Ask most people what it takes to become a venture capitalist and the answer arrives almost by reflex: a top-tier MBA, a few years in investment banking, and the right business card. It is a tidy story, and the data shows it is largely wrong.

The evidence assembled over the past decade, from Cambridge Associates’ performance database, PitchBook’s fundraising records, the Kauffman Foundation’s landmark limited partner research and analyses of thousands of investor backgrounds, points to a conclusion that should reframe how aspiring fund managers think about the industry. Credentials do not predict venture returns. Access, judgement and specialist knowledge do. Nearly half of the investment partners at venture firms hold no MBA at all, the majority of top-performing funds in most vintage years are run by managers on their first or second fund, and the small, focused vehicles that newcomers typically raise are precisely the fund profile that dominates the top of the return tables.

None of this makes raising a first fund easy, the fundraising data is sobering, and this article does not pretend otherwise. But it does mean the barrier is not the one most people assume. What follows is a full, evidence-based examination: who actually runs venture capital, how first-time managers perform, what the current fundraising market really looks like, and the practical route map the data supports for launching a fund without a conventional finance pedigree.

The credential myth: who actually runs venture capital

Start with the most basic question: how many professional venture investors actually hold the qualifications the stereotype demands?

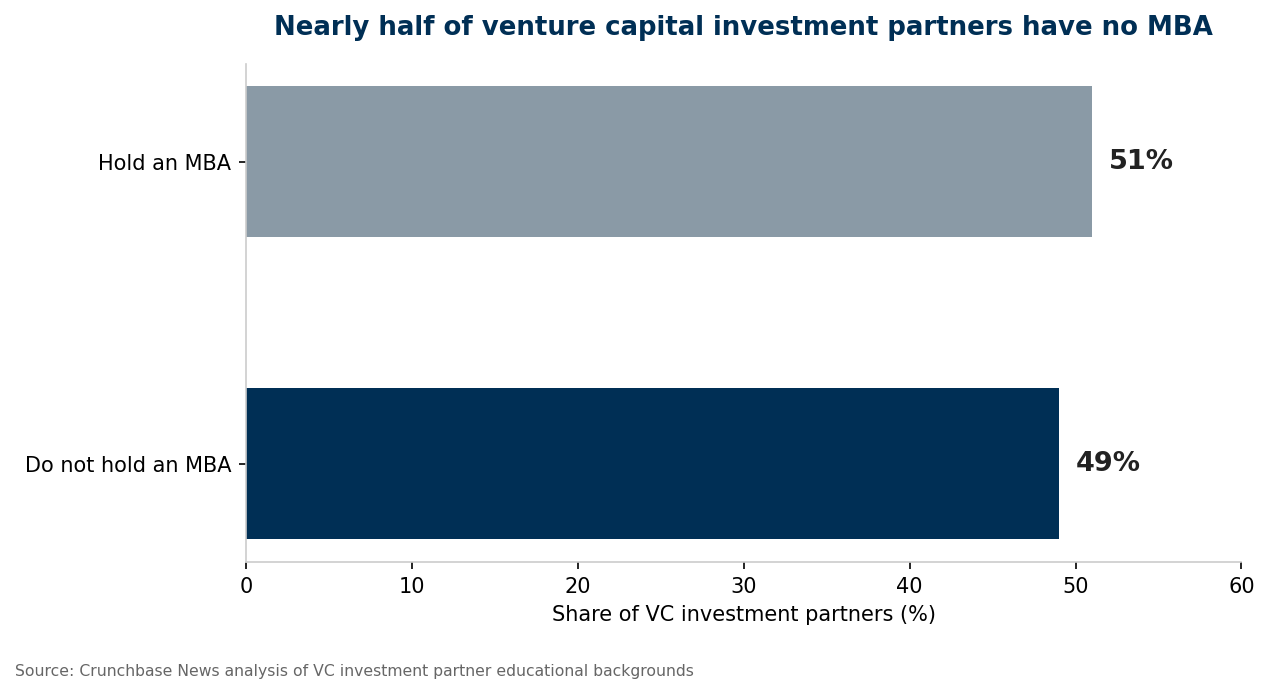

A Crunchbase News analysis of the educational backgrounds of investment partners at venture firms found that just 51% held an MBA, the barest possible majority. Put differently, nearly one in two of the people making institutional venture decisions reached the partner level without ever setting foot in a business school. The same dataset found that around 16% held a doctorate or medical degree instead, a reflection of how much of modern venture, biotech, deep tech, artificial intelligence, rewards scientific depth over financial training. Among angel investors, who collectively write a substantial share of early-stage cheques, MBA prevalence falls further still.

The picture is similar when one asks where investors worked before venture, rather than where they studied. CB Insights examined its ranking of the world’s top 100 venture capitalists and found that 38 had founded or co-founded a company before becoming investors, while 62 had not, and that six of the top ten on the list had never founded a company at all. The elite of the industry includes former journalists, engineers, operators, scientists and salespeople alongside the bankers and consultants. European research by Leta Capital, examining 300 venture investors who had raised at least one fund of $50 million or more, found only around 17% had entrepreneurial backgrounds; the remainder came from an assortment of corporate, technical and analytical careers.

Two conclusions follow. First, there is no single doorway into venture capital, and the credentialed route, banking, MBA, associate seat, describes barely half the industry even at its most traditional. Second, and more importantly for anyone weighing a fund launch: if backgrounds are this heterogeneous at the top of the profession, then the qualification limited partners are actually underwriting must be something other than the certificate on the wall. The performance data shows exactly what that something is.

The performance evidence: first-time managers punch above their weight

Here is the finding that should anchor every conversation about launching a fund without conventional credentials: emerging managers, those raising their first few funds, are not the speculative fringe of venture capital. They are, by the numbers, its performance engine.

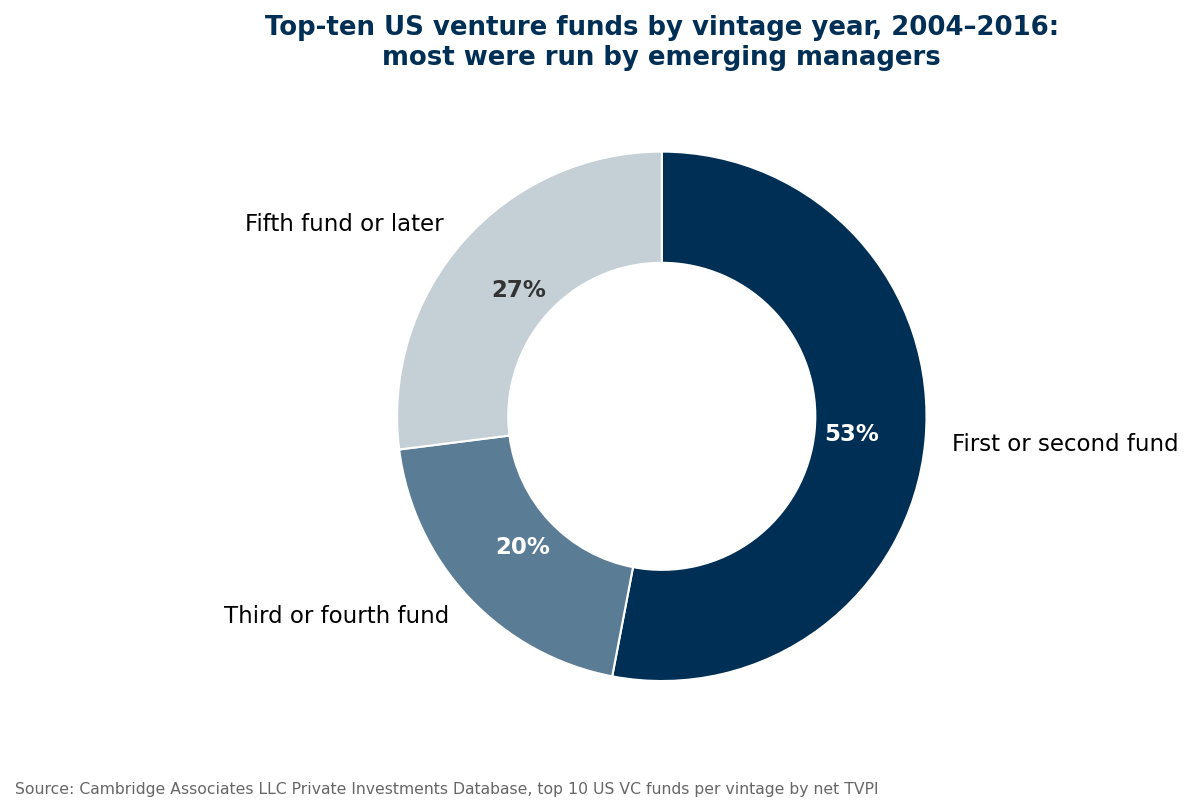

Cambridge Associates, whose private investments database is among the most rigorous in the industry, states the finding plainly: while venture investing often connotes established, access-constrained franchises, a majority of the top-quartile performers in a given vintage year are actually emerging managers raising one of their first few funds. Its analysis of the top ten US venture funds by vintage between 2004 and 2016 found that 53% were run by managers on their first or second fund; extend the definition to managers on any of their first four funds and the figure rises to roughly 73%. Established franchises raising their fifth fund or later, the firms most LPs instinctively regard as the safe choice, accounted for barely a quarter of the very best funds.

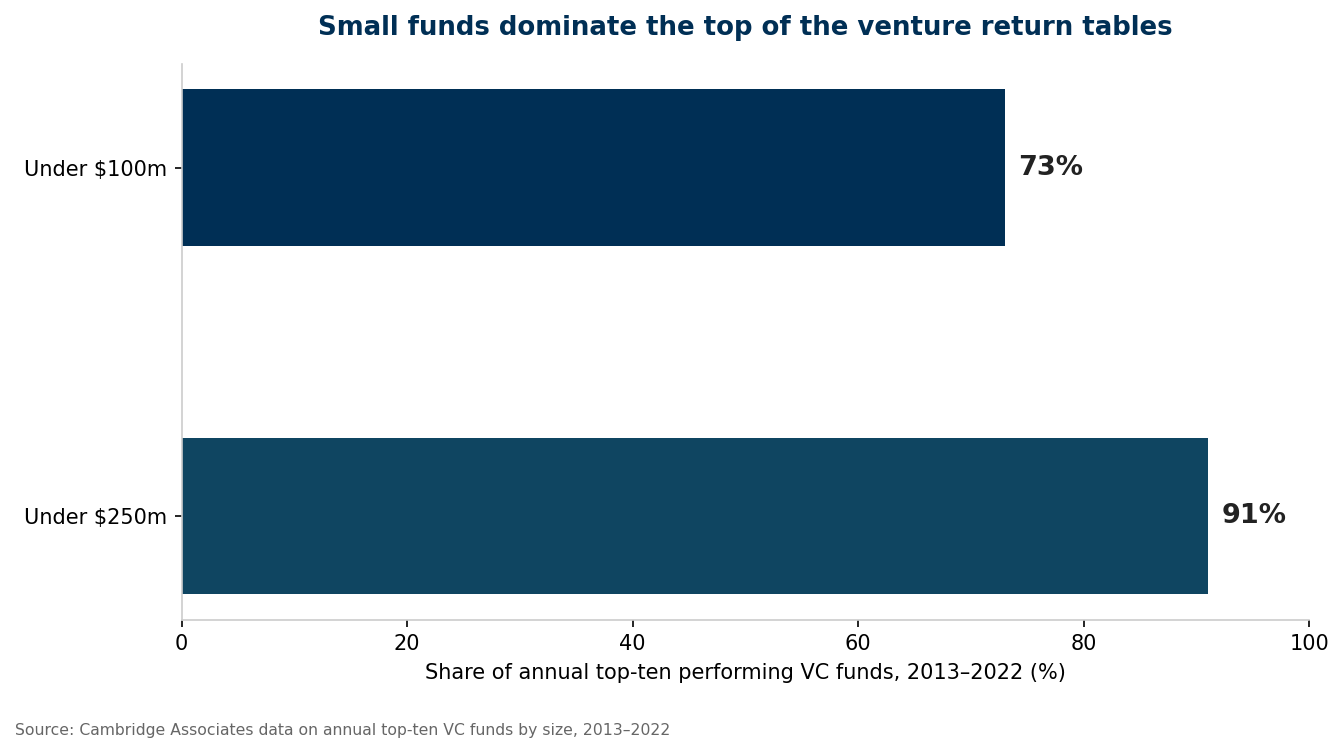

The supporting evidence is consistent across sources and decades. The Kauffman Foundation’s influential study of its own venture portfolio found that, between 1997 and 2011, first-time funds outperformed established firms by an average of 3.1 percentage points annually. PitchBook analysis has found that close to 18% of first-time funds achieve an internal rate of return of 25% or higher, against roughly 12% of funds from seasoned managers. And size, the natural condition of a debut fund, turns out to be an advantage rather than a handicap: of the annual top-ten performing venture funds between 2013 and 2022, 91% were smaller than $250 million and 73% smaller than $100 million.

Why should newcomers outperform? The mechanics are not mysterious. A small fund needs only modest outcomes to multiply: a $20 million vehicle returns its entire fund on a single $20 million realised position, while a $2 billion fund barely registers it, which means small managers can profit from the broad middle of startup outcomes that megafunds must ignore. First-time managers are also structurally hungrier, their entire career rests on Fund I, and tend to run concentrated, conviction-led portfolios in markets they know intimately, rather than the diversified index-like exposure that large platforms drift towards. None of this requires an MBA. All of it requires genuine edge in a specific market, which is a different and far more accessible qualification.

One caveat belongs here, in fairness to the data. Dispersion among emerging managers is wider than among established firms: the same cohort that produces a disproportionate share of top-decile funds also produces more bottom-quartile ones. The emerging manager premium is real, but it is a premium on selection, which is precisely why limited partners scrutinise the things examined later in this article.

The honest part: what the fundraising data really shows

If the performance case is encouraging, the fundraising environment demands honesty. Raising a first fund today is harder than at any point in the past decade, and anyone considering the path should see the numbers unvarnished.

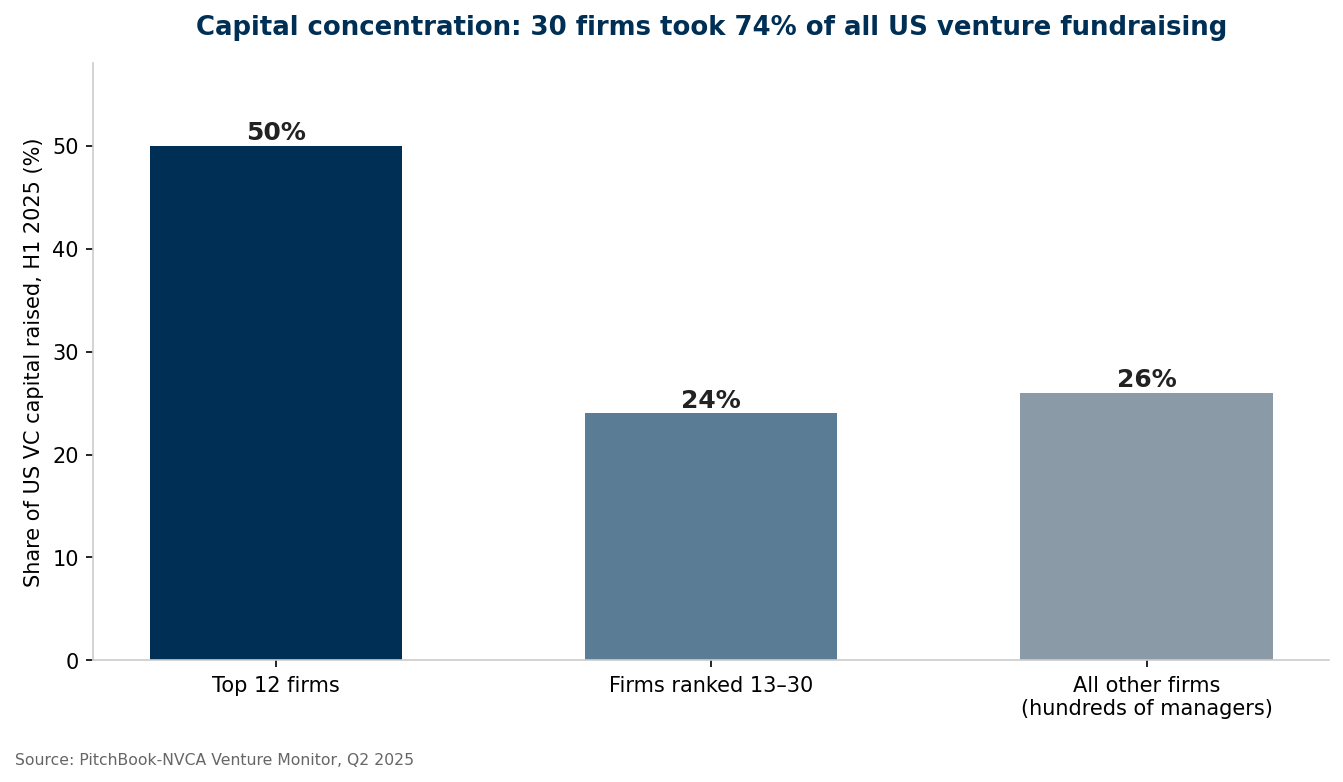

According to the PitchBook-NVCA Venture Monitor, just 44 first-time US venture funds closed in the first half of 2025, raising a combined $1.8 billion, less than half of what a single established firm, Founders Fund, gathered on its own over the same period. Capital has concentrated dramatically: twelve firms accounted for more than 50% of all US venture capital raised in that half-year, and the top thirty took 74%, leaving hundreds of smaller and newer managers to compete for the remaining quarter. The median time to close a venture fund stretched to a record 15.3 months, and emerging managers’ share of overall LP commitments has stabilised at roughly 29%, down from the highs of the 2021 cycle, though showing tentative signs of recovery as fund-of-funds capital returns to the segment.

Read carefully, however, the same data contains the strategic insight. The concentration of capital in megafunds is not evidence that small funds cannot raise; it is evidence that the industry has bifurcated into two different businesses. At the top sit asset-gathering platforms whose economics depend on management fees and whose returns, mathematically, must trend towards the market. At the other end sits a growing ecosystem of micro funds and solo general partners, typically raising between $5 million and $50 million from individuals, family offices and specialist fund-of-funds rather than pension funds, competing on access and specialist judgement rather than brand. The bar for the second category is not a CV. It is proof.

What LPs actually underwrite: the four assets that replace the credential

Strip out the noise and limited partner due diligence on a first-time manager examines four things, none of which is taught at business school.

The first is proprietary deal flow. Can this manager see excellent companies before they are widely shopped, and, crucially, why? An acceptable answer is structural: a community the manager has built, an industry in which they are a recognised authority, a publishing platform founders already trust, an operator network from a previous career. Domain expertise that founders actively seek out is the single most fundable asset a new manager can hold, because it solves venture’s core problem, access, at the source.

The second is the ability to win allocations. Seeing a great company is worthless if its founders take money from a brand-name firm instead. LPs look for evidence that founders choose this manager: angel cheques that got into competitive rounds, syndicates that founders invited in, references from entrepreneurs who picked the manager’s smaller cheque over a larger one.

The third is demonstrated judgement, a track record, however assembled. This is where the modern path diverges most sharply from the credentialed one, because a verifiable record can now be built without ever holding a fund job: through personal angel investments, special purpose vehicles, syndicate leads and scout cheques, each with auditable entry prices and markups. A portfolio of fifteen to twenty-five angel or SPV positions over three to five years, with sensible entry valuations and a handful of meaningful markups, is the de facto CV of the emerging manager class.

The fourth is operational credibility: evidence the manager can run a regulated investment business, fund administration, legal structure, LP reporting, reserves policy and pacing discipline. This is the one genuinely learnable, hygiene-level component, and the ecosystem that has grown around emerging managers (specialist fund administrators, standardised fund documents, accelerator programmes for general partners) has reduced it from a barrier to a checklist.

Notice what is absent from the list. At no point does an LP’s underwriting model award points for a finance degree. The degree was only ever a proxy for these four assets, and a proxy is unnecessary when the real thing can be demonstrated directly.

The route map the data supports

The careers of successful non-traditional managers, and the structure of LP due diligence, converge on a staged path. It is slower than the mythology of venture suggests, and far more accessible.

Stage one is building visible domain authority, typically over one to three years. Pick the market where you hold genuine informational advantage, the industry you have worked in, written about, sold into or built within, and become publicly, verifiably expert in it. Publish research. Convene the community. Be the person founders in that niche call first. This stage costs little money and compounds quietly; it is also where a media platform, newsletter or industry publication becomes a strategic asset rather than a sideline, because audience is deal flow in waiting.

Stage two is building the track record, usually overlapping with the first. Begin with personal angel cheques at whatever scale is responsible, then graduate to syndicates and special purpose vehicles, which allow a manager to invest other people’s capital deal by deal, building both an auditable record and a base of backers who already trust their judgement. Many of today’s solo general partners raised their first fund substantially from the very individuals who had invested in their SPVs. Deal-by-deal vehicles also teach the unglamorous craft, allocation negotiation, diligence under time pressure, LP communication, that a fund will demand at scale.

Stage three is the fund itself, and the data argues for restraint. The evidence on small-fund outperformance, and the advice of the LPs who specialise in the segment, points to debut vehicles sized to what the manager can credibly deploy with edge, frequently $5 million to $30 million for a solo GP, rather than the largest number the market might tolerate. A focused, modestly sized Fund I with a sharply articulated thesis is both easier to raise and easier to return, and Fund II is raised on Fund I’s discipline.

Two practical notes belong in any honest version of this map. First, regulation: a fund manager in the United Kingdom will typically operate under Financial Conduct Authority authorisation or as an appointed representative of an authorised firm, while a US manager will usually rely on the venture capital fund adviser exemption and private placement rules; in both cases the structures are well-trodden and specialist counsel is non-negotiable, but neither regime requires any particular academic qualification. Second, economics: a sub-$20 million fund generates modest management fees, and most solo GPs treat Fund I as an investment in a franchise rather than a salary, a fact worth confronting before launch rather than after.

The thesis is the credential: why specialists are winning

If there is a single thread connecting the managers who succeed on this path, it is specificity. The PitchBook finding that specialist funds outperform generalists across return metrics is mirrored in fundraising: the first-time vehicles that still close in a difficult market are overwhelmingly those with a distinct, defensible thesis and a manager whose background makes them the obvious person to execute it.

This is the deeper sense in which the MBA question misses the point. A generalist seed fund run by a well-credentialed ex-banker is, to a limited partner, an undifferentiated product in an oversupplied market. A focused fund run by someone with a decade of lived authority in a specific vertical, climate hardware, fintech infrastructure, healthcare workflow, defence software, is a unique instrument for accessing deals the LP cannot otherwise reach. The credential of the next decade of venture capital is founder-relevant expertise, and it is earned in industries, communities and operating roles, not classrooms.

The same logic explains why the demographic profile of new managers is broadening. Programmes that train and launch first-time GPs now report cohorts drawn from operators, engineers, scientists, marketers and community builders, people whose qualification is the network and knowledge their previous career created. The industry’s own data, from the partner-background studies to the vintage-year return tables, suggests this is not a dilution of standards but a return to venture capital’s original logic: backing informed conviction wherever it resides.

The maths of a small fund: why the economics favour outsiders

It is worth pausing on the arithmetic, because the economics of fund size explain both why emerging managers outperform and why the credentialed establishment largely ignores the segment in which they operate.

Consider two funds investing in the same market. The first is a $25 million debut vehicle writing initial cheques of around $400,000 into pre-seed and seed rounds, building a portfolio of perhaps thirty companies with reserves for follow-on. The second is a $1.5 billion multi-stage platform. For the small fund, a single portfolio company exiting at $250 million, an outcome that occurs hundreds of times in a typical cycle, can return the entire fund several times over from one position, assuming a sensible entry valuation and ordinary dilution. For the large platform, the identical outcome is a rounding error: its model only works if it repeatedly accesses the handful of generational companies that reach valuations in the tens of billions, an access game in which brand, cheque size and political capital decide the winners.

This is why the two ends of the industry are not really competitors, and why a newcomer’s lack of brand matters far less than the mythology implies. The micro fund does not need to beat Sequoia to a decacorn; it needs to be earliest and most useful in a market it understands better than anyone deploying at scale possibly can. The return tables reflect this division of labour: small specialist funds harvest the broad middle of the outcome distribution that the giants are structurally unable to monetise, which is precisely why 91% of the annual top-ten performers across 2013–2022 managed less than $250 million.

The same arithmetic, however, imposes discipline on the manager’s own finances, and the data-driven view requires saying so plainly. A $15 million fund charging a conventional 2% management fee generates roughly $300,000 a year before fund expenses, legal, administration, audit and travel, typically leaving a solo general partner a salary well below what they could earn in industry. The real compensation of a first fund is carried interest that arrives, if at all, seven to twelve years later, plus the franchise value of a successful Fund I. The managers who navigate this best treat the debut fund as the foundation of a decade-long business, keep personal burn low, and frequently sustain themselves through adjacent income, advisory work, an existing business, or a media and research platform that doubles as the fund’s deal-flow engine. Far from disqualifying them, that hybrid structure often strengthens the LP case, because it demonstrates the manager can survive the fund’s long liquidity cycle without mis-sized fees.

The rise of the solo GP: the structural shift in the data

The most consequential change in venture’s structure over the past decade barely registers in headline fundraising statistics, because it happens at sizes the headlines ignore: the normalisation of the solo general partner and the micro fund as a recognised, investable category.

The infrastructure tells the story. Ten years ago, launching a fund meant bespoke legal work measured in six figures and a back office assembled from scratch. Today, standardised limited partnership documents, specialist administrators serving sub-$50 million vehicles, banking and cap-table platforms built for fund operations, and rolling fund structures that allow quarterly capital raising have collapsed the operational cost of entry. Accelerator-style programmes for emerging general partners now graduate cohorts of first-time managers each year, and their published cohort data shows exactly the demographic the credential myth excludes: operators from technology companies, technical founders, sector specialists from healthcare, climate and defence, and community builders whose qualification is trust within a founder population that traditional firms systematically overlooked.

Limited partner behaviour has followed the infrastructure. Dedicated emerging-manager programmes now exist inside institutional allocators; fund-of-funds vehicles raised specifically to back first- and second-time managers have returned to the market after the post-2021 freeze; and family offices, the natural first institutional cheque for a debut fund, given their flexibility and appetite for direct access, report growing intent to back new managers as a route to deal flow they cannot reach through megafund commitments. The segment’s share of LP inflows, stabilising near 29% of a smaller overall pie, understates the depth of this specialised capital because much of it never appears in headline fundraising data at all: SPVs, rolling funds and sub-$10 million vehicles frequently go unreported.

For the aspiring manager without a conventional pedigree, the strategic meaning is significant. The category they would enter is no longer an anomaly requiring explanation. It is a recognised asset class niche with its own benchmarks, its own LP base and its own performance literature, one in which the absence of an MBA has never once appeared as a diligence criterion, and in which the presence of authentic, narrow, founder-relevant expertise appears in virtually every successful raise.

What this means for each side of the table

For aspiring managers, the synthesis is straightforward, if demanding. The data removes the false barrier, no degree stands between you and a fund, and replaces it with a real one: several years of deliberate work building authority, access and an auditable record in a market you genuinely know. The market is brutal for undifferentiated newcomers and surprisingly navigable for specialists with proof.

For limited partners, family offices especially, the evidence cuts against the instinct to equate safety with brand. The vintage-year data shows the top of the return distribution persistently populated by small, early funds, and family offices’ growing willingness to back emerging managers reflects a sober reading of that record rather than appetite for risk. The discipline lies in selection: underwriting deal flow, win-rate and judgement with the same rigour the best managers apply to founders.

And for founders, the rise of the non-traditional manager is largely good news. Investors drawn from operating and domain backgrounds tend to compete on usefulness rather than fund size, and the data on founder choice suggests that is increasingly how competitive allocations are won.

Conclusion: the data’s verdict

Venture capital has spent decades wrapped in a credentialed mystique that its own numbers do not support. Half its partners have no MBA. Most of its best funds, year after year, are run by managers near the start of their fund careers, deploying small pools of capital with specialist conviction. The gate that matters is not academic; it is evidential, and the tools for assembling that evidence, from angel syndicates to publishing platforms to standardised fund infrastructure, have never been more available.

The honest summary of the data is this: an MBA will not raise your fund, and the absence of one will not stop it. What raises a first fund is proof, of access, of judgement, of a market edge no generalist can replicate. Build the proof, size the fund to the edge, and the credentials question answers itself.

Insights & Answers

Do you need an MBA or finance degree to start a venture capital fund?

No. There is no regulatory or academic qualification required to become a general partner. Crunchbase News analysis found only 51% of VC investment partners hold an MBA, and LP due diligence on first-time managers centres on deal flow, track record, the ability to win allocations and operational readiness, none of which depends on a degree.

Do first-time venture funds really outperform established ones?

The evidence consistently supports it. Cambridge Associates data shows a majority of top-quartile funds in a typical vintage year are raised by emerging managers, and its 2004–2016 vintage analysis found 53% of annual top-ten funds were first or second funds. The Kauffman Foundation found first-time funds outperformed established firms by 3.1 percentage points annually over 1997–2011. The caveat is wider dispersion: emerging managers populate both tails of the return distribution.

How much money do you need to raise for a first VC fund?

The data favours starting small. Of the annual top-ten performing venture funds between 2013 and 2022, 73% were under $100 million, and most debut solo-GP vehicles close between $5 million and $30 million. Fund size should match the manager’s demonstrable edge and deployment capacity rather than ambition.

How do you build a track record before having a fund?

Through personal angel investments, syndicates and special purpose vehicles, which create an auditable record of entry prices, markups and realised outcomes. A coherent portfolio of fifteen to twenty-five such positions over several years, alongside visible domain authority in a specific market, is the standard evidence base on which modern first funds are raised.