the global embedded finance market is forecast to reach $7 trillion by 2030, according to industry estimates compiled by Boston Consulting Group. Embedded finance, the integration of financial services into non-financial platforms, generated an estimated $92 billion in revenue in 2024. The concept is straightforward: companies that already have customer relationships are adding lending, insurance, payments, and banking services directly into their existing products rather than sending customers to separate financial institutions.

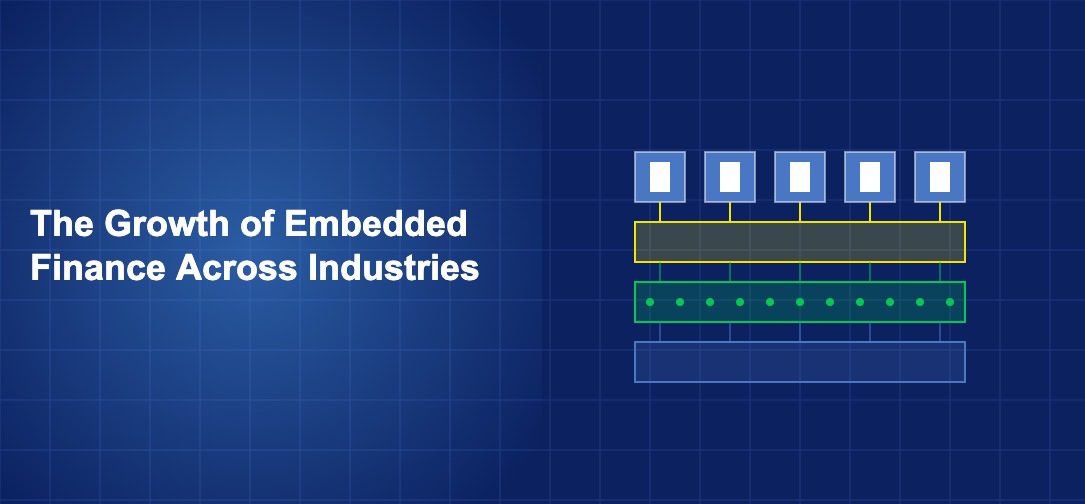

How Embedded Finance Works in Practice

Embedded finance operates through a three-layer architecture. At the bottom, licensed financial institutions (banks, insurance companies, lenders) provide the regulated infrastructure: deposit insurance, lending capital, insurance underwriting. In the middle, fintech infrastructure companies (Stripe Treasury, Unit, Bond, Marqeta) provide the APIs and technology that connect regulated services to non-financial platforms. At the top, the platforms themselves (Shopify, Uber, DoorDash, Salesforce) offer financial products to their users through their existing interfaces.

McKinsey estimated that embedded finance could generate $230 billion in revenue by 2030. The growth is driven by two economic forces. First, non-financial platforms can acquire financial customers at near-zero marginal cost because they already have the customer relationship. Second, financial products offered at the point of need convert at rates 2-5 times higher than standalone financial products marketed through traditional channels.

CB Insights reported that over 150,000 non-financial companies were offering embedded financial services globally in 2024, up from approximately 50,000 in 2021. The adoption rate is accelerating as infrastructure providers make integration simpler and more affordable.

Embedded Payments: The Largest Segment

Embedded payments account for the majority of embedded finance revenue. When a consumer pays through a ride-hailing app, orders food delivery, or purchases through a marketplace, the payment processing is embedded into the platform experience. The consumer does not interact with a separate payment provider.

Stripe processed $1 trillion in payments in 2023, with the majority flowing through embedded integrations in platforms and marketplaces. Adyen’s platform business grew 29% in the first half of 2024. Square (Block) generated $21.8 billion in revenue in 2023, primarily from payment processing embedded in merchant point-of-sale systems.

fintech platforms are reducing financial transaction costs by up to 80% and embedded payments contribute directly to this efficiency by reducing the number of steps between a purchase decision and payment completion. Statista data shows that one-click payment methods, enabled by embedded payment infrastructure, increase checkout conversion rates by 25-35% compared to traditional payment forms.

Embedded Lending: Credit at the Point of Need

Embedded lending is the fastest-growing segment of embedded finance. Buy-now-pay-later at retail checkout is the most visible example, but embedded lending extends far beyond consumer retail. Shopify Capital has disbursed over $5 billion in merchant cash advances, offered automatically to merchants based on their sales data. Amazon provides working capital loans to marketplace sellers. Uber offers vehicle financing to drivers through in-app lending partnerships.

S&P Global estimated that embedded lending volume reached $120 billion globally in 2024 and is growing at 30% annually. The conversion advantage is significant: merchant lending offered through e-commerce platforms converts at 15-20%, compared to 2-3% for traditional bank marketing of business loans.

digital lending platforms originated $47 billion in personal loans in 2025 through both standalone and embedded channels, with embedded lending growing faster as platforms gain more data about borrower behavior and repayment capacity. The platforms that offer embedded lending have a structural data advantage: they observe the borrower’s revenue, customer base, inventory, and growth trajectory in real time, enabling more accurate underwriting than credit bureau data alone.

Embedded Insurance and Banking

Embedded insurance is growing as platforms add coverage options at points of purchase or service. Tesla offers insurance directly through its vehicle purchase process, using driving data from its cars to price policies. Airbnb includes host protection insurance in its platform fees. Airlines offer travel insurance at booking. Ride-hailing apps provide ride-specific coverage.

The global embedded insurance market reached $70 billion in gross written premiums in 2024, according to BCG. Companies like Qover, Bolttech, and Cover Genius provide the infrastructure that allows non-insurance companies to offer coverage products without obtaining insurance licenses.

Embedded banking is the newest segment. Companies like Unit, Treasury Prime, and Column enable non-bank companies to offer FDIC-insured deposit accounts, debit cards, and payment processing under their own brand. fintech platforms are growing faster than traditional banks in user experience design and are extending that advantage by embedding banking services into the platforms where users already spend their time, whether that is a gig economy app, a payroll system, or an e-commerce marketplace.

Industry-Specific Embedded Finance

Embedded finance is expanding into industry-specific applications that go beyond generic lending and payments. In healthcare, companies like Sunbit and CareCredit embed patient financing into medical provider workflows. In real estate, platforms like Divvy Homes and Better embed mortgage services into home search platforms. In logistics, companies like Flexport embed trade finance into supply chain management software.

financial APIs are powering the next generation of fintech platforms that can be customized for specific industry workflows. A healthcare lending API has different requirements than an e-commerce BNPL API: different regulatory disclosures, different underwriting criteria, different repayment structures. Infrastructure providers are building industry-specific modules that address these differences while maintaining standard integration patterns.

global fintech revenue is expected to triple within the next decade will drive the next phase of embedded finance growth. As APIs become more specialized and easier to integrate, the number of industries and use cases for embedded financial services will continue to expand. The long-term vision is that every software platform with a customer relationship will offer some form of financial service, with the financial infrastructure invisible to the end user.

Embedded finance in 2026 has moved from concept to mainstream adoption. Shopify is a financial services company. Uber is a financial services company. Amazon is a financial services company. None of them describe themselves that way, but each generates billions in revenue from financial products embedded into their platforms. The $7 trillion projected market represents the logical extension of a trend that has been building for a decade: financial services moving from standalone institutions to invisible infrastructure embedded in the platforms where people already live, work, and shop.