Open a phone, tap a contactless reader, and the transaction lands in a merchant’s bank within seconds. That speed is now expected at point of sale, and in 2026 it is reshaping the technical stack behind every dollar that moves through the US payments system. Issuers, acquirers and platform processors are spending most of their build budget on the parts of the rails that consumers never see, and the engineering trade-offs they are making now will set the cost structure for the next three to five years.

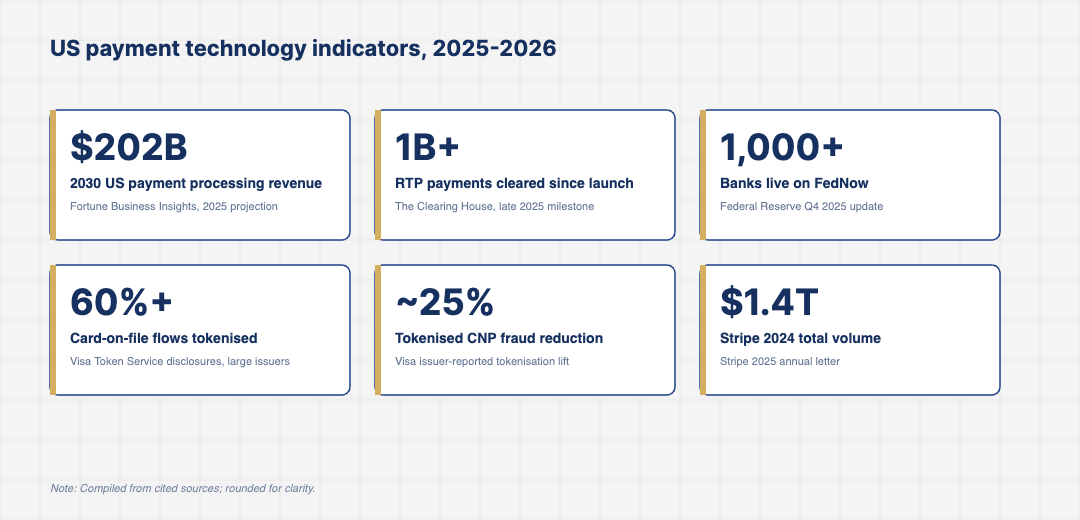

The US payments market is projected to reach roughly $202 billion in payment processing revenue by 2030, growing at a compound annual rate near 14%, according to Fortune Business Insights. Card networks, real-time rails and tokenisation vendors are absorbing most of that uplift, and the gap between processors that ship modern APIs and those that do not is widening fast. Treasury teams, fraud teams and merchant-services teams are all reorganising around the same set of building blocks, even when their internal road maps still describe the work in older language.

Real-Time Rails Have Crossed the Adoption Line

The Clearing House’s RTP network reached more than 1 billion payments cleared since launch by late 2025, with daily volume rising past 1 million transactions on peak days. FedNow, which the Federal Reserve launched in mid-2023, added more than 1,000 participating banks by the close of 2025, per the Federal Reserve’s quarterly update. Both networks now reach a credible majority of US deposit accounts on the receive side, even though send-side coverage at smaller community banks is still climbing.

The headline numbers obscure where the value sits. Most US consumer payments still ride card rails. What real-time has done is take adjacent flows, payroll top-ups, insurance disbursements, merchant payouts, and pull them off ACH’s overnight cadence. Treasury teams at mid-market firms now expect intraday settlement as a default, and that expectation is rebuilding the cash-management product roadmap at every major bank. The most-cited use case in 2025 was insurance claim disbursement, where carriers reported that real-time payouts cut customer service contact volume by double-digit percentages and reduced cost-to-serve on small-dollar claims.

Orchestration layers that sit above the rails are now where most banks are spending engineering time. The decision of whether a given payment routes via RTP, FedNow or same-day ACH used to be a procurement choice. It is now a per-transaction routing call that takes into account recipient eligibility, network operating hours, fee structure and risk score, and the platforms that do this well are quietly turning real-time into a profit centre rather than a cost line.

Tokenisation Is Now the Default, Not the Upgrade

Network tokens replaced more than 60% of card-on-file transactions at large US issuers in 2025, according to Visa’s tokenisation product disclosures. Mastercard reports comparable figures for its own token vault. The shift carries two operational consequences that merchants are still absorbing, and both of them hit revenue lines rather than cost lines.

First, refresh rates on stored credentials no longer rely on customer action. When a card is reissued, the token updates silently. Failed authorisations on recurring billing have dropped roughly 3 to 5 percentage points at large subscription platforms, which translates directly into retained revenue. Second, fraud liability shifts under the network token framework, which has nudged smaller processors toward integration even when the engineering work is non-trivial. Issuer teams report that fraud rates on tokenised card-not-present transactions sit roughly 25% below pan-based equivalents, which is now the dominant reason cited for prioritising token adoption.

For merchants who built their billing systems before tokenisation was widely available, the migration path has been the harder part. Vault providers and processors have introduced bulk-conversion services that map existing card-on-file records to network tokens without re-prompting customers, and adoption of those services accelerated through 2025. The merchant-side prize is a quieter, less visible one: fewer chargebacks, fewer fraud disputes, and a lower share of involuntary churn from declined renewals.

Card Networks Are Quietly Re-Pricing Risk

Interchange remains the largest single line item for most merchants accepting cards, and the network rules around it have been tightening. Visa and Mastercard adjusted hundreds of interchange categories across 2024 and 2025, raising fees on some card-present transactions and trimming them on tokenised e-commerce flows where fraud signal quality is higher. The detail sits in the network operating bulletins rather than in headline press releases, which is why most merchants only see the changes show up on their monthly residuals.

The result is a slow re-weighting of how processors price their merchant portfolios. Interchange-plus pricing, once the preserve of large enterprise accounts, is now reaching merchants in the $1 million to $10 million annual volume tier. Flat-rate processors, particularly those serving micro-merchants, are absorbing more of the rule changes themselves rather than passing them on. That decision has been a marketing choice in the short term and a margin compression problem in the long term, and it is starting to show up in earnings commentary at the listed processors. Larger acquirers have begun rebuilding their pricing engines to model interchange shifts in close to real time, rather than refreshing rate cards on a quarterly basis.

Why Embedded Payments Keep Pulling Volume off Standalone Processors

Stripe, Adyen and a handful of platform-led acquirers continue to take share from traditional ISO and processor footprints. Stripe processed $1.4 trillion in total payment volume in 2024, up roughly 38% year over year, per the company’s annual letter. The pattern repeats at Adyen and at platform-embedded providers serving vertical software vendors, with both reporting volume growth well ahead of the underlying market.

The driver is integration depth, not headline price. Vertical SaaS platforms, from veterinary clinic software to short-term rental managers, can now route payments without their customers ever choosing a processor. The merchant onboarding step disappears, KYC happens inside the platform, and the platform takes a margin on each transaction. Standalone processors competing on rate alone have very little room left to pull merchants back, and most have responded by either building their own platform integrations or by selling capacity wholesale to other platforms.

The model also reshapes data flow. Embedded acquirers see line-item invoice context, payout schedules and customer churn signals that a standalone processor never sees, which feeds back into both underwriting and risk pricing. That data advantage compounds quickly, and it is what makes the embedded segment difficult for incumbents to displace through pricing alone. By 2026, several mid-tier ISOs have started selling themselves as platform-enablement partners rather than as merchant-services brands, a shift that would have been unthinkable five years ago.

Where the 2026 Spend Is Concentrating

Three engineering areas are absorbing most of the new payment-technology spend at US issuers and acquirers. Tokenisation infrastructure and network-token vault integration sits at the top, followed by real-time rail orchestration that lets a single API choose between RTP, FedNow and same-day ACH on price and recipient eligibility. The third area is fraud-decision modernisation, where teams are replacing rule engines with model-driven scoring that consumes device, behavioural and network-token signal together.

None of those investments produce a marketing moment. They show up as fractional improvements in authorisation rates, fewer customer service tickets on declined transactions and a slow tightening of fraud losses. The processors that compound those gains across the next 24 months are the ones that will hold pricing power when the next round of network rule changes lands, and they are also the ones that will hold the merchant relationship when the next wave of embedded platforms tries to displace them.

For finance leaders and operators tracking the sector through 2026, the practical signal is to watch where authorisation rates, real-time send-side coverage and tokenised volume curves are moving inside their own portfolios, because those internal metrics will lead public earnings commentary by several quarters and will tell you which providers are widening the gap on the rest of the market.