Thirty years separate the first US online banking pilot from the day mobile banking became the default interaction surface for the majority of American adults. The journey is short by the standards of most service industries, and unusually long by the standards of consumer technology. What that thirty-year arc reveals about US financial service design is more interesting than any single year inside it, because design choices that landed in 1996 and 2007 still shape how customers expect to move money in 2025.

FRAM Creative’s 2025 banking UX research describes a market where mobile-first design has decisively beaten the desktop-led patterns that defined the 1995-2014 era, and where the next frontier is voice, conversational AI, and embedded interactions inside non-banking software. The current state is the result of forty years of layered decisions made under different technology constraints, and reading those decisions in sequence is the most reliable way to anticipate what 2030 will look like for both incumbent banks and the fintechs trying to displace them.

The article that follows reads the timeline forward, explains why each shift mattered commercially as well as visually, and pulls out the three operational struggles that absorb the most senior design effort in 2025. The takeaways at the end are pointed at founders, in-house design leaders, and the broader industry, because all three audiences face the same question: what does it cost to ignore the next design transition, and how much advantage flows to whoever moves first.

How financial service design got here

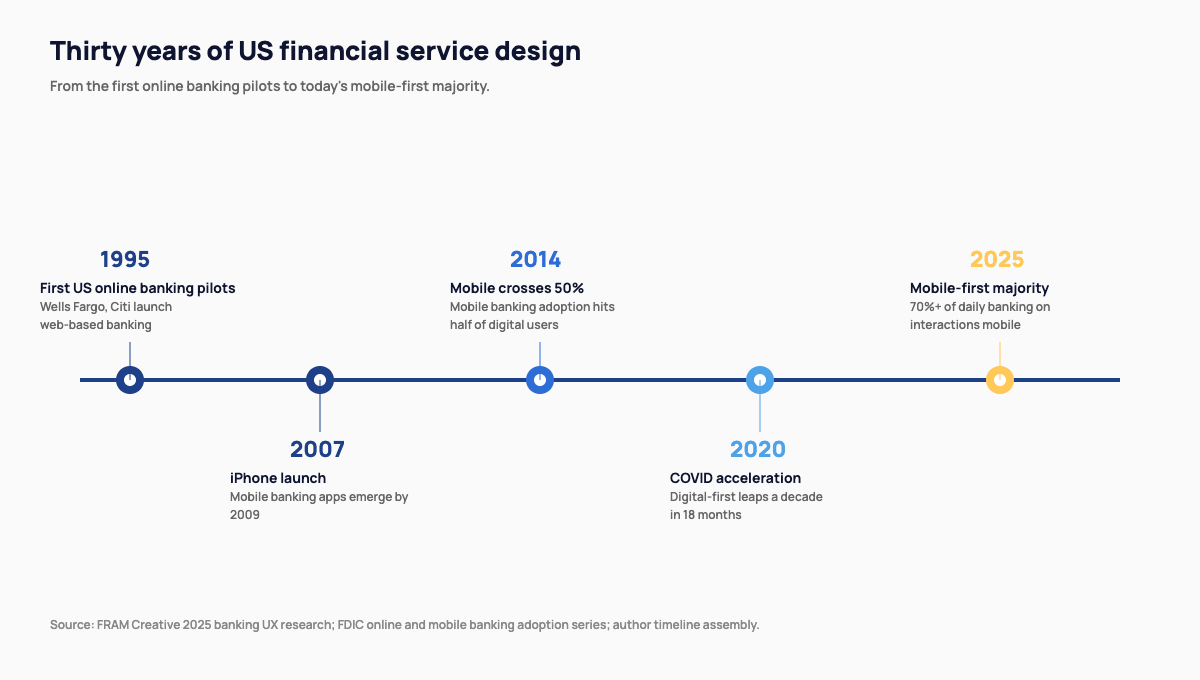

The first US online banking pilots launched in 1995, when Wells Fargo and Citibank both rolled out web-based account access for selected customer segments. The early UX was a literal port of the branch experience: account list, statement view, transfer form. The information architecture matched the bank’s internal organisation, not the customer’s mental model, and the design choice that defined the era was to optimise for completeness rather than for ease of action.

The 2007 iPhone launch did not immediately change banking design, but the consumer expectations it set did. By 2010, every major US bank had a mobile app. By 2014, mobile crossed 50 percent of digital banking interactions. The COVID period accelerated the next jump, compressing roughly a decade of digital-first adoption into eighteen months and forcing institutions to deliver experiences that no longer assumed the customer ever set foot in a branch. The 2025 state is the equilibrium that has formed after that acceleration: mobile-first as the default surface, web as a secondary surface for higher-friction tasks, and a small but growing share of voice and AI-led interactions on the edge.

Why mobile-first beating online banking matters, and the Forrester ROI claim

The shift from web-led to mobile-led design changed the unit economics of consumer banking in ways that are still reshaping product roadmaps. Mobile banking sessions are shorter, more frequent, and more transactional than web sessions. That session profile rewards interface choices that prioritise speed of action over completeness of information. The banks that redesigned for that profile early are the ones with the highest digital engagement metrics today, and the ones that ported web designs to mobile with minimal change are still paying customer-acquisition costs to win back customers they implicitly trained to bank elsewhere.

Forrester’s recurring usability research argues that every dollar invested in serious banking UX returns roughly $100 in lifetime customer value, driven by retention, cross-sell, and reduced support load. The number itself is a stylised summary of multiple studies, but the underlying claim is durable across methodologies: usability investment in financial services pays back faster than usability investment in most other consumer software categories, because the cost of a single bad experience is so much higher when money is on the line. That asymmetry is what is funding the current wave of design hiring inside US banks and fintechs, and it is also why design leadership has shifted from a marketing-adjacent function to a product-adjacent one inside the most disciplined institutions.

What design teams actually struggle with in 2025

The interesting struggles in 2025 are not the surface ones (visual polish, accessibility, dark mode, microcopy). Those have largely been solved or commoditised. The interesting struggles are operational. Three keep showing up in design-leader conversations across both banks and venture-backed fintechs.

The first is governance across legacy systems. Most banks run multiple core systems acquired through M&A activity over decades, and the customer-facing app sits on top of a backend reality that is fundamentally fragmented. Designers are increasingly responsible for hiding that fragmentation, which means the design work is often more about systems integration than about visual choice. The second is regulatory layer-in. Disclosure requirements, fair-lending text, consent flows, and accessibility minimums all compete for surface area that mobile-first design intentionally limits. Resolving that tension is where the most senior design talent now spends its time, and the teams that have built explicit patterns for it ship faster than teams that improvise per-feature.

The third is AI-assisted interactions. Conversational interfaces, agentic features, and AI-generated guidance are landing in banking apps faster than the design patterns and user-trust assumptions are catching up, and most teams are flying without an established playbook. Building a hallucination-tolerant interaction model for money movement is harder than the marketing makes it sound, and the teams that solve it credibly will set the standard for the next half-decade of consumer banking interactions.

Where the design language is heading

Three directions are visible in 2025-2026 product roadmaps. The first is conversational and voice-led interactions that handle low-cognitive-load tasks (balance check, recent transactions, simple transfers) without launching the full app. That category has been promised for ten years but is finally landing as voice models become reliable enough for financial contexts. The second is embedded design, where the same banking experience appears inside non-banking software (payroll, accounting, e-commerce checkout) and the design challenge is consistency across surfaces the bank does not directly control.

The third is AI-led personalisation, where the surface adapts to predicted customer intent rather than presenting a fixed default. That direction has obvious upside on engagement and equally obvious downside on transparency and explainability. The banks that lean into it without a serious explainability layer underneath are accumulating regulatory and reputational risk that will land somewhere in 2026-2027. The banks that build AI-led personalisation with explainability baked in from the start are positioned to define the next decade of consumer banking interaction patterns, and the design leaders shaping those decisions inside the largest institutions are now hired off design-systems and AI-research backgrounds rather than visual design alone.

What founders, design leaders, and the industry should take from the data

For founders, the practical lesson is that design quality is now a competitive necessity rather than a differentiator. A poorly-designed fintech app does not just convert badly; it actively damages the brand because customers compare it to the well-designed apps they use daily. The strategic question is not whether to invest in design but where to invest first: onboarding (highest acquisition impact), money-movement primitives (highest retention impact), or AI-led features (highest forward-looking differentiation impact).

For design leaders inside banks and fintechs, the lesson is that the senior design role has expanded beyond visual and interaction design into systems thinking, regulatory translation, and AI-experience strategy. The leaders who get budget and influence are the ones operating at that broader scope. Open innovation patterns across US finance increasingly include design as a partnership criterion when banks evaluate fintech acquisitions, and that recognition is recent enough that the operators who anticipate it are still finding leverage in it. The broader industry implication is straightforward: the next decade of US financial services will be won and lost on interaction-design decisions made in the next eighteen months, and the institutions that staff those decisions properly now will set the rules everyone else has to play by.