A US neobank with over 10 million users spent most of 2023 explaining to investors that scale without net interest margin is not the same as a business. By late 2024, the same company was reporting its first full year of GAAP profitability, having restructured its revenue mix around interchange, lending, and a treasury book that actually earned. That turnaround, or, for some peers, the failure to produce one, is what platform economics means in the current US fintech cycle. The global fintech platform market was valued at roughly $135 billion in 2024 and is projected to exceed $220 billion by 2030, according to Fortune Business Insights.

What platform economics means in practice

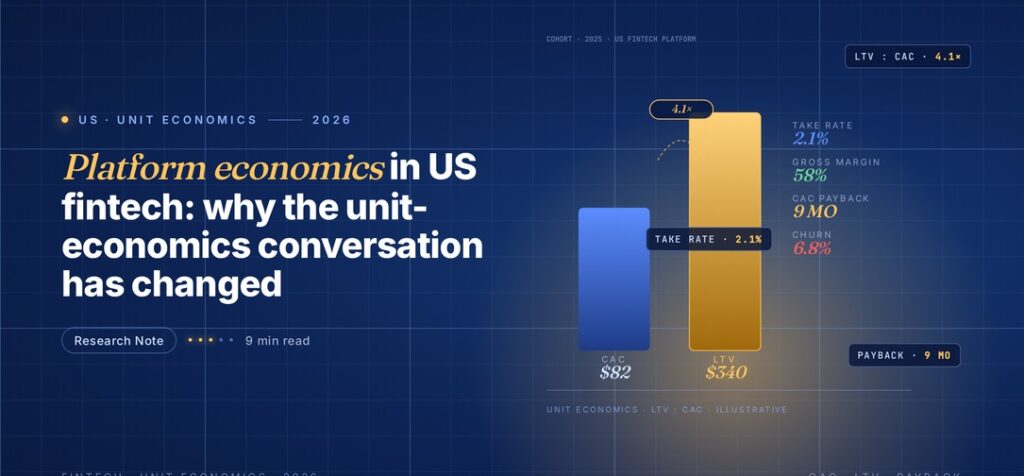

Platform economics in fintech refers to the unit-level math of a business that acquires users through a product, earns revenue across multiple transaction types, and has a cost structure dominated by fixed technology and compliance spend rather than variable cost-of-goods. In a bank, unit economics are mostly about net interest margin; in a fintech platform, they are a combination of interchange, interest, subscription fees, and spread on money-market balances, all layered on top of a customer-acquisition cost that has to amortise across the whole relationship.

The reason the US conversation has changed is that the two tailwinds that made fintech unit economics easy between 2019 and 2022, zero interest rates and cheap venture capital, both flipped at the same time. Fintechs now have to justify every customer against a measurable lifetime-value calculation rather than against a future promise.

The revenue-mix shift

The clearest evidence of the reset is how fintech revenue composition has changed. Five years ago, the typical US consumer fintech earned most of its revenue from interchange and subscription. Today, net interest income and treasury spread are often the largest line items, driven by higher rates and by business models that explicitly route customer balances into yield-bearing accounts.

| Revenue line | Typical 2020 share | Typical 2025 share | Main driver |

|---|---|---|---|

| Interchange | 50-70% | 20-35% | Volume still grows but share falls as other lines rise |

| Net interest / treasury spread | <10% | 30-50% | Higher rates; deposit sweeps; Treasury products |

| Subscription / premium tiers | 15-25% | 10-20% | Mature in consumer; growing in SMB |

| Payments / FX / other | 5-10% | 10-15% | Cross-border and B2B |

Source: company disclosures and Fortune Business Insights analysis; see the Fortune Business Insights fintech report.

The share ranges are indicative; individual companies vary widely. What is consistent across the US sector is the direction: away from interchange-dominant models and toward revenue mixes that look closer to a regulated bank.

Why customer-acquisition cost matters more than it used to

Customer acquisition cost has been the variable most affected by the new environment. Paid user growth through digital channels has become more expensive as platforms like Meta and Google consolidated ad inventory, and referral-driven growth has slowed because the most referral-friendly segments, early adopters, young professionals, are already inside the category.

The practical consequence is that US consumer fintechs are now distinguished by CAC payback periods measured in years rather than months. That puts a premium on products that monetise within the first six to twelve months of a relationship, which explains why deposit-sweep products, premium subscriptions, and credit products have all grown faster than pure checking. The shift echoes the broader digital-banking adoption pattern covered in our piece on why digital banking adoption is accelerating among SMEs.

What distinguishes the fintechs that have made the math work

The US fintechs that achieved operating profitability in 2024 share three characteristics. They own the primary account relationship, meaning customers route direct deposit or run substantial transactional balances through the platform rather than treating it as a secondary account. They have at least two meaningful revenue lines, so that a decline in one does not threaten the business. And they have brought compliance and risk operations in-house at a cost structure that scales sub-linearly with customers.

That last point is the most underappreciated. A BaaS-dependent fintech pays a sponsor bank per account and per transaction; a fintech with its own charter or banking partnerships engineered for scale does not. The economics diverge dramatically at the 1-million-customer mark. For more on how this dynamic sits inside the larger sector shift, see our analysis of how fintech is reshaping competition in financial services.

Where venture capital has moved

Venture capital has not left fintech, but it has moved up-market and down-market at the same time. Early-stage money is flowing again into specialised infrastructure plays, compliance, identity, payments rails, that serve the existing fintech stack. Late-stage capital is concentrated in companies with demonstrated unit economics and a plausible path to public markets. The middle has thinned: the growth-stage consumer fintech category that raised at double-digit billions between 2019 and 2021 has had almost no new entrants at that scale since.

That pattern is consistent with the broader venture-capital analysis in our reporting on the role of venture capital in fintech growth.

What this means for operators

For operators, the playbook has narrowed. The US market will no longer reward a consumer fintech that grows users without a clear monetisation path. Early hires in risk, compliance, and treasury are now as important as early product and marketing hires. Founders are building smaller teams with sharper unit-economics targets from the start, and growth rates expected in 2019 have been replaced by gross-margin expectations closer to those of a software company.

The longer arc

Platform economics in US fintech has completed a full cycle. The first wave was about growth; the middle period was about whether growth could be funded; the current phase is about which revenue models hold up against a bank-adjacent cost base. The next wave will be decided by which US fintechs can sustain a software-like margin profile while carrying regulated-finance obligations, a narrower doorway than the one most of the industry walked through during the last boom. For a broader view of how strategic priorities inside traditional institutions are shifting in response, our piece on why fintech is becoming a strategic priority for financial institutions tracks the parallel move.