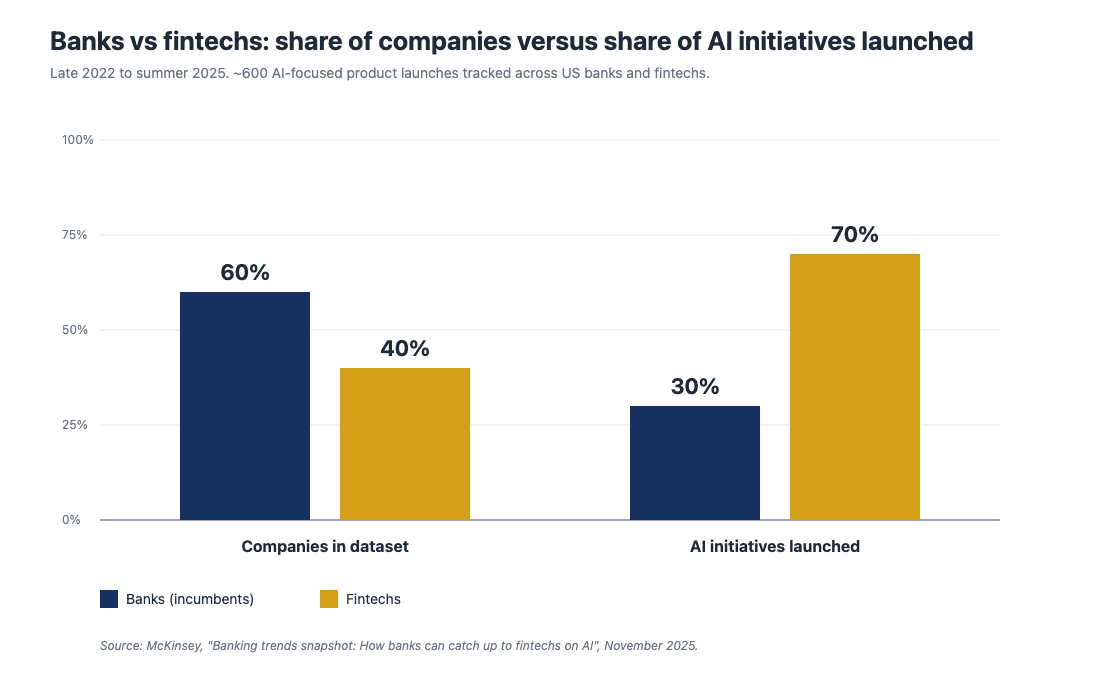

The first time a US retail bank publicly admitted it could not build something faster, cleaner, or better than a fintech partner already had, something quietly shifted in how senior banking leaders talk about innovation. It stopped being framed as an internal project to defend and started being treated as the default operating mode. McKinsey’s November 2025 banking trends snapshot describes a sector where banks have spent five years closing the AI capability gap with fintechs, mostly by partnering, licensing, and embedding rather than building from scratch.

That sets the tone for what is happening across US finance right now. The largest institutions are no longer trying to out-innovate every fintech. They are trying to absorb the right ones into the customer experience without losing the trust premium that comes with being a bank. Fintechs, on the other side, have shifted from disruption rhetoric to a more pragmatic stance: distribution at scale lives inside banks, and the path to that distribution runs through partnership rather than displacement. The result is an open-innovation operating model that looks less like a science fair and more like a procurement function.

What open innovation actually means in US financial services

Open innovation in finance is not the same as open banking. Open banking is the technical and regulatory layer, APIs, consent flows, data-sharing standards, that lets a customer’s account information move between institutions. Open innovation is the broader operating model that sits on top of that plumbing: the way a bank decides which capabilities to build internally, which to acquire, which to license, and which to consume from partners through APIs.

In practice, the largest US banks now run through a sequence of build-buy-partner decisions every quarter. Underwriting models, fraud detection, credit decision engines, onboarding flows, customer support automation, and small-business lending interfaces are all candidates for partner-supplied components rather than internal-only builds. The shift is less about who writes the code and more about who carries the regulatory, operational, and brand risk when a feature ships.

Internal benchmarks at top-five US banks now ratio those decisions roughly forty percent partner, forty percent build, and twenty percent acquire, a flip from a decade ago when build dominated. The partner share is concentrated where capability moves fastest, which means anything touching machine learning, real-time risk scoring, or customer-facing AI tooling.

Where the opening is showing up, and how big it is

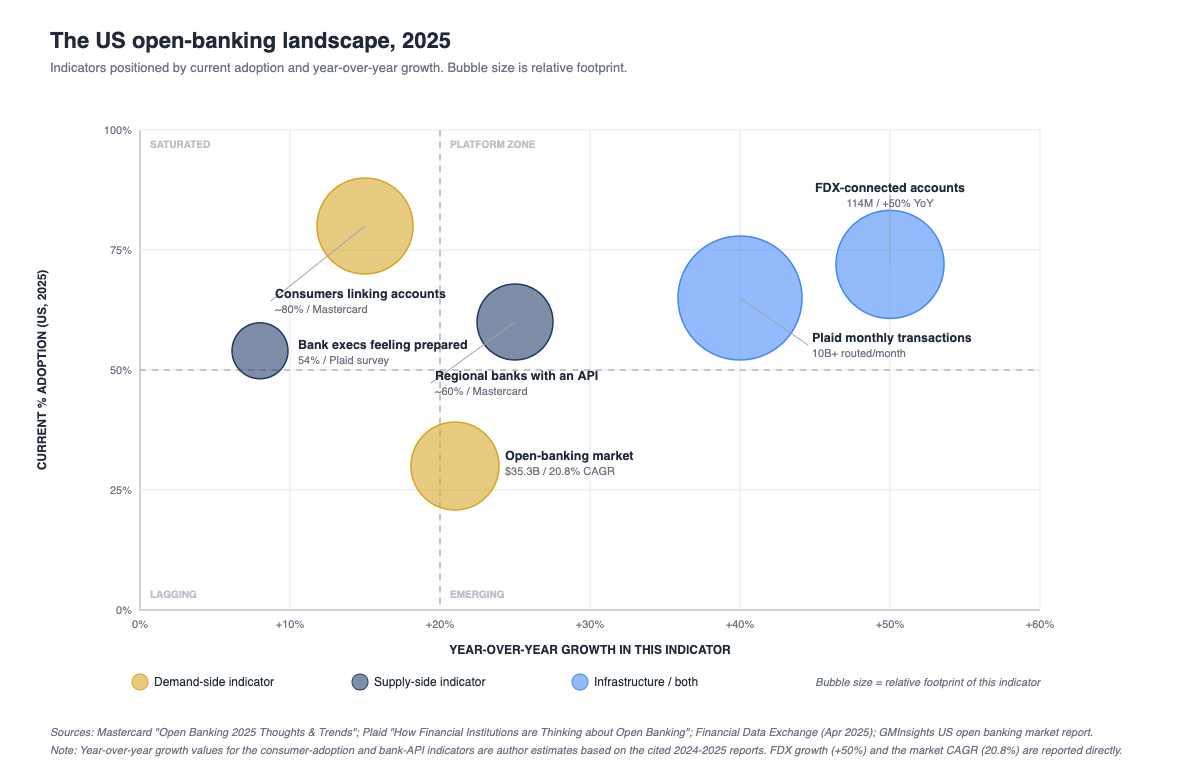

The numbers tell a clearer story than the rhetoric. Mastercard’s 2025 open banking trends report tracks a doubling of the user base for permissioned account-data flows in the US between 2023 and 2025, with a heavy concentration in lending applications, payroll-linked services, and personal financial management tools. Roughly 76 million Americans had used a permissioned open-banking connection by mid-2025, up from about 33 million in 2023.

Standards work is finally catching up to volume. The Financial Data Exchange is now the consensus interoperability layer, with API specifications adopted by most major US banks and aggregators. That shift from screen-scraping to standardised APIs is what makes the next category of partnerships possible at scale, because it gives both sides a predictable contract for data quality and uptime.

The most forward-leaning category is account-to-account payment flows. McKinsey argues open banking is the catalyst for account-to-account payments in the US, with pay-by-bank rails projected to reach 14 percent of online retail payment volume by 2028, up from less than 4 percent in 2024. That has direct implications for payment rails, merchant acceptance economics, and the role of card networks in the next stack.

What’s slowing it down

The frictions are not technical; they are commercial and institutional. Four keep showing up in deal conversations.

First, liability allocation. When a bank-fintech partnership produces a customer-facing feature, the regulatory exposure typically still sits with the bank’s chartered entity. That makes risk teams slow to approve any partnership where the underlying model, fraud, credit, KYC, cannot be inspected in detail. Several large US banks now require partner audits at a frequency that smaller fintechs cannot economically support.

Second, data ownership and reciprocity. Open banking has moved consumer data outbound to fintechs, but inbound flows, fintechs sharing analytical signals back to banks, are still rare. A reciprocal data model would unlock joint product work, particularly in lending and small-business banking, but the legal frameworks for it are not yet standardised.

Third, distribution economics. Bank-owned distribution is expensive to access. Revenue-share splits favour the bank for in-app placements, which compresses fintech unit economics and pushes startups to look for embedded-finance routes through non-bank channels, payroll providers, accounting software, vertical SaaS, instead.

Fourth, integration cost. Even when the commercial deal closes, the engineering reality of plugging a fintech component into a fifty-year-old core banking system can take twelve to eighteen months and consume a meaningful share of the partner’s runway. Founders who underestimate that timeline rarely make it to the second contract.

What founders and operators should take from the data

A clean compliance posture is now table stakes for any bank-side conversation. That means real second-line risk functions, documented model governance, and an incident-response history that survives a partner audit. The fintechs winning the largest distribution deals in 2025 invested heavily here years before they started pitching banks, and the cost of catching up retroactively tends to wipe out the gross-margin advantage that drew the bank to the partnership in the first place.

Banks are increasingly willing to license rather than build, but only if the licensed component fits inside the bank’s existing operational and data-protection frameworks. Founders building horizontal infrastructure, fraud, blockchain infrastructure for settlement, treasury automation, dispute management, have a structural advantage over those building vertical, customer-facing apps that compete directly with the bank’s own brand.

Distribution still matters more than features. The pragmatic founder builds the partnership before perfecting the product, because the data flywheel only spins inside a real customer base. Banks remain the largest and most consolidated customer base in US finance, so partnership economics, even at unfavourable revenue splits, often beat direct-to-consumer paths for any B2B fintech with a horizontal product. The trade-off is governance: every partnership commitment narrows the founder’s product-roadmap autonomy, and serious operators price that loss into their term-sheet negotiations from the first conversation.

What to watch in 2026

Three things are worth tracking over the next twelve months.

The first is how the largest US banks structure their internal fintech-partnerships function. Several top-five institutions have moved this responsibility out of innovation labs and into commercial banking lines, signalling that partnerships are now a revenue motion rather than a marketing one. That structural shift typically precedes a step-change in deal volume, because it forces partnership economics into the same P&L discipline that everything else in commercial banking already lives under.

The second is regulatory clarity around CFPB Section 1033 and how prescriptive the final rules end up being on consumer data portability. A more prescriptive rule set accelerates aggregator economics; a more permissive one favours bilateral bank-fintech deals. Either outcome reshapes which fintechs are valuable to which banks, and on what terms.

The third is the question of who owns the next layer of the stack. As account-to-account payments scale and embedded finance leaks into more non-bank channels, the open question is whether banks step up to own the full embedded experience or cede it to platform companies. The answer will shape US fintech valuations and M&A activity through the back end of the decade. The practical implication for US fintechs and incumbent banks is that partnership design now matters more than capability buildout for most growth roadmaps in 2026.