Industry-trend lists in FinTech tend to age badly. The 2022 lists were dominated by buy-now-pay-later and crypto. The 2023 lists were dominated by AI. The 2024 lists were dominated by AI plus regulatory pullback. The pattern of any given year reflects what is loud, not what is structurally most important. The trends that actually matter for U.S. FinTech operators in 2026 are quieter, more cumulative, and easier to underweight in a quarterly review.

This piece sets out the trends that are doing the most to reshape U.S. FinTech right now, with an emphasis on second-order effects rather than headline categories. The format is intentionally selective: a short list of forces, each large enough to bend the next decade.

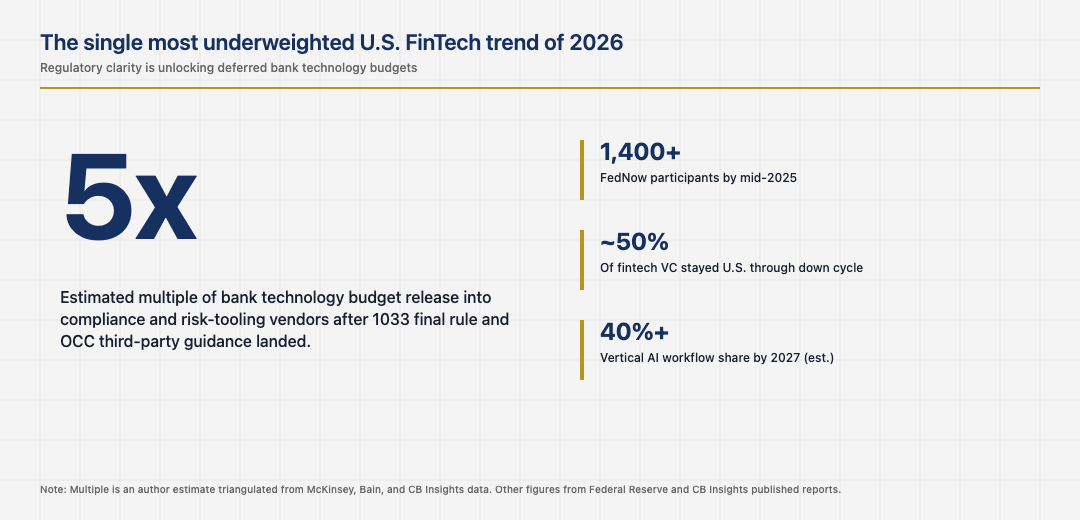

The compounding effect of regulatory clarity

The most underrated trend of the past two years is the slow, uneven, real arrival of regulatory clarity in places that used to be ambiguous. The CFPB’s 1033 final rule on personal financial data rights set the shape of who owns customer data and who can move it. The OCC’s third-party risk guidance set the baseline for bank-fintech partnerships. State adoption of the Money Transmission Modernization Act has materially reduced the multi-state licensing burden. These individually look procedural. Cumulatively they reduce the regulatory uncertainty discount that investors had been applying to the entire category.

The implication for operators is that the categories that benefited most from ambiguity now have to compete on the merits. The categories that suffered most from ambiguity, particularly compliance and risk-tooling vendors, are now winning more of the budgets that banks had been holding back. The reset is uneven. It is also durable, in a way that few of the louder trends are.

AI moves from horizontal to vertical

The first wave of AI in finance was horizontal: generic LLMs applied to customer support, document summarisation, and code assistance. The trend that matters in 2026 is the vertical wave, where specialised models, fine-tuned on financial data, are quietly replacing line-of-business workflows in commercial credit underwriting, fraud-pattern detection, and regulatory disclosure analysis.

The vertical applications are less newsworthy because they do not sit in front of a user. They sit inside a credit committee, an AML team, or a disclosure-review queue. The dollars they save are large enough that they will reshape commercial bank and insurance economics over the next three years, even if the consumer-facing AI products attract more press attention. Read the trend through this lens and the priorities of any sensible bank technology budget become clearer.

Real-time payments crosses the convenience threshold

FedNow has crossed the threshold from infrastructure curiosity to active use case in 2026. The Federal Reserve’s published participant count is over 1,400 institutions and counting. RTP from The Clearing House continues to grow. The combined volumes are still small relative to ACH or card volume, but the curve has steepened, particularly for B2B payouts, payroll, and account-to-account movement that used to depend on next-day ACH.

The competitive question is whether real-time payments cannibalise card interchange faster than the card networks can defend the experience layer. The current evidence suggests that erosion will be slow but real, and that the firms positioning for an account-to-account future will quietly accumulate share over a five-to-seven year horizon while the networks defend the experience layer with rewards programs and merchant tooling.

Embedded finance moves from pitch to production

Embedded finance has been a pitch-deck trend for several years and is now becoming a production trend. Vertical SaaS platforms in healthcare, construction, restaurants, and field services are embedding payments, lending, and insurance into workflows that used to require separate provider relationships. The economics work because the SaaS platform owns the workflow data, which makes underwriting cheaper and customer acquisition essentially free at the margin.

The companies winning here are not the loud BaaS platforms of the prior cycle. They are the SaaS platforms that decided to absorb the financial product themselves through partnerships with chartered banks, sometimes with sponsorship banks and sometimes through direct charters. The structural lesson is that financial product distribution is migrating to whoever owns the workflow, not whoever owns the licence, and any operator strategy that ignores this is fighting last decade’s competitive battle.

Capital markets reset and the durable-economics filter

The fifth trend is the discipline of capital. The growth-at-any-cost trade is over. Public market investors have made clear that they will reward profitable fintech operators with multiples and punish unprofitable ones with discounts. Private capital has internalised the same lesson. The result is a market in which the best operators are accumulating share at the expense of weaker peers, often through acqui-hires and tuck-in acquisitions that look unglamorous on the surface and matter enormously in three years.

Each of these trends is structurally durable. None of them is the kind of headline a trend deck wants to feature. Read together, they describe a U.S. FinTech market that is maturing in the right places: regulatory clarity is improving, AI is moving to where the dollars are, payments rails are scaling, distribution is migrating to workflow owners, and capital is becoming more selective. The operators who are positioning against these forces are the ones most likely to find themselves on the right side of the next cycle.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.