Latest figure | Source |

|---|---|---|

| US unbanked rate (2023) | 4.2% | FDIC |

| US unbanked rate (2011) | 8.2% | FDIC |

| Black US households unbanked (2023) | 10.6% | FDIC |

| Global adult account ownership (2024) | 79% | World Bank Global Findex |

| Developing economies saving in accounts (2024) | 40% | World Bank Global Findex |

| US households using non-bank credit | 14.2% | FDIC |

Table sources: FDIC 2023 National Survey and World Bank Global Findex 2025 (both cited above).

The US progress is real but the global pace means that inclusion is no longer a story the US is leading. Markets with mobile-money penetration above 70 percent, Kenya, Bangladesh, the Philippines, are serving use cases (micro-savings, bill-splitting, cross-border remittances) that US fintech is still working through.

What this means for US fintech and policy

For fintech operators, the unbanked gap in the US is too small on its own to anchor a growth strategy, 5.6 million households, most of whom have been persistently hard to serve. The larger commercial opportunity is the underbanked middle: the 50+ million Americans who have an account but rely on non-bank credit, overdraft products, or cash advances to get through a month. That group is now the target of most new consumer fintech product design.

For policymakers, the 4.2 percent number has quietly shifted the conversation. The CFPB’s and Treasury’s financial inclusion priorities are now less about “reaching the unbanked” and more about the quality of the relationship, overdraft fees, credit invisibility, access to small-dollar credit at non-predatory rates. That second conversation is further connected to the role of digital banking platforms, which we covered in our analysis of how digital banking adoption is accelerating among SMEs.

For investors, the segment that has attracted the most capital, mass-market consumer neobanks, has now fully penetrated the bankable population and must compete for customer lifetime value against incumbents rather than simply winning new accounts. The venture dynamics behind that shift are covered in our piece on the role of venture capital in fintech growth.

Where the remaining unbanked actually live

The geography of the remaining US unbanked population is more concentrated than most policy discussions suggest. FDIC microdata shows that unbanked households cluster in specific census tracts: older rural counties in the lower Mississippi delta, inner-ring urban neighborhoods where branches have closed over the last decade, and border counties with large undocumented populations. Those three clusters account for a disproportionate share of the 5.6 million figure, and the interventions that would move the number further depend on geography rather than on a single product. Mobile-first neobanks have reached the bankable-but-not-banked segment; reaching the last few million will require a mix of in-person identity verification, cash-to-digital onramps that do not depend on a bank branch, and credit products that work for customers with thin or no traditional credit files. The federal banking agencies have started publishing county-level unbanked maps to help allocate Community Reinvestment Act credit toward these specific populations, a shift that gives regional banks a commercial reason to build for the last-mile problem.

The longer arc

Financial inclusion in the US has moved through three phases in living memory: from the branch-expansion era through the post-2008 fintech wave and now into a phase where access is largely solved and quality is the unsolved problem. The 4.2 percent number is a milestone, not a finish line, and the next decade of US inclusion will be decided by who can make the existing system work better for the households already inside it. For a wider view of how fintech is reshaping the banking model globally, our coverage of the future of global digital banking tracks where the inclusion frontier is moving next.