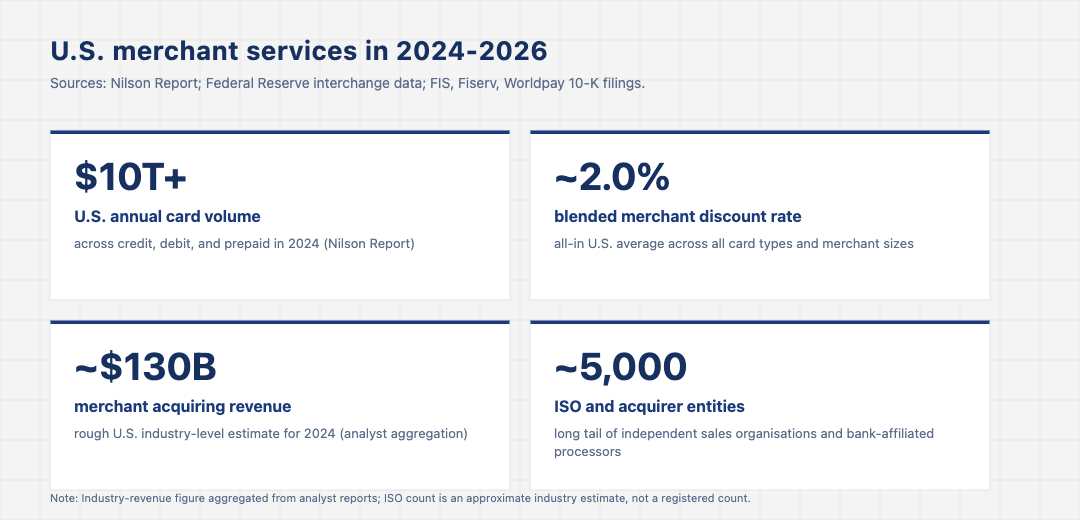

Walk into any independent restaurant in any U.S. city in May 2026, and the payment terminal on the counter is more often than not a Square reader, a Toast tablet, or a Clover device, not the bank-branded countertop terminal that would have been there fifteen years earlier. The transition is partly aesthetic and mostly economic. The U.S. merchant services category, which collectively processed more than $10 trillion in card volume across 2024 according to the Nilson Report, has been quietly remade across the past decade. The category that was once an opaque relationship between a small business and an independent sales organisation, with surprise fees and three-year contracts, is now a software-led product category where pricing is transparent and switching is easy. The old acquirer stack is finally cracking, and the implications for the roughly $130 billion of annual U.S. acquirer revenue are significant.

What U.S. merchant services actually covers

The phrase “merchant services” is a catch-all for the bundle of products a small or mid-sized merchant needs to accept card payments. At minimum it includes a payment terminal or online checkout, a gateway service that talks to the card networks, an acquiring bank that holds the merchant account and submits transactions for clearing, and the underlying contracts and pricing schedules that govern what the merchant pays. Around that core sit a constellation of adjacent products: chargeback management, gift cards, loyalty programmes, business banking accounts, working capital advances, payroll, and increasingly point-of-sale software that runs the rest of the merchant’s operation.

The traditional U.S. structure was that a small merchant got everything from an independent sales organisation, an ISO, that resold the services of a back-end processor like First Data, Global Payments, Worldpay, or FIS, with an acquiring bank further behind that. The ISO charged a markup on top of interchange and the processor’s fees, and the merchant rarely understood the full pricing because the underlying interchange schedules are themselves several hundred pages of bilateral pricing tiers. The structure made sense in 1995 when door-to-door sales got terminals deployed; it made progressively less sense as merchants got better information and more alternatives. By the late 2010s the structure had become a textbook information-asymmetry problem.

The economics that have driven the shift

The headline U.S. number is that the average all-in merchant discount rate, the total a merchant pays per dollar of card transaction volume, is roughly 2.0 percent across credit, debit, and prepaid combined, with substantial variation by merchant size and category. Of that 2.0 percent, interchange to the issuing bank is the bulk, typically 1.5 to 1.8 percent on a credit transaction. Card network fees are another 13 to 15 basis points. The acquiring fee, which is what the merchant services provider actually keeps, is the residual, somewhere between a few basis points for very large merchants on interchange-plus pricing and several percentage points for very small merchants on simple flat-rate plans.

The aggregate U.S. acquirer revenue pool is roughly $130 billion based on industry-analyst aggregation, with the top five acquirers including Stripe, Block, Adyen, Fiserv, and FIS taking the largest single shares. The remainder is distributed across roughly 5,000 ISOs, smaller bank-affiliated acquirers, and vertical-specific players. The pie has been growing at roughly card-volume growth rates, which is to say faster than GDP, and the rate compression on individual merchants has been more than offset by the underlying volume growth. Most of the value migration in the category has been within the pie, from legacy ISOs and processors toward software-led entrants, rather than the pie itself shrinking. The TechBullion piece on payments systems and infrastructure covers the broader rail context.

The Square model that broke the old stack

The most consequential change in U.S. merchant services in the last fifteen years was Square’s launch of a flat-rate, contractless, software-led merchant service in 2009. Square’s pricing was deliberately simple: a single percentage rate per transaction, no setup fee, no monthly fee, no commitment. The simplicity was the product. It made the cost of switching, and the cost of trying, essentially zero, which broke the door-to-door ISO sales model that the legacy acquirers depended on. By 2015 Block (then called Square) had millions of merchants. By 2024 the company reported approximately $228 billion in Square gross payment volume in its 2024 10-K, with total Block GPV of $240.8 billion. The legacy acquirers responded by building their own software-led offerings, by acquiring software-led entrants, or by losing share. Most of the share-loss has been at the small-merchant end, where the legacy stack was most exposed and where the software-led economics worked best.

The other half of the disruption came from PSPs like Stripe building merchant-services-equivalent products for online merchants. The collapse of the gateway-acquirer distinction discussed in the TechBullion piece on why banking infrastructure is becoming digital is largely about Stripe and similar online-first PSPs absorbing the acquirer role into the API. The result, by 2026, is that very few new U.S. merchants choose a traditional ISO model. The default for online is Stripe; the default for in-person is Square, Toast, or Clover; the default for enterprise is Adyen.

The vertical software bundling that is reshaping the category

The most economically interesting development in U.S. merchant services in 2024 and 2025 has been the rise of vertical-specific software-and-payments bundles. Toast in restaurants, Mindbody in wellness, ServiceTitan in home services, Procare in childcare, all sell merchant services as part of a software stack designed for a specific industry. The economics work because the software justifies a much higher per-merchant subscription fee than a generic POS would, and the payments revenue then sits on top with much less price sensitivity than a stand-alone payments product would face.

For Toast specifically, the payments-attached model has driven a meaningful share of company revenue and is the principal reason the company commands a software-style valuation rather than a hardware-style one. The pattern is replicating across vertical after vertical. The implication for the broader merchant services category is that horizontal generic acquiring is increasingly the commodity layer underneath, with the value moving to the vertical software wrapping it. The TechBullion piece on why banking innovation is accelerating worldwide covers the broader vertical-bundle pattern, which is increasingly the global story rather than a U.S.-specific one.

What founders and merchants should take from the shift

For merchants, the practical implication is that the contract is renegotiable. The 2026 merchant has more leverage than at any previous point in this category, with multiple credible alternatives and pricing transparency that did not exist a decade ago. For founders, the implication is the inverse: building a generic horizontal merchant services product is harder now than it has ever been. Building a vertical-specific software product with payments attached is easier than it has ever been. The funding environment has noticed this distinction, and most recent merchant-services-adjacent investment is in vertical software companies that monetise primarily through attached payments rather than in horizontal acquirers competing on rate.

U.S. merchant services in 2026 is not a quiet utility category. It is one of the more economically interesting parts of the broader fintech sector, with $10 trillion of underlying volume, $130 billion of revenue at stake, and an architectural shift from horizontal acquirer to vertical software that is still actively playing out. The old ISO-and-processor stack is not gone; it still serves a meaningful slice of the U.S. merchant base. But it is no longer the default, and the trajectory of the next several years is set. The interesting question for the rest of the decade is which verticals get bundled next, which legacy acquirers respond well enough to remain relevant on the other side, and how much of the existing $130 billion revenue pool migrates into the hands of the software platforms that were not even in this category five years ago.