Inside Charles Schwab’s San Francisco offices a few years ago, the most productive engineering team did not actually work for Schwab. It worked for a four-person fintech in Charlotte that had won a partnership pitch the previous quarter. That pattern, of an incumbent renting outside builders to ship faster than its own roadmap allows, has now become normal across US banking. According to several industry surveys, North American financial institutions now spend more on partnerships, accelerators and fintech investments than they do on their own internal innovation labs.

What open innovation actually means in US finance

Open innovation in finance is a working arrangement, not a label. The bank owns the customer relationship, the licence and the balance sheet. An external partner ships product, data infrastructure, or specialised models. The two sides operate under a commercial agreement that gives the bank distribution and the partner scale, and the regulators see a single, accountable institution.

Henry Chesbrough coined the term in 2003, but the practical version in US banking is more recent. The cluster of partnerships that defined the 2018 to 2022 period (Goldman with Apple, JPMorgan with Plaid, BBVA with Azlo, the BaaS programmes run by Cross River, Sutton and Evolve) crystallised a model that did not exist when Chesbrough wrote.

The model rests on a simple cost equation. Banks have customers, regulatory permissions and capital. Startups have engineering velocity and a willingness to specialise narrowly. Almost any modern product (a new card programme, a Treasury yield account, a cross-border payment feature) can be shipped faster by combining the two than by either side building alone.

Why incumbents stopped trying to build everything in-house

For a long stretch in the 1990s and 2000s, US banks defaulted to building. JPMorgan, Bank of America and Wells Fargo each ran technology budgets larger than the GDP of small countries, and the cultural assumption was that any capability that touched a customer should be home-grown. That assumption has eroded.

Three forces accelerated the shift. The first was the developer experience gap. By the late 2010s, the API quality of Stripe, Plaid, Marqeta and a few dozen other vendors was visibly better than what large banks could ship from their own engineering organisations. Once a bank’s product team had used a Stripe SDK over a weekend, the comparison was unforgiving.

The second was regulatory clarity around bank-fintech partnerships. The OCC, FDIC and Federal Reserve issued joint guidance in 2023 covering third-party risk management, and that document gave general counsels enough comfort to greenlight programmes that compliance teams had been blocking for years. The US payment rails most fintechs sit on are the same rails the banks operate, which made partnership simpler than competition for both sides.

The third was capital allocation. Boards started asking why a bank with a $3 billion technology budget was building features that a fintech with $30 million could ship in eight weeks. The answer increasingly was that it should not.

The same dynamic plays out at smaller institutions. Most US credit unions cannot fund a serious internal engineering team, so their entire product roadmap is now a partnership roadmap. Fiserv, Jack Henry and Q2 operate the largest of these partnership programmes, and the CUSOs (credit union service organisations) layered on top sometimes look more like venture studios than utility software companies. The economics work because the partnership cost is amortised across the entire participating membership rather than carried by any single institution.

The numbers behind the partnership wave

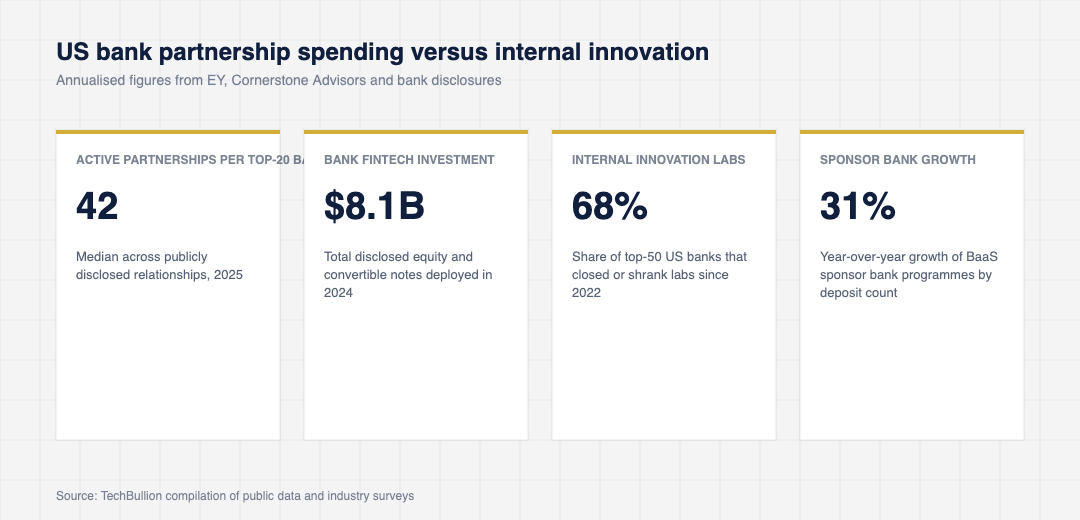

The scale of the shift is visible in spending data and disclosed partnership counts. Some of the most useful figures come from public disclosures and recurring industry surveys conducted by EY, Cornerstone Advisors and KPMG.

The pattern is consistent across asset tiers. Top-twenty US banks each report multiple dozens of active fintech partnerships. Regional banks below $50 billion in assets often run leaner internal innovation functions and instead route through partnership platforms or fintech sandboxes. Community banks operate the deepest partnership relationships of all, because their economics simply do not support in-house engineering teams of the scale required to ship competitive consumer features.

The internal partnership team at a large bank typically has three sub-functions. A discovery function scouts and triages incoming fintechs, often via accelerator programmes or scout networks. A diligence function runs vendor risk, information security, BCP and model risk reviews. A commercial function handles term sheets, revenue share, exclusivity and renewal mechanics. Founders who walk into the bank without understanding which of those three teams owns each step of the process tend to lose three months relearning it on the job.

What founders should actually understand about the partnership model

The most common mistake fintech founders make is treating bank partnerships as a sales motion. They are not. A bank partnership is a regulatory and operational integration that happens to begin with a commercial conversation. The founders who close these deals tend to walk into the first meeting already understanding the bank’s third-party risk programme, its core banking platform, and the specific compliance officer who will block the deal if she is not consulted early.

The other common mistake is underestimating timeline. From a first introduction to a live, production partnership at a top-50 US bank, twelve to eighteen months is typical. Smaller community banks can move in six months. Either way, the diligence stack (information security review, vendor risk assessment, BCP testing, model risk validation if AI is involved) is substantial. Founders who treat this as paperwork lose the deal. Founders who treat it as the actual product win.

Inside the bank, the most important relationships are not at the top. They are with the head of payments operations, the BSA officer, the chief technology officer for retail, and the line-of-business owner who has revenue pressure. When those four people are aligned, the CEO sign-off is procedural. When they are not, the CEO cannot save the deal regardless of how senior the introduction.

The ACH plumbing that quietly powers every retail product in the US is exactly the kind of detail that separates partnerships that ship from partnerships that stall.

Two warning signs separate partnerships that will ship from partnerships that will quietly stall. The first is the absence of a named line-of-business owner inside the bank. A partnership that lives only inside an innovation group rarely converts into production. The second is a procurement process that has not started by month three of the relationship. If the master services agreement has not been redlined by then, the bank is browsing, not buying.

How the next five years will reshape the partnership stack

The partnership model itself is now starting to evolve. The first generation of bank-fintech relationships was bilateral: one bank, one fintech, one product. The next generation is being built around shared platforms. Banking-as-a-service providers aggregate multiple sponsor banks and offer them to fintechs through a single integration. Industry data networks (such as the Akoya consortium for consumer-permissioned data) are doing the same on the data side.

Two regulatory shifts will define the next five years. The CFPB’s Section 1033 rule, finalised in late 2024, gives consumers a right to share their financial data through machine-readable APIs, which will force banks to standardise their data partnerships. And the OCC’s posture on novel bank charters, including the recent revival of the fintech charter conversation, is shaping how partnership deals get structured. Banking innovation that scales globally tends to be built by teams that read these two policy threads correctly.

The economic outcome of all of this is that the partnership stack is starting to look less like a procurement function and more like a portfolio. Banks now run formal venture arms, accelerator programmes, sandbox environments for technical proofs, and commercial partnership desks. The most disciplined incumbents have begun publishing partnership scorecards internally, tracking revenue, customer lift and operational risk on every relationship the same way they would track an internal product line.

None of this means in-house engineering is going away. It means the boundary between bank-built and partner-built has moved, and operators on either side of that boundary now compete on integration quality rather than feature count.

For the US community-bank fintech partnership landscape, see the Federal Reserve community-bank fintech partnerships report.