If you talked to a U.S. blockchain engineer in 2022, the dominant complaint was gas fees. If you talk to the same engineer in 2026, gas fees are no longer the bottleneck. Layer 2 rollups have absorbed the activity. Base, Arbitrum, Optimism, zkSync, Linea, Scroll and a long tail of newer chains together carry roughly 85% of Ethereum-related transaction volume by Dune Analytics counts, with the U.S. user share heavily concentrated on Base and Arbitrum. The mainnet is increasingly used for settlement, not for everyday transactions.

This shift has reorganized U.S. blockchain engineering. The questions that mattered four years ago, about sharding, about throughput limits and about MEV on a single chain, have been replaced by a different set: which rollup, which prover, which sequencer, which data availability layer. The practical implications for U.S. developers, exchanges and institutional users are large enough that the topic now sits inside engineering, treasury and compliance discussions at most American crypto-adjacent companies.

Why Layer 2 won the scaling argument in the US

Ethereum’s roadmap for scaling has, since 2021, been organized around the rollup-centric thesis articulated by the Ethereum Foundation. The idea is simple to state. Push transactions off the main chain to a second layer that handles execution at high throughput and low cost, then post a compressed proof or transaction batch back to Ethereum for settlement. The mainnet provides security. The Layer 2 provides speed.

That thesis carried the day in part because the alternative, monolithic high-throughput chains like Solana, faced their own production issues and concentration concerns. The market settled into a working compromise. Solana captured a meaningful share of consumer crypto, particularly memecoins and high-frequency activity. Ethereum-anchored Layer 2s captured DeFi, institutional tokenization, and most of the wallets that already held meaningful U.S.-based balances. Base, run by Coinbase, became the largest single venue for U.S. retail by daily active addresses in the second half of 2024 and has stayed there.

The Optimistic vs ZK rollup split, in plain terms

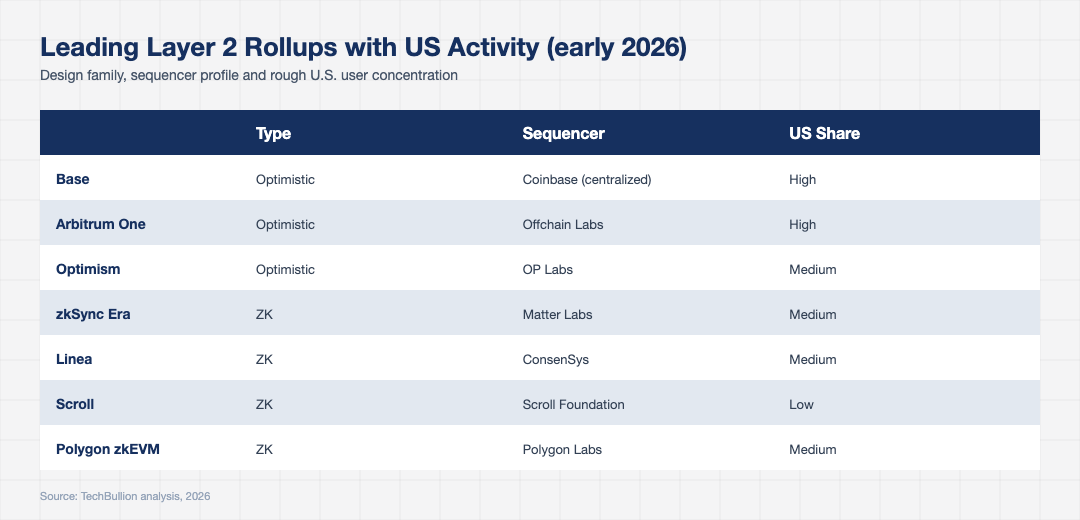

The two rollup designs in production use are optimistic rollups and ZK rollups. The shorthand is that optimistic rollups assume transactions are valid unless proven otherwise, while ZK rollups produce a cryptographic proof that they are valid. Both designs settle on Ethereum, both reduce fees by an order of magnitude or more compared with mainnet, and both have working production deployments at U.S. user scale.

The trade-offs are real but narrowing. Optimistic rollups have a fraud-proof challenge window, traditionally seven days, during which a withdrawal back to Ethereum can be contested. That window is what gives the design its security, but it adds friction to user experience. Liquidity providers stepped in to bridge the gap, offering near-instant withdrawals for a fee. By 2026 the friction is almost invisible to retail users on Base, Arbitrum and Optimism.

ZK rollups produce a validity proof on each batch, which means withdrawals back to Ethereum are effectively immediate as soon as the proof is verified on mainnet. zkSync, Linea, Scroll and Polygon’s zkEVM have all reached production with full EVM equivalence. Their proof generation costs have dropped sharply through 2024 and 2025 thanks to specialized prover hardware and more efficient proving systems. The economic gap between optimistic and ZK is narrowing fast.

How US developers actually choose between rollups

Four factors dominate the choice in 2026 for a U.S.-headquartered team. The first is user distribution. If the target user already holds a wallet on Base, the development calculus tilts heavily toward shipping on Base. Coinbase’s Wallet integration, its retail audience and its fiat on-ramp make this the path of least resistance for consumer apps. Arbitrum and Optimism remain the choice for DeFi protocols with deeper liquidity needs.

The second factor is sequencer decentralization. Most production rollups still run a single sequencer operated by the rollup’s team. That is a known concentration risk and U.S. compliance teams have flagged it during due diligence in 2025. Optimism’s plan to share its sequencer with the Superchain ecosystem, Arbitrum’s BoLD permissionless validation upgrade, and Espresso’s shared-sequencer marketplace are each addressing the issue in different ways. The teams that have made the most concrete progress here have a real advantage in institutional sales conversations.

The third factor is data availability. Each rollup must publish enough data for the underlying Ethereum chain to reconstruct its state. EIP-4844 blobs, introduced in March 2024, dropped that data cost roughly an order of magnitude. The longer-term play is offloading data to a dedicated availability layer such as Celestia or EigenDA, which Base, Arbitrum’s Orbit chains and several others now support as options. The choice matters because it directly determines transaction cost.

The fourth factor is regulatory posture. Coinbase, as a U.S. listed company, has been the most public about its rollup’s compliance considerations. Other rollup teams have followed in similar directions, particularly around OFAC sanctions handling at the sequencer level. The OCC’s 2024 guidance and the SEC’s enforcement focus on token offerings rather than infrastructure has given rollup teams enough clarity to operate, but not enough clarity to ignore.

Where institutional flow is showing up

The clearest institutional signal in 2026 is on Base, Polygon and Arbitrum, the three rollups that have signed the most enterprise integrations. BlackRock’s BUIDL fund, after launching on Ethereum mainnet, expanded to Polygon, Optimism, Avalanche, Arbitrum and Aptos in 2024 and 2025. JPMorgan’s Onyx team has run trial deployments on Polygon and an internal permissioned rollup. Visa has used Solana for stablecoin settlement pilots and has tested both Base and Polygon for cross-border settlement use cases.

Tokenized money market funds have been the loudest enterprise application. Franklin Templeton’s BENJI runs on Stellar, Polygon, Arbitrum, Avalanche, Aptos and Base, with the bulk of share class activity concentrated on the highest-throughput chains. The Boston Consulting Group’s 2025 tokenized assets report estimates that around 60% of newly tokenized U.S. fund issuance went to Layer 2 chains rather than Ethereum mainnet, a flip from the situation just two years earlier.

For retail, the most observable institutional impact is fiat on-ramp economics. Coinbase, Stripe, MoonPay and Robinhood now route most of their stablecoin issuance and consumer-facing onchain payments through Layer 2s rather than mainnet, simply because the per-transaction economics work. That is a quiet but important production proof that the rollup-centric thesis is no longer theoretical.

What US Layer 2 scaling looks like in 2027

Looking 18 months out, three trends will define the U.S. picture. The first is rollup consolidation. The market does not need 60 production rollups, and venture capital is already pulling back from undifferentiated entries. Expect a smaller number of well-funded, well-engineered rollups to capture most of the U.S. user base, with appchain-style rollups specializing for individual large applications.

The second is shared sequencing and shared security. The same logic that drove EigenLayer’s restaking thesis applies to sequencers. Multiple rollups sharing a single set of decentralized sequencers can deliver atomic cross-rollup transactions and stronger censorship resistance. By 2027 several major U.S.-relevant rollups will likely use a shared sequencer, with material implications for liquidity and user experience.

The third is the slow convergence of optimistic and ZK design. Several optimistic rollups, including Optimism and Arbitrum, are integrating ZK proofs as a faster finality layer. The end state is something most engineers expect to look hybrid, with optimistic execution combined with ZK validity proofs for faster withdrawals and stronger guarantees. That direction is no longer experimental. It is the working roadmap.

For U.S. teams building onchain in 2026, the practical takeaway is simple. The scaling problem has been solved well enough for production use, and the engineering question is now which rollup family, which sequencer, and which data availability layer fits the specific application. The infrastructure has matured to the point where most discussions are about product fit rather than about whether the underlying technology can carry the load.