In 2020, a single Uniswap swap on Ethereum could cost a US retail user more than forty dollars in gas at peak hours. Five years later, the same swap on Base, Arbitrum or Optimism settles in seconds for a few cents, and the underlying capacity of the Ethereum ecosystem has expanded by more than two orders of magnitude. The story of how that happened, and what the US institutional desks built on top of it, is the most consequential infrastructure shift in crypto since proof of stake.

What blockchain scalability actually means in 2026

Blockchain scalability has historically meant three different things, often conflated in popular coverage. The first meaning is throughput, measured in transactions per second. The second is cost per transaction, which matters more for retail use than throughput in isolation. The third is finality, which matters most for institutional settlement, because a transaction that can still be reorganised an hour later is operationally unusable for many regulated workflows.

The Layer 1 chains made progress on all three, but the breakthrough came from Layer 2 rollups. Optimistic rollups (Optimism, Arbitrum, Base) batch user transactions, settle them to Ethereum, and rely on a fraud-proof window to handle disputes. Zero-knowledge rollups (Scroll, Linea, zkSync Era, Starknet) prove correctness cryptographically and avoid the dispute window entirely at the cost of more complex cryptography. In 2026, both types are in production, both carry serious volume, and both have matured to the point where institutional users can rely on them.

The most important Ethereum mainnet upgrade behind this shift was the EIP-4844 proto-danksharding upgrade, which added a dedicated blob data space for rollups in early 2024. Per-transaction costs on rollups dropped roughly an order of magnitude after the upgrade. The trajectory through full danksharding, scheduled for the next two protocol upgrade windows, would drop costs another order of magnitude. The US payment rails fintechs sit on now intersect with rollup-based stablecoin flows for a meaningful share of B2B treasury moves.

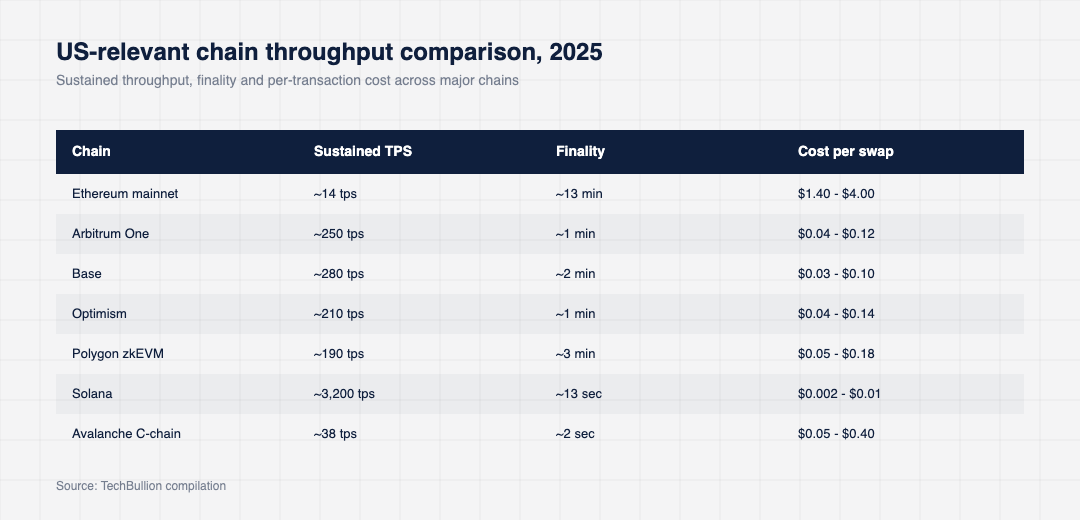

How the major US-relevant chains compare on throughput in 2026

Throughput numbers are easy to mislead with, because peak throughput in ideal conditions is a different number from sustained throughput under real load. The composite figures below pull from operator dashboards (Optimism, Arbitrum), the L2Beat dashboard, and the EVM benchmark suites maintained by the rollup teams themselves.

The headline pattern is that rollups now carry roughly five times as much US-originated activity as Ethereum mainnet does, and the gap is widening. Mainnet has become the settlement and security layer; the rollups have become the execution layer. That separation of roles was the bet the Ethereum roadmap made in 2018, and the institutional adoption now flowing into the rollup ecosystem suggests the bet has paid off.

The rollup ecosystem has also matured operationally. Most US-relevant rollups now publish daily on-chain dashboards covering sequencer uptime, batch posting cadence, fraud-proof window status and bridging throughput. Institutional desks subscribe to these dashboards the same way they subscribe to exchange status pages. The largest US custodians have also begun shipping rollup-native custody products, with multi-party computation key management and integrated tax reporting.

Where US institutions are actually using rollups in production

Three categories of US institutional activity have taken root on rollups. The first is regulated stablecoin settlement. USDC is now native on every major rollup, and the issuance and redemption patterns observed on Base in particular suggest that Coinbase’s commercial relationships have driven meaningful B2B volume there. The second is tokenised real-world assets. BlackRock’s BUIDL, Ondo’s USDY and the major short-Treasury products live mostly on Ethereum mainnet today but have started extending to rollups for cheaper subscription and redemption flows.

The third is institutional DeFi. Aave, Compound, MakerDAO (Sky) and the newer fixed-rate protocols (Notional, Pendle) all run rollup deployments alongside their mainnet versions, and US institutional desks increasingly route through the rollup deployments to keep gas costs in check. The total value locked on Layer 2 rollups crossed $50 billion in 2025 by L2Beat’s count, and the institutional share of that number is rising. ACH-based on-ramps are the practical bridge between regulated dollars and rollup-resident stablecoins for most US users.

One overlooked driver of institutional rollup adoption is data availability. The dedicated blob space introduced by EIP-4844 reduced data costs enough that publishing a rollup batch is now cheap enough for institutional issuers to consider running their own rollup for a single product line. A small but growing number of US fintechs and asset managers have started doing exactly that.

Non-EVM chains still compete for US institutional attention. Solana has captured a meaningful share of US retail crypto activity, particularly around memecoin trading and consumer payments through Solana Pay. Its sustained throughput numbers genuinely exceed any EVM environment in production today, and the institutional infrastructure around it (Anchor, Helius, Triton) has matured fast. Whether Solana can capture the same share of regulated US flow as the Ethereum rollups remains an open question, but the gap has narrowed.

The risks and trade-offs that still matter

The rollup architecture introduces specific trade-offs that US institutional users have to track. The first is the centralisation of sequencers. Most production rollups today rely on a single sequencer operated by the rollup team, and that operator can in principle censor or reorder transactions. The rollup roadmaps include shared and decentralised sequencer designs, but those are still partly aspirational in 2026.

The second is the bridging risk. Funds move between rollups and mainnet through bridges, and bridge exploits have been the largest single source of value loss in the rollup ecosystem to date. The Wormhole exploit in 2022 and the Nomad and Multichain incidents in 2023 each cost users hundreds of millions of dollars. The current generation of canonical bridges (the optimistic rollup canonical bridges, the LayerZero and Connext designs, the ERC-7281 standard) is more cautious than its predecessors, but the bridge layer remains the weakest link in many institutional risk reviews.

The third is the fraud-proof window for optimistic rollups. A seven-day window between settlement and withdrawal is operationally tolerable for many users but unworkable for others, which is why intent-based liquidity layers (Across, Hop, Synapse) have emerged to short-cut the wait at a modest cost. Banking innovation that scales globally over public chains will keep depending on how these trade-offs are managed.

Developer tooling is the under-reported story. Foundry, Hardhat, Tenderly, Alchemy and the major rollup-native testnets have made building on rollups easier than building on Ethereum mainnet was in 2020. A US fintech engineering team can ship a production rollup deployment in weeks with infrastructure that would have required quarters of custom work five years ago. The talent supply has not fully caught up, but the tooling has.

What US founders building on rollups should understand now

For a US fintech founder considering a rollup deployment, three practical considerations dominate. Pick the rollup based on the user base, not the headline benchmark. Base concentrates US retail and Coinbase-mediated flow. Arbitrum concentrates DeFi-native liquidity. Optimism has a strong public-goods funding story that has attracted certain protocol ecosystems. Polygon, Scroll, zkSync and Linea each have their own communities. The deployment that gets traction is the one that lands where your users already are.

Plan for multi-rollup deployment from the start. The single-rollup era ended quickly, and most institutional flows now move across at least three rollups during a typical workflow. Your contracts and operational runbooks should assume that complexity rather than try to fight it.

Invest in sequencer monitoring, bridge risk reviews and gas cost dashboards before you ship any production transaction. Most US fintechs that get into trouble on rollups discover, after a sequencer incident or a bridge slowdown, that they had no production visibility into the layer they were depending on. The fix is cheap and the cost of skipping it is high.

Rollups did not turn out to be the temporary scaffolding many sceptics expected in 2020. They are now the execution layer of choice for any serious US institutional activity on public chains, and the next two protocol upgrade windows will reinforce that pattern rather than reverse it.

For up-to-date TVL and security data on US-popular rollups, see L2BEAT scaling summary.