The most expensive bug in a US bank is the one nobody catches before it touches a customer balance. The reconciliation surface of a modern US bank, the layer that decides whether two ledgers tell the same story, is exactly the kind of code where a missing test does not show up in QA and does not show up in user feedback; it shows up months later as a mismatched balance that has to be unwound across thousands of customers. Stories like that are the reason unit testing in financial applications is no longer an engineering hygiene topic. It is part of the bank’s risk control framework, and US regulators have started to treat it that way.

What Unit Testing in Financial Applications Now Covers

Inside a typical US bank engineering organization, unit testing covers the per function and per class tests that run on every commit. These sit at the bottom of the test pyramid, below integration tests, contract tests, and end to end suites. Unit tests are fast, deterministic, and run thousands of times per day inside continuous integration pipelines on GitHub Actions, Jenkins, or internal platforms.

The scope has expanded. Unit tests at US banks now cover not just business logic but data transformations, state machine transitions, regulatory rules, and fraud signal calculations. A modern US bank service typically ships with substantial unit test coverage, weighted heaviest on the modules that touch money movement or customer identity, where the cost of a regression is highest.

The cultural shift is the bigger story. Five years ago a meaningful share of US bank engineering teams treated unit tests as an after the fact obligation. Today, the senior engineers write tests first or in tandem with the code, the code reviewers refuse pull requests without coverage, and the platform teams instrument the test suite as a first class production system.

The Workloads Where Unit Testing Has the Highest Return

Three categories of US banking code have the steepest cost of failure, and they are where unit testing investment concentrates.

The first is the ledger. Any code path that posts to a debit, credit, or balance update is subject to the highest scrutiny. Unit tests cover the arithmetic, the rounding behaviour, the currency conversion, the holiday calendars, and the corner cases around zero and negative balances. A bug in this layer is visible on the bank’s general ledger in hours, and the audit trail back to the original deployment is short.

The second is fraud and risk scoring. The model output that decides whether to approve a card transaction or freeze an account has to be tested against a known suite of cases, including the false positive scenarios that affect legitimate customers. US bank fraud teams maintain test fixtures with thousands of historical cases that every new model has to pass before deployment.

The third is regulatory rule engines. The code that decides whether a transaction triggers a Currency Transaction Report, a Suspicious Activity Report filing, or an OFAC sanctions screen is high risk. Unit tests document the regulatory intent, capture the boundary conditions, and create a defensible record for the bank’s compliance officer to review.

A fourth category, identity and authentication code, has its own unit test requirement profile. Password handling, token generation, session management, and step up authentication all have well known failure modes that unit tests document and protect against. The investment in test coverage here is justified by the cost of a single account takeover incident at a US bank, which routinely runs into six figures even before regulatory remediation.

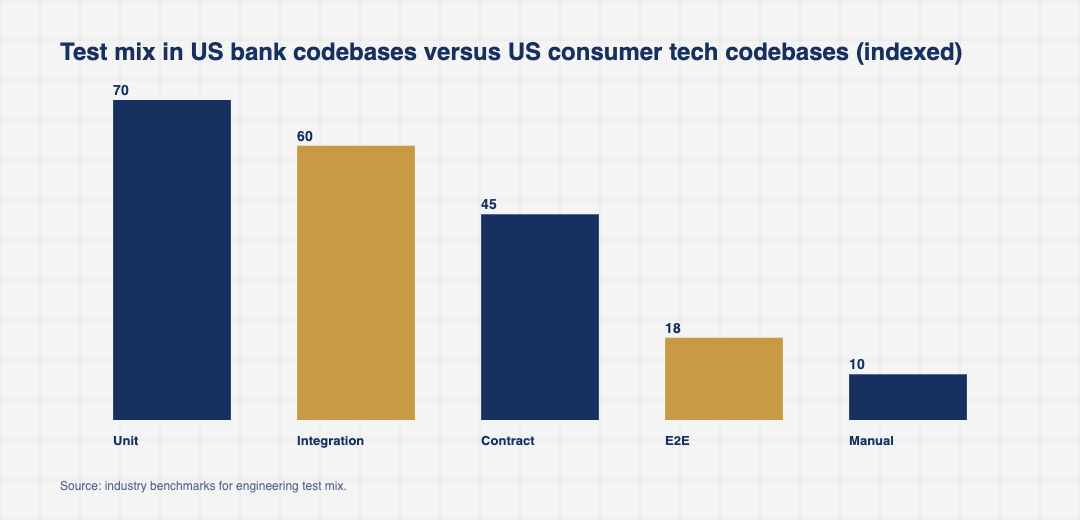

How Unit Testing in Financial Applications Compares to Other Layers

The test pyramid inside a US bank looks different from a typical consumer tech company.

Unit tests still account for the largest share of total test count. Integration tests follow, with a much higher share than the typical consumer company because US banks need to validate interactions between systems that cross regulatory boundaries. Contract tests have grown rapidly, used to validate the API contracts between microservices and between the bank and its external partners. End to end tests, which are slow and brittle, are kept to the smallest viable set.

The result is a slower delivery pipeline than a pure consumer technology company would tolerate, but a meaningfully lower change failure rate. For a US bank that ships to production multiple times per day, this is the trade off that the engineering culture has explicitly chosen.

The Friction Points That Slow Unit Testing Adoption

Three frictions are well known and well managed.

The first is legacy code. Large parts of every US bank codebase predate the modern unit testing culture. Adding tests to code that was not written for testability is hard, often requiring refactoring before a meaningful test can be written. Most US banks have accepted this as a long term investment and run dedicated programs to add tests to high risk legacy modules.

The second is test data. Realistic financial test data is hard to synthesize. US banks have invested in test data platforms that generate plausible customer profiles, transaction streams, and edge cases, with PII safely anonymized. The platforms are expensive to build and maintain, but the alternative, using production data in test environments, is rarely acceptable from a regulatory perspective.

The third is flaky tests. A test suite with even a small percentage of intermittently failing tests erodes trust in the entire pipeline. US bank platform engineering teams now treat flaky test detection and removal as a continuous program, with internal dashboards showing flake rate by repository and team.

Where Unit Testing in Financial Applications Is Heading

Three signals shape the next phase.

The first is AI assisted test generation. GitHub Copilot, internal bank LLMs, and dedicated unit test generation tools have started writing first draft tests from a function signature and a few examples. The senior engineer reviews and curates, but the productivity gain on test coverage is measurable, particularly for the boilerplate cases.

The second is property based testing. Tools like Hypothesis in Python and similar libraries in Java and Kotlin have moved from a niche enthusiasm to a standard part of the testing toolkit at the most mature US bank engineering teams. The idea, that a test specifies properties rather than examples, is a particularly good fit for financial code where the invariants are well defined.

The third is the slow extension of unit testing practices to data pipelines, machine learning models, and infrastructure as code. The tools to test a SQL transformation, a model artefact, or a Terraform module are now mature enough that US bank teams have started building them into the standard delivery pipeline.

For US bank engineering leaders, the question is no longer whether to invest in unit testing. It is how to keep the test suite healthy as the codebase grows, how to measure the value the suite is delivering, and how to extend the testing discipline to the new categories of code being written across the bank.

A fourth signal is the way US regulatory expectations around model risk and operational risk have begun to shape software development discipline. The SR 11-7 model risk management guidance issued jointly by the Federal Reserve and the OCC sets expectations for testing, documentation, and ongoing monitoring of models in production, and bank examiners increasingly treat the supporting software around those models with similar scrutiny. That has moved unit testing from a pure engineering practice into something the chief risk officer reads about.

Reconciliation-class bugs of the kind the industry has occasionally surfaced through public post-mortems tend to be found by a customer first and a test later. The remediation work that follows usually means backfilling unit tests across the affected services for the better part of a year before the engineering team feels comfortable with the surface again. That kind of story has shaped how US banks now think about testing, and the result is that unit testing in financial applications has stopped being a developer preference and become a control that the bank itself depends on. That is a quiet but durable change, and it will keep shaping how US banking software gets built for the rest of the decade.