Most U.S. consumers have not knowingly used a blockchain payment, but a fast-growing share of U.S. businesses have. The boundary between “crypto payment” and “ordinary payment” has been blurring for two years, and by January 2026 it has effectively dissolved in three corridors: cross-border B2B transfers, U.S. dollar settlement for global digital businesses, and on-chain payroll for crypto-native firms. According to Chainalysis, U.S.-originated stablecoin payment volume reached $4.1 trillion in calendar 2025, up from $1.7 trillion in 2023. The category has stopped being an experiment, and the use cases for blockchain for payments America are now visibly shaping treasury operations.

The shape of the volume

The composition of that $4.1 trillion is the most useful data point. Roughly $2.7 trillion was settled in USDC, $1.1 trillion in Tether, and the balance in PYUSD, RLUSD, and a small set of bank-issued tokenised deposits. Cross-border B2B transactions were the largest use case at about $1.4 trillion, followed by FX-corridor settlement at $980 billion and on-chain payroll at $130 billion. The remainder included remittances, marketplace settlement, and a long tail of niche flows. The split shows that blockchain payments grew where the underlying friction was greatest: cross-border, multi-currency, and time-sensitive contexts where existing rails impose either delay or cost.

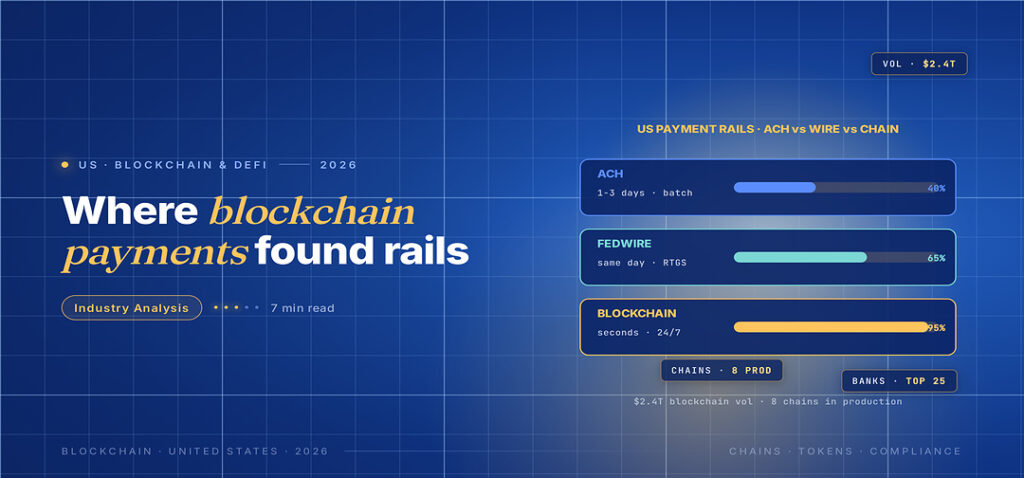

A useful comparison is what blockchain payments are not yet doing. Domestic U.S. consumer payments remain almost entirely on traditional rails (Visa, Mastercard, ACH, FedNow). The reason is straightforward: the existing rails are good enough at low cost that there is no commercial space for a blockchain alternative. The cross-border gap is different. Wire transfers cost $25 to $40 and take one to two business days. A stablecoin transfer costs cents and clears in minutes. The economics are not close, and U.S. corporate treasuries have noticed.

Who is moving the volume

The most active U.S. corporate users of blockchain payments in 2025 were not crypto firms. They were U.S. multinationals running global operations: SpaceX, Uber, Lyft, and Boeing all integrated stablecoin settlement into specific treasury workflows during 2024 and 2025, mostly for paying contractors, suppliers, and minority-market sales channels. Visa’s stablecoin settlement programme, which lets card issuers settle interchange in USDC, ran roughly $19 billion in 2025. Mastercard’s competing programme passed $14 billion. Stripe acquired Bridge in late 2024 and quietly turned stablecoin acceptance into a default option for international merchants by mid-2025; the company reported processing $42 billion in stablecoin settlement in the second half of 2025 alone.

U.S. banks have moved more cautiously, but several have moved. JPMorgan operates JPM Coin, which processes intra-firm and bilateral transactions averaging $2.6 billion daily. Citi runs Token Services for cross-border treasury management, with about $5 billion in 2025 throughput. Bank of New York Mellon and State Street operate institutional custody for tokenised assets and use the same infrastructure for settlement of those assets, though they do not yet operate consumer-facing payment products on chain. The pattern is the same one visible in every other tokenisation category: institutions are using the technology, but they are not branding it for the consumer.

The corridor data is granular enough to be useful. The U.S.-Mexico corridor saw $187 billion in stablecoin volume in 2025, mostly through MoneyGram’s USDC integration and a handful of fintech remittance providers (Felix Pago, Bitso, Strike). The U.S.-Philippines corridor saw $94 billion, with Bittwa, MoonPay, and a small group of regional payment processors carrying most of it. The U.S.-Vietnam corridor saw $61 billion, almost all through Stripe’s Bridge product. None of these corridors had any meaningful blockchain volume in 2022.

The price elasticity of the demand is striking. Cross-border B2B fees that traditional rails charge at 2.5 to 3.5 percent compress to 0.4 to 0.7 percent on stablecoin rails. Even after accounting for on-ramp and off-ramp fees, the all-in cost is roughly half of the legacy alternative. For a mid-sized U.S. exporter doing $80 million annually in cross-border B2B, the savings are visible in the operating margin line.

The regulatory unlock

Two pieces of U.S. regulation finalised in 2025 made the current scale possible. The GENIUS Act required dollar-pegged stablecoins to back every issued token with cash or short-dated Treasuries, audited monthly, and gave both bank and non-bank issuers a defined path to operate at federal scale. The CLARITY Act drew a line between decentralised infrastructure and intermediated trading platforms, removing most of the legal ambiguity that had paralysed corporate treasury teams in 2022 and 2023. The combination meant that a CFO who wanted to use stablecoin settlement could get a clean legal opinion in days instead of months.

What did not get settled is whether stablecoin issuers should be subject to bank-level capital and liquidity requirements. The OCC and the Federal Reserve are reportedly drafting guidance, and a working consensus expected by mid-2026 is that issuers above a certain transaction volume threshold will be supervised under a federal charter. That, if it lands, would push smaller issuers either to merge or to operate under state-level money transmitter rules.

The other open question is the cross-border treatment. A USDC payment from a U.S. firm to a Vietnamese contractor still triggers ambiguous tax and reporting obligations on both sides. The Treasury Department issued guidance in February 2026 that began to clarify these obligations but stopped short of resolving them. The expected next step is a joint OECD framework that will land sometime in 2026 or early 2027.

What 2026 will probably reveal

Two questions are likely to dominate the year. First, whether blockchain payments cross from corporate treasury into consumer-facing products at meaningful volume. The trigger would be a major U.S. neobank (Chime, Cash App, or Robinhood) launching native stablecoin transfers as a default option. Several are reportedly in development; none has launched. Second, whether the FedNow network, which processed roughly $853 billion in total transaction value across calendar 2025, averaging just over $2 billion in daily volume by year-end, integrates a stablecoin settlement option for cross-border use cases. The Federal Reserve has not announced such a plan, but the operational rationale for one is strong, and the OCC’s Acting Comptroller has publicly mentioned it twice in 2025.

A third, smaller question is whether at least one large U.S. retailer integrates direct stablecoin acceptance at the point of sale. Whole Foods, Starbucks, and Chipotle are the names most often mentioned. The economics are debatable: U.S. retail margins are too thin to swallow card interchange fees, and a stablecoin acceptance flow could shave 1.5 to 2 percentage points off processing costs. The first major retail launch will set the pricing baseline for the rest of the industry.

The downstream effect on regional U.S. banks is worth flagging. The fee income that mid-sized banks earn on outbound wire transfers has dropped roughly 12 percent year-on-year, according to the FDIC’s quarterly call reports compiled in early 2026. That decline is small in absolute terms but represents the first sustained year-on-year drop in two decades, and it is concentrated in the segments most exposed to cross-border SME activity. Regional banks have responded by either partnering with a stablecoin provider (the more common path) or building their own deposit-token product (the more capital-intensive path).

What this means for blockchain for payments America

The U.S. position in blockchain payments is, ironically, less consumer-led than the position of several emerging markets. In Brazil, Pix dominates. In India, UPI dominates. The U.S. consumer payments market is well served by existing rails, and there is no operational space for a blockchain alternative at the consumer level. The U.S. position is corporate and institutional: stablecoins as a settlement currency, tokenised deposits as a wholesale rail, and on-chain treasury operations as a working line of business.

That position is more durable than a consumer-facing one. It is grounded in operational economics rather than user adoption psychology. A CFO does not need to be persuaded to use a faster, cheaper rail; the spreadsheet will do the persuading. By the end of 2026, the question for most U.S. multinationals will not be whether to use blockchain settlement; it will be how much of their treasury workflow to put on chain. That is a different conversation than the one happening eighteen months ago, and it is the one the next twelve months will define.