A US treasurer trying to send a payroll batch from New York to Singapore in 2026 has more options than at any point in the dollar’s history. According to a BIS CPMI cross-border payments programme published earlier this year, total US-resident cross-border payment volume reached roughly 1.8 trillion dollars in 2025, growing at high single digits, while the average end-to-end settlement time for the fastest channel collapsed from days to seconds. The growth alone is not the news. The news is the changing share of who carries the volume, with stablecoin rails posting double-digit gains while traditional correspondent banking lost ground for the first time on record. The story is not just about technology adoption. It reflects a structural change in how US-resident corporates and consumers think about moving dollars internationally, with new players entering the rail mix every quarter and existing banks rebuilding their cross-border services around APIs rather than messages.

The pipes that move dollars across borders

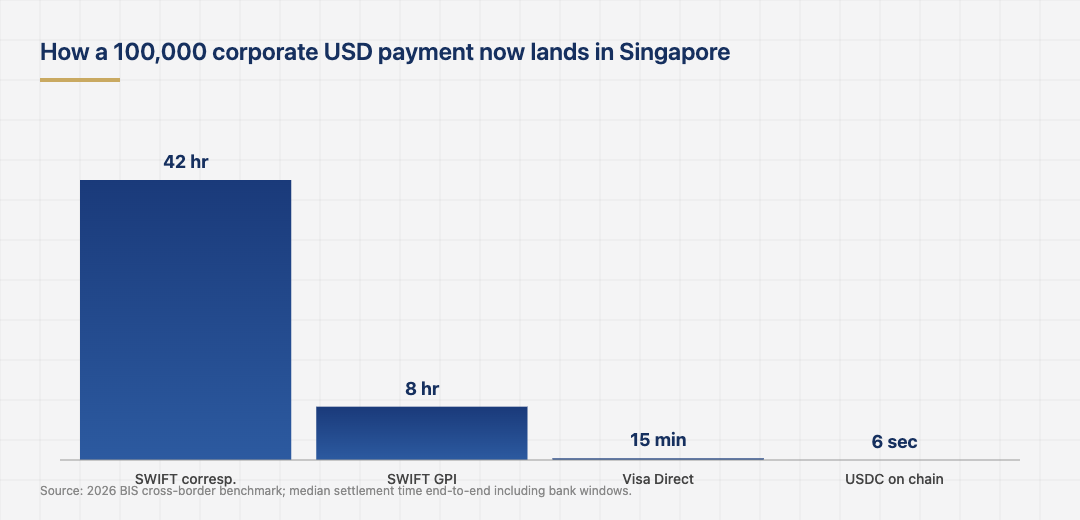

For most of the post-Bretton Woods era, US-originated cross-border payments meant SWIFT messages between correspondent banks, with three to five hops on a typical large-value transaction. The model worked, but it was slow and opaque. Fees were difficult to predict and settlement could take days, especially across multiple time zones. SWIFT itself responded with the SWIFT GPI service in 2017, which improved tracking and reduced settlement to hours for most major corridors. Card networks built parallel rails: Visa Direct and Mastercard Send now move funds across borders in under fifteen minutes for many country pairs. Specialised fintechs like Wise built API-first remittance flows that bypassed correspondent banking entirely. The most recent entrant is the stablecoin rail, where dollar-pegged tokens move on public blockchains and settle in seconds. The breakdown of where the 1.8 trillion now sits is no longer dominated by a single rail. The same dynamic is playing out in domestic settlement, where real-time payments adoption has shifted volume away from card and ACH systems for higher-value transfers.

Where the volume actually goes

Roughly 60 percent of US cross-border payment volume in 2025 still moved through traditional correspondent banking, but that share is down ten percentage points in three years. SWIFT GPI accounts for most of the bank channel, with corridor coverage now reaching most major economies. Card-network rails handled about 18 percent of volume, with Visa Direct alone clearing more than 200 billion dollars in 2025 across more than 190 countries, with average payout times under fifteen minutes. Money-services businesses, including Western Union and Wise, accounted for 12 percent of US-resident cross-border payment volume during 2025, with most of that share tied to consumer-to-consumer remittances rather than corporate flows. The remaining 10 percent moved over stablecoin rails, up from less than 2 percent in 2023, with the share concentrated in corridors where bank infrastructure has historically been thinnest. The dollar-volume figure understates the operational shift, because stablecoin transactions are typically smaller and higher in count, suggesting the rail is being used for use cases that previously required several days of correspondent processing. The composition of stablecoin flows is also revealing: roughly 70 percent is B2B according to issuer data, with the remaining share split between remittances and treasury operations inside multinational corporates.

The corridor mix matters as much as the rail mix. Latin American corridors are the most stablecoin-heavy, with USDC and USDT now accounting for the majority of US-to-LatAm B2B settlement in surveys conducted by remittance trade groups. Asian corridors are still dominated by SWIFT and Visa Direct because most beneficiary banks have not yet integrated stablecoin off-ramps. The same fragmentation surfaces in embedded finance work, where US fintechs are increasingly the rail of choice for non-bank software platforms moving money internationally.

Why correspondent banking is losing share

The shift has three drivers. The first is cost. Traditional correspondent banking is expensive on small-to-medium-sized payments, where the per-transaction fees can wipe out a meaningful percentage of the principal. Stablecoin rails charge a fraction of a percent on most chains. The second driver is speed. A treasurer paying overseas suppliers no longer wants a 24-hour window for a payment to arrive. Same-day or instant arrival removes working-capital friction and allows for cash management that was not possible before. The third driver is transparency. Stablecoin transactions are visible on chain, with confirmation that a counterparty received exact funds, end of story. Bank statements can take hours or days to update. Correspondent banks have not stood still. SWIFT GPI now offers status-tracking comparable to the on-chain rails, and most large US banks have invested in API connectivity that lets corporate treasurers initiate and monitor payments in close to real time, including direct integration with ERP systems used by Fortune 500 finance teams. The rail-level improvements have prevented faster share loss than would otherwise have occurred.

The compliance lift

The compliance picture across rails is uneven. Bank-led rails have decades-old AML and sanctions infrastructure baked in. Stablecoin rails are catching up, with most major issuers now operating screening at the issuer level and sanctions list integration at the wallet level. The federal stablecoin framework that passed in 2025 made these requirements explicit. Treasury OFAC has clarified that USDC and USDT issuers, as US-regulated entities, are responsible for blocking sanctioned wallet addresses, and Circle has publicly published quarterly transparency reports on this. The remaining gap is in correspondent stablecoin flows, where one bank uses stablecoins as a settlement layer between two SWIFT endpoints. The compliance attribution there is still being worked out, and at least one major US bank has paused its stablecoin pilot in 2025 over precisely this question. Wider regulatory framework reporting tracks how Treasury and the federal banking agencies are now treating these flows, with new joint guidance expected in the second half of 2026.

What 2026 will likely change

Three things are likely to shift through the rest of the year. First, more US Tier 1 banks will offer client-facing stablecoin payment products as a complement to SWIFT, rather than running internal pilots. Bank of America, JPMorgan, and Citi have each disclosed roadmaps that point this direction, and BNY Mellon is building custody products around the major stablecoins. Several regional banks have also begun to offer FX hedging products tied directly to stablecoin payment flows, which removes one of the main objections that corporate treasurers had against using on-chain rails for international settlement. The product set is still incomplete in many corridors, and several US banks expect 2026 to be the year their stablecoin offering moves from a small pilot to a mainstream commercial-banking line. Second, the pricing pressure on traditional correspondent banking will intensify, particularly in corridors where stablecoin alternatives are now mainstream. Banks will respond with bundled services or tighter integration with their treasury platforms. Third, regulators will publish a more complete framework for cross-border stablecoin flows, addressing the questions of which entity owes the AML obligation when a payment hops between rails. None of these alone will displace correspondent banking. Together, they tilt the volume share toward instant rails fast enough that by 2028, the dominant channel for most corridors is unlikely to be the one that has run for the last forty years. Corporate treasurers and bank product managers are already planning around that assumption, even when they cannot yet say in which year it lands.

A treasurer who needed to send funds across borders in 2015 had two practical options and a clear understanding of which would work. In 2026 the same treasurer has at least four good options and a harder choice. The infrastructure underneath cross-border payments in the US is no longer a settled question. It is a competitive market, with stablecoins, card networks, and traditional banks all reaching for the same volume, and the corridor-by-corridor story is now what corporate treasurers spend most of their time tracking when they design 2026 cash management plans.