Financial systems architecture is a dry phrase for the most consequential set of design decisions any FinTech company makes. Get the architecture right and the company can absorb growth, regulatory change, and partnership shifts without rewriting itself every two years. Get it wrong and the rewrites become the company’s actual product, paid for in cycles of customer attrition and engineering burnout.

This piece sets out the architectural patterns that separate the U.S. FinTech operators who survive scale from the ones who do not. The framing is deliberately practitioner-focused. The patterns are unglamorous. They are also where most of the value in modern financial systems gets created or destroyed.

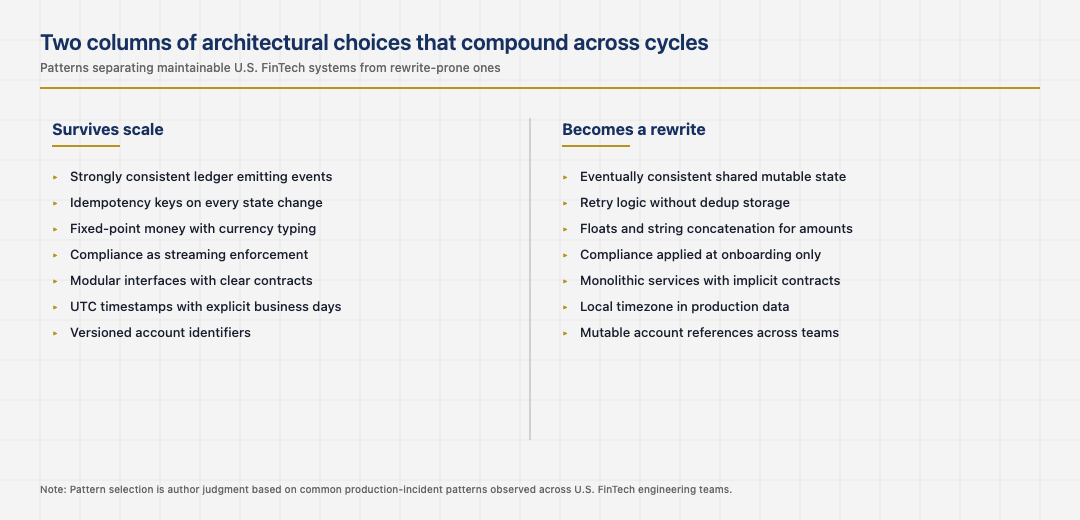

Money in motion versus money at rest

The first architectural decision is the cleanest separation between money in motion and money at rest. Money at rest lives on a ledger: a system of record that knows balances, ownership, and history with strict consistency. Money in motion lives on a wire: a system of transit that knows messages, sequencing, and counterparty state. The two sets of guarantees are different, and conflating them is the source of most of the ugliest production incidents.

The mature pattern is a strongly consistent ledger that emits events to message-driven downstream systems. The ledger never bends its consistency rules. The downstream systems handle the asynchrony. The temptation to take shortcuts shows up on every team that has not yet had a bad outage. The discipline shows up on every team that has.

Idempotency, not retries

The second architectural decision is treating idempotency as a first-class property rather than an afterthought added during the second incident postmortem. Every state-changing operation needs a deterministic key, deduplication storage, and a clear contract about what happens on retries.

This is unglamorous. It is also the difference between a payments system that can be retried safely under partial failure and one that double-charges customers. The U.S. operators who scale through volume spikes without incident are the ones who built idempotency into the request layer from day one. The ones who add it later spend the next eighteen months patching the gaps it should have closed.

The data model is the architecture

The third decision is the data model itself. Financial data has hard rules: amounts in fixed-point representation, currencies as enumerated codes, timestamps with timezone awareness, account references with versioned identifiers. Operators who treat these as flexible primitives end up reconciling rounding errors and timezone bugs forever.

The mature data model treats money as a typed, fixed-point value with a currency code and an explicit precision. It treats accounts as immutable identifiers with a separate mutable state table. It treats time as UTC with explicit business-day overlays. None of this is novel. All of it is consistently underbudgeted in the architecture review until the rounding errors hit production.

Compliance as a system, not a checklist

The fourth architectural decision is treating compliance as a continuously enforceable system rather than a checklist applied during onboarding. KYC needs to refresh. AML monitoring needs to run on streaming transaction data. Sanctions screening needs to fire on every counterparty. The compliance state of a customer or transaction is a first-class element of the data model, not a metadata field.

The operators who build this way satisfy supervisory expectations without rebuilding their pipelines every time the rules change. The operators who treat compliance as bolt-on logic find themselves rewriting it under regulatory pressure on someone else’s timeline. The cost difference between the two patterns shows up in every supervisory exam and every partnership negotiation with a sponsorship bank.

Architecture for change, not just for scale

The fifth decision is the meta-decision: building for change rather than just for scale. The U.S. financial system is in continuous flux. Card networks update their rules. Payment rails launch new capabilities. Regulators update their guidance. Sponsorship banks change their risk appetite. Operators whose architectures cannot absorb these changes spend their engineering capacity on adaptation work that customers never see.

The pattern that absorbs change well is modular: separable modules behind clear interfaces, with explicit contracts about what each module owns and what it depends on from others. The pattern that does not absorb change is the inverse: monolithic systems where a payments rail change requires a four-team coordination effort. The mature U.S. operators have largely converged on the modular pattern. The newer operators learn it the hard way during their first major regulatory change cycle, usually after losing a partnership over an integration timeline they could not meet.

Read across these five decisions, the architectural pattern that defines durable U.S. FinTech operators in 2026 is not exotic. It is disciplined separation of concerns, hard data typing, idempotent state changes, compliance as continuous enforcement, and modularity for change. The companies who treat these as foundational rather than aspirational compound their advantage with every quarter. The companies who treat them as luxuries spend their next funding round paying down the architectural debt they accumulated.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.