The first time an American paid for a meal with a piece of plastic was 1950, when Frank McNamara handed a Diners Club card to a waiter at Major’s Cabin Grill in Manhattan. Three quarters of a century later, the country runs more than 132 billion non-cash payments a year, according to the Federal Reserve, and the story of how the plumbing was built is the most useful background a US fintech founder can have.

How the country built its payment plumbing

American financial infrastructure was assembled in layers, not all at once. The Federal Reserve was created in 1913 to give the country a real central bank after the panics of 1893 and 1907. ACH followed in 1972, when the San Francisco clearing house went live so payroll could stop moving on paper. Visa and MasterCard formed in the late 1960s, the wire networks Fedwire and CHIPS scaled in the 1970s, and the SEC’s modernisation of equity market structure ran from the 1975 Securities Acts Amendments through Regulation NMS in 2005. Each of these layers is still load-bearing today, which is why the US payment rails every fintech has to think about still include a 1970s batch system alongside a 2023 instant network.

The pattern across these decades is consistent. A specific market failure, a panic or an inefficiency, prompts a coalition of banks, regulators and operators to build something durable. Once that piece is built, almost nothing replaces it. New layers get added on top.

Founders sometimes treat the pre-internet era as ancient history, but a surprising amount of today’s regulatory and operational logic was set in those decades. The Bank Secrecy Act of 1970 still defines AML obligations. The Truth in Lending Act of 1968 still defines how consumer credit must be disclosed. The 1974 Equal Credit Opportunity Act sits underneath every credit underwriting model that touches a US consumer. When a modern fintech lawyer flags a model risk concern, they are usually citing rules that predate the personal computer.

Three waves that reshaped American finance

If you compress the modern era into three waves, the shape of the country’s innovation history becomes clearer. The first wave, from roughly 1968 to 1990, was the institutional automation wave. Banks moved from paper to mainframe. Trade settlement compressed from five days to three. The SEC pushed market structure from physical floors toward computer-mediated matching engines. Citibank, Bank of America and JPMorgan spent more on technology in this period than most readers realise.

The second wave, from about 1995 to 2010, was the internet wave. PayPal launched on eBay in 1998. E-Trade and Ameritrade brought retail brokerage online. The 2008 crisis then forced a regulatory reset, with the Dodd-Frank Act, Basel III, the establishment of the CFPB, and a wave of post-crisis compliance investment that built much of the infrastructure today’s RegTech vendors plug into.

The third wave, from 2010 to today, is the API and mobile wave. Stripe shipped its first API in 2010. Square began processing card payments on phone-attached dongles in 2009. Plaid started linking bank accounts in 2013. Venmo became a verb. The Federal Reserve’s FedNow service launched in July 2023, finally giving the country a 24/7 instant payment rail of its own. Crypto, embedded finance and the current generation of AI-driven workflow tools all sit on top of this wave.

A scoreboard for the last decade

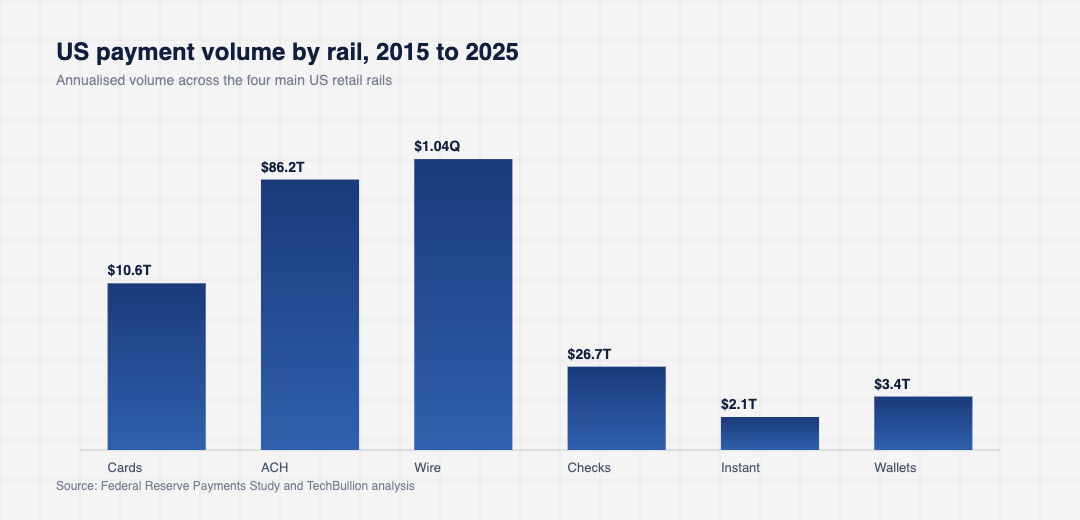

The numbers are the cleanest way to see how much has changed since 2015. Card payments, mobile wallet adoption, instant payment volume and digital lending originations all moved by an order of magnitude. The chart below pulls a handful of indicators from the Federal Reserve Payments Study and CFPB market monitoring data to give a single snapshot.

The line that surprises most operators is the one for instant payments. Real-time settlement was a niche idea in 2015. By the end of 2025, FedNow had cleared more than 1.4 million transactions per business day across more than 1,300 participating institutions, and The Clearing House’s RTP network was settling several billion dollars a day in parallel. Neither network has displaced ACH, which is still the spine of payroll and bill payment, but they have changed expectations. A consumer who has used Zelle for a peer transfer does not understand why their tax refund takes nine days.

What the historical pattern says about the next ten years

The same logic that shaped 1972 and 1998 is still shaping 2026. Each generation of American financial innovation has done three things in sequence. First, a new substrate becomes available, whether that is mainframes, the public internet, smartphones, or now general purpose AI and tokenised rails. Second, a handful of operators figure out how to expose that substrate as a simple developer or consumer surface. Third, regulation and risk management catch up, often after a stress event, and the surface becomes a default.

If that pattern holds, the 2026 to 2035 window will produce mainstream infrastructure around three substrates that are already visible. AI is the obvious one, with the model providers, the workflow tooling layer, and the model risk frameworks all moving into place at the same time. Stablecoins are the second, with regulated US dollar tokens now sitting on bank balance sheets and starting to move B2B treasury flows. Identity is the third, with the rollout of mobile driver licences in more than a dozen states giving fintechs a digital identity primitive that did not exist in the previous wave.

Look at the wave that produced the post-2008 generation. The wave was not created by a single product. It was created by simultaneous moves at the Federal Reserve, the SEC, the CFPB and the OCC, plus a venture capital cycle that finally caught up with the technology. The same pattern is visible in 2025 and 2026. Stablecoin guidance from the OCC, the Fed’s Section 13 process for novel bank charters, and the SEC’s stance on tokenised securities are all moving at the same time. Operators who track all four agencies at once tend to read the curve a quarter or two ahead of the broader market.

Founders who study the timing of past waves tend to make better bets than those who chase the narrative of the moment. The fintech operators who shipped in 2009 and 2010 built into a substrate that was about to scale by a factor of ten. The ones who shipped in 2014 and 2015, against the same substrate, mostly built features for somebody else’s platform.

Treasury teams at large US banks have begun running stablecoin settlement pilots that would have been illegal to discuss publicly five years ago. None of that is hype. It is a slow, agency-by-agency expansion of what banks are permitted to do, and it rhymes very closely with how ACH and the card networks were authorised in their own time.

The lessons founders keep relearning

Three lessons from American financial innovation history keep coming back when you read the founding stories of today’s category leaders. The first lesson is that distribution beats novelty. Diners Club did not invent the credit card; it solved the chicken-and-egg problem between merchants and consumers in a single city, then scaled out. PayPal did not invent online payments; it became the default on eBay. Plaid did not invent bank data aggregation; it built a developer-friendly wrapper around something engineers were already trying to do badly themselves.

The second lesson is that the boring rails matter most. ACH still moves more value than any other US retail rail, and the operators who understand its quirks (return codes, settlement windows, the dance between originating and receiving banks) build products that other founders cannot replicate from a deck.

The third lesson is that regulators are slow but not absent. The CFPB, OCC, FDIC and Federal Reserve each have a long memory. Founders who treat compliance as a moat rather than a tax tend to compound. Banking innovation that scales globally has, in almost every case, been built by teams that took the regulatory conversation seriously from year one.

None of this means the next decade will look like the last. It means the country’s financial innovation history is more useful as a guide than founders sometimes assume, and that the operators who treat it as required reading tend to end up with the durable companies.

For longitudinal US non-cash payments data referenced above, see the Federal Reserve Payments Study.