A merchant in Brooklyn opens a new bakery, downloads a checkout SDK on a Tuesday and takes a card payment by Wednesday morning. That timeline used to belong to enterprise treasury projects. In 2026 it is the baseline expectation, and the payment service providers that deliver it consistently are the ones taking share at the expense of every legacy acquiring footprint in the US market.

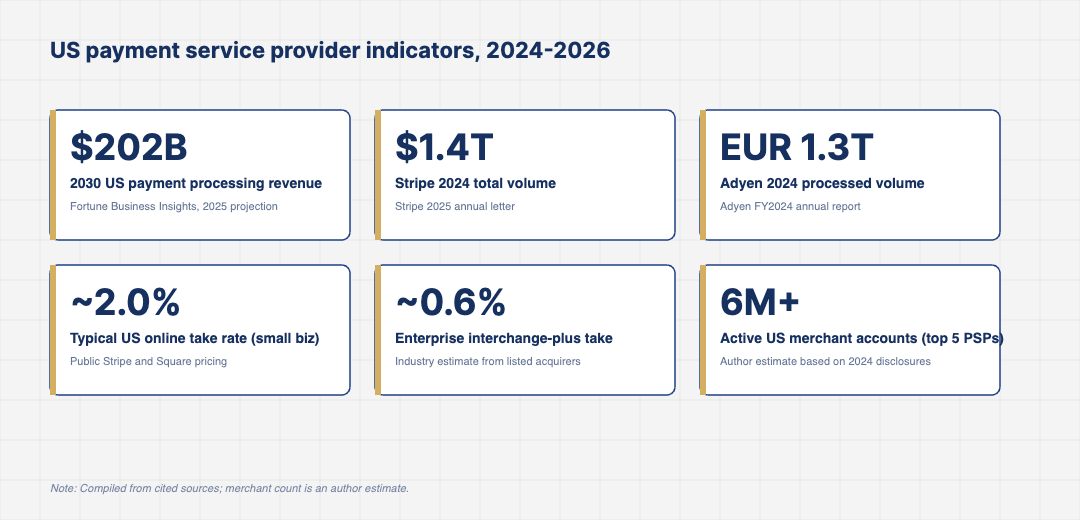

US merchant acquiring revenue is on track to exceed $202 billion in payment processing fees by 2030, growing at a compound annual rate near 14%, per Fortune Business Insights. The share captured by modern PSPs has crossed the half-way mark on net new merchant additions, and the gap between integrated software-led acquirers and the older referral-driven ISO model is now wide enough to show up in quarterly earnings rather than only in trade press commentary.

Stripe and Adyen Set the Top of the Market

Stripe disclosed $1.4 trillion in total payment volume in 2024, growing roughly 38% year over year, per the company’s annual letter. Adyen reported EUR 1.3 trillion in processed volume in its FY2024 results, with North America its fastest-growing region. The two companies operate at very different ends of the merchant spectrum, but both have made the same product bet: deep, opinionated, multi-currency platform offerings that abstract the underlying acquirer, processor and scheme layers from the merchant entirely.

That bet is what is reshaping the rest of the market. Standalone processors and traditional ISOs cannot match the depth of integration that Stripe and Adyen ship by default, and the merchants they are courting expect API-first onboarding, hosted compliance and same-day pricing changes. The longer this gap holds, the more reasonable it becomes to view the modern PSP layer as the new acquiring baseline in the US, with everything else as a long tail.

The Mid-Market Is Where the Margin Sits

The micro-merchant segment is largely flat-rate priced and dominated by Square, PayPal and a handful of vertical platforms. The enterprise segment runs on interchange-plus and is dominated by a small number of acquirers competing on a few basis points. The mid-market, broadly merchants doing $1 million to $250 million in annual card volume, is where pricing, product depth and integration value still meet, and it is the segment where most PSPs are now putting their go-to-market spend.

The reason is straightforward economics. Net take rates in this band still sit between 1.2% and 1.9% depending on mix, and the volume per merchant is enough to support real account management. The PSPs that build serious mid-market sales motions, with vertical-aware onboarding and treasury connectivity, are pulling merchants off legacy acquiring footprints faster than the incumbents can re-platform. That trend is not subtle in the 2025 earnings commentary at the listed processors.

What makes the mid-market harder to serve than it looks is the fragmentation in software stacks. A regional restaurant chain may be running a 1990s POS system at the table, a 2020s loyalty platform on the mobile, a generic accounting suite on the back office and a separate ecommerce store for catering. The PSP that can land in this environment and unify the data is the one that gets to keep the merchant, and most legacy acquirers do not have the integration depth to do it cleanly.

Why Vertical-Embedded Acquiring Keeps Compounding

Toast in restaurants, Mindbody in fitness, ServiceTitan in trades, ShipMonk in commerce. Vertical software platforms with integrated payments have become a dominant on-ramp for new merchants in their categories, and the merchants that come in through these platforms tend to stay in them. The PSP behind the platform earns the acquiring economics, the platform earns a share, and the merchant never sees a separate processor relationship.

The dynamic is now so well established that several mid-tier traditional acquirers have repositioned as platform-enablement partners. They sell capacity to vertical SaaS companies wholesale, take a thinner margin and grow volume through the platform’s distribution rather than through their own sales motion. Whether this rescues their long-term economics or simply delays the share shift will become clearer through 2026 as platform consolidation accelerates.

The platform-economics piece is also unusually durable. The platform owns the merchant onboarding experience, the day-to-day reporting screen and the customer support contact. A merchant that wants to switch acquirer for slightly better pricing has to leave the software they use to run their business, which most merchants find harder than absorbing a few extra basis points. That switching cost is the underwriting of the entire embedded-payments model and is why platform-led acquirers see materially better retention than traditional ones.

Where the Listed Acquirers Are Pushing Back

Fiserv, FIS, Global Payments and Worldpay together still handle a very large share of US card volume, and they are not standing still. The first investment area has been API and developer experience modernisation, with each company shipping a more credible REST API and SDK story than the last. The second has been ISV partnership programs, where the goal is to win new platform business before it lands at Stripe or Adyen by default. The third has been M&A, particularly tuck-in acquisitions of vertical software companies that bring captive merchant footprints.

The hard part for the listed acquirers is cultural. Long sales cycles, contract-led pricing and slow product release rhythms remain features of how they operate, and the modern PSP segment treats those as competitive advantages of the disrupting side. The most credible turnaround stories so far have come from leadership teams willing to break some of the old patterns inside the listed companies; the laggards risk being squeezed in the mid-market just as they are losing the small-merchant tier to embedded platforms.

One quieter line in the listed-acquirer playbook is rationalising the back-book of small merchants on flat-rate plans. Several of the listed acquirers now report that they are deliberately re-pricing or letting go of unprofitable micro-merchant accounts as a way to shore up margin, while reinvesting the freed-up servicing capacity into mid-market sales coverage. That approach buys time but does not solve the structural problem, and it tends to attract attention from the disclosure side because it shows up as merchant-count declines in quarterly reporting.

Where the 2026 PSP Spend Is Concentrating

Three engineering areas absorb most of the new PSP investment. The first is orchestration, where a merchant can route a payment between acquirers, alternative payment methods and BNPL providers based on cost, conversion and risk in real time. The second is tokenisation and stored-credential management, which sits behind every recurring billing and subscription product. The third is fraud and authentication, which has moved from rules to model-driven scoring fed by network token data and behavioural signal.

None of those investments produce a marketing moment. They show up as fractional improvements in authorisation rates, smaller chargeback ratios and slightly tighter spreads on the acquirer’s own funding cost. The PSPs that compound those gains across the next 24 months are the ones that will hold their take rates while the rest of the market accepts compression, and they are also the ones best positioned for the next round of cross-border and stablecoin-adjacent payment volume that is starting to enter the US merchant conversation.

For operators and investors tracking the US payment service provider segment through 2026, the practical signal is to watch net new merchant additions in the mid-market band, the share of revenue coming from value-added services beyond acquiring and the take-rate trajectory on the largest disclosed cohorts, because those three together will explain why some PSPs are widening the gap and others are losing it.

The competitive ceiling for the next two years is set by which providers can convert orchestration, tokenisation and fraud capability into a clear merchant cost-of-acceptance story rather than treating those features as engineering line items, and the providers that get that message right will absorb the bulk of the volume that is still in motion across the US market.