A venture investor who led a Series A in a US consumer fintech in 2019 recently described the deal as a product of a different economic era, a time when a business could raise at a ten-figure valuation on user growth alone. The investor had, in the intervening six years, watched the industry work out how it actually makes money. That reckoning, not a downturn, but a clarification, is the story of fintech economics in the United States right now. The global fintech market was valued at roughly $312 billion in 2024 and is projected to exceed $1.1 trillion by 2032, according to Fortune Business Insights. Growth continues; the question is which revenue models actually hold up.

The four revenue models that matter

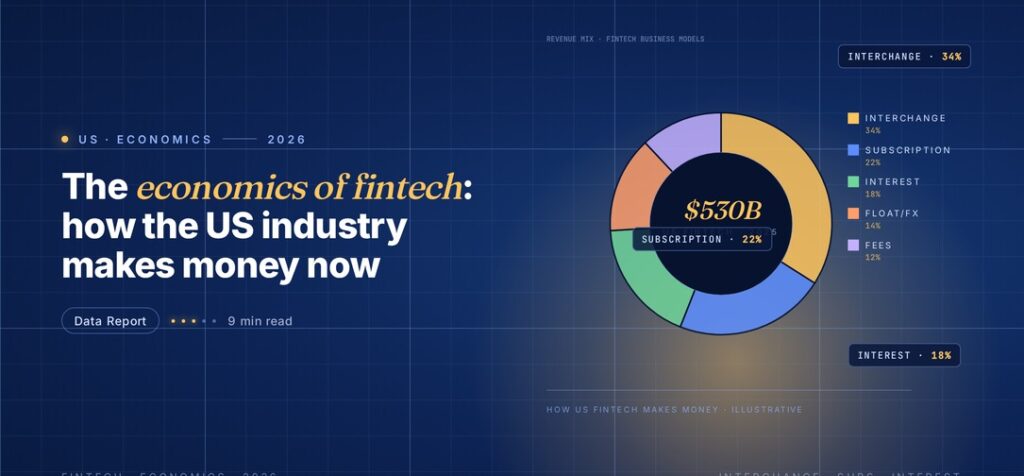

US fintechs earn money through four durable revenue models, and the relative weight of each has changed markedly over the last three years. Interchange remains the largest single line for most consumer fintechs but has declined as a share of total revenue. Net interest income and treasury spread have risen sharply as interest rates moved. Subscription and premium tiers have matured from an experimental model into a meaningful contributor at a subset of firms. Payments-and-FX revenue has grown fastest among B2B and cross-border fintechs.

The economic question that defines the US market in 2025 is which combination of the four a fintech can run at scale. A single-line business, pure interchange, pure subscription, pure net interest, has become structurally harder to defend, because any one line can be undercut by a competitor with a different cost base.

Interchange, under pressure but still the workhorse

Interchange remains the single largest revenue line for most US consumer fintechs. A neobank that routes a customer’s debit-card activity through a sponsor bank earns a share of the interchange fee merchants pay, typically around 1 to 1.5 percent of transaction volume. For a fintech with two million active users each spending several thousand dollars a month, that is a meaningful revenue stream.

The pressure on interchange in the US comes from regulatory debate and from merchant pushback. Proposed rulemaking at the Consumer Financial Protection Bureau and sustained lobbying by large retailers have kept debit interchange under review for years. The uncertainty has not moved fees materially yet, but it has forced US fintechs to plan for a world in which interchange is a smaller share of revenue than it is today. The Federal Reserve’s Regulation II framework for debit card interchange is the locus of most of that policy conversation.

Net interest income, the surprise of the cycle

The shift that most changed fintech economics in the United States is the rise of net interest income as a first-order revenue line. Between 2022 and 2024, rising US interest rates turned customer cash balances, which previously earned close to zero, into a meaningful source of spread income. Fintechs that routed deposits into yield-bearing accounts, or that offered tokenized money-market or high-yield savings products, earned material revenue simply on their float.

The same dynamic has affected lending fintechs. Unsecured consumer loan yields rose as rates moved, and while default rates also rose, the economics at prime credit tiers have stayed positive for the leading originators.

| Revenue model | 2020 share (typical US consumer fintech) | 2025 share (typical US consumer fintech) |

|---|---|---|

| Interchange | 50-70% | 20-35% |

| Net interest / treasury spread | <10% | 30-50% |

| Subscription / premium tier | 15-25% | 10-20% |

| Payments / FX / other | 5-10% | 10-15% |

Source: Fortune Business Insights and company disclosures; see the Fortune Business Insights fintech report.

The share ranges here are indicative rather than a universal pattern; individual firms vary widely. What is consistent is the direction, interchange share falling, interest-line share rising, across essentially every US consumer fintech of scale.

Subscription models: the quiet consolidation

Subscription revenue in US fintech has consolidated into two configurations that work and one that mostly does not. The configurations that work are premium consumer tiers tied to tangible features, higher yield on cash, better foreign-exchange rates, priority support, identity-theft coverage, and pure-subscription B2B SaaS sold to small and mid-sized businesses for accounting, payroll, or payments workflow. The configuration that mostly does not work is the standalone consumer subscription to a financial product without a corresponding non-fee benefit.

The most visible US fintechs running subscription models at meaningful scale, including Chime’s premium tier, Revolut’s US subscription products, SoFi’s premium account, and a long tail of SMB-focused platforms, have all converged on bundles that tie subscription price to measurable feature value rather than to an abstract membership concept. The broader digital-banking context for these bundles is covered in our reporting on why digital banking adoption is accelerating among SMEs.

Payments and FX: the fastest-growing B2B line

The fastest-growing revenue line at many US fintechs in 2024 and 2025 has been cross-border payments and FX. US-based B2B payments companies that serve international supply chains, marketplaces, and remittance corridors have seen volumes rise quickly as global commerce returned to pre-pandemic growth rates and as incumbent banks continued to price cross-border payments at rates that invited competition.

The US venture capital ecosystem has recognised this, and new-company formation in international B2B payments has been one of the more active corners of US fintech funding. The broader venture pattern is consistent with the analysis in our piece on the role of venture capital in fintech growth.

What this means for US fintechs

For US fintechs, the economic lesson of the last three years is that a single-revenue-line business is a fragile business. The firms that have reached operating profitability have diversified across at least two of the four categories above, and the most stable of them run meaningful revenue from three.

For founders, the implication is that the decision about revenue model is now a first-order product decision, not a late-stage monetization question. A fintech that cannot describe, at seed stage, which two or three of the four revenue lines it will run is a fintech that will struggle to raise a Series A in the current US market. That shift is part of the strategic rebalancing described in our piece on why fintech is becoming a strategic priority for financial institutions.

The longer arc

The economics of US fintech have converged on a recognisable shape. The days of revenue-free user growth are over; the days of single-line monetization are over. The fintechs that will define the next five years are the ones that have worked out which combination of interchange, interest, subscription, and payments revenue they can run together at an operating margin closer to software than to banking. For a wider view of how competitive dynamics are reshaping the sector, our analysis of how fintech is reshaping financial-services competition provides the frame.