Three years ago the question about U.S. stablecoins was whether they would survive at all. Two large failures (TerraUSD and a brief de-pegging of USDC during the SVB crisis in 2023) had concentrated regulatory attention on the category, and at one point a federal ban looked plausible. The position by January 2026 is the opposite: stablecoin supply held by U.S.-accessible issuers has grown to roughly $213 billion, up from $128 billion at the start of 2024, according to CoinGecko aggregated reserves. The structure of the market has consolidated around the reserve model that the GENIUS Act ratified, and the conversation about stablecoin mechanisms in America has shifted from “if” to “how much further”.

The mechanism that won

Three issuance models competed in the early 2020s. The first was full-reserve fiat backing, where every issued token is backed one-for-one by cash and short-dated U.S. Treasuries held in audited reserves. USDC and PayPal’s PYUSD operated this way from inception. Tether moved most of its reserve composition to comply with this model during 2024 and 2025. The second was crypto-collateralised, where reserves consist of other crypto assets held in over-collateralised positions. DAI was the most prominent example. The third was algorithmic, where supply is balanced by a paired token under arbitrage incentives. TerraUSD was the most prominent example. By 2025 only the first model held meaningful market share. The second remained niche. The third, after Terra’s failure, effectively did not exist in the U.S.-accessible market.

The GENIUS Act, signed on July 18, 2025, formalised this convergence. It required dollar-pegged stablecoins offered to U.S. persons to be backed by cash and short-dated Treasuries held in audited reserves with monthly attestations, and it explicitly prohibited algorithmic stablecoins from operating under the federal framework. Crypto-collateralised stablecoins were given a partial pass under specific conditions, but the segment has not grown materially under the new rules. The Act also gave both bank and non-bank issuers a path to operate at federal scale, eliminating the patchwork of state-level money transmitter requirements that had previously fragmented the market.

Who actually issues U.S. stablecoin supply

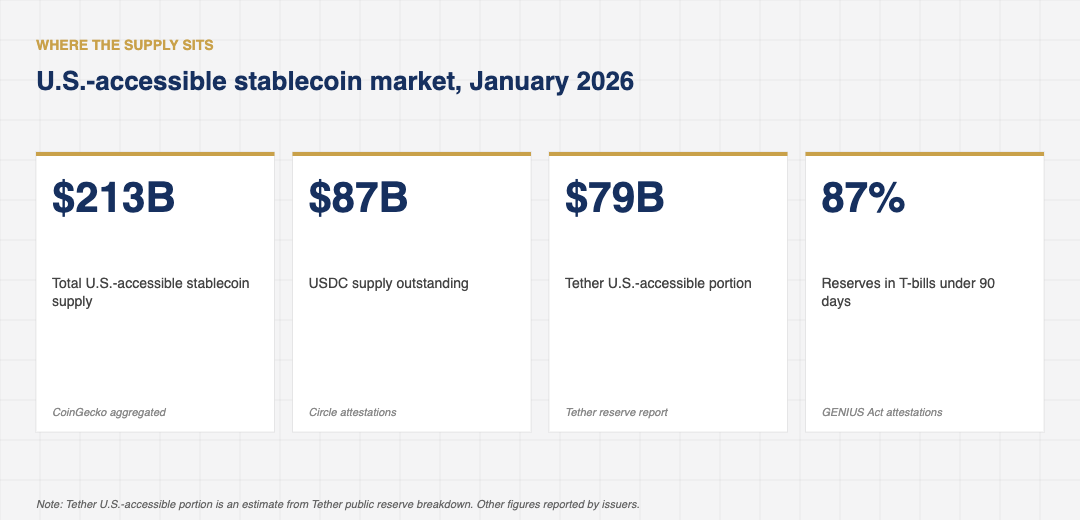

The composition of the $213 billion is concentrated. USDC accounts for $87 billion (Circle), Tether accounts for $79 billion (the U.S.-accessible portion), PYUSD accounts for $14 billion (PayPal), RLUSD accounts for $8 billion (Ripple), and a long tail of smaller issuers (FDUSD, USDH, GHO, plus several bank-issued tokenised deposits) makes up the remaining $25 billion. The top two issuers together hold 78 percent of the U.S.-accessible supply. The next three combined hold about 10 percent. The rest is split across roughly twenty smaller products.

The bank-issued tokenised deposit category is the most interesting growth area. JPMorgan’s JPM Coin, while technically a tokenised commercial bank deposit rather than a stablecoin in the strict sense, has crossed $14 billion in cumulative supply by January 2026. Citi’s similar product is at about $4 billion. Goldman Sachs and Bank of New York Mellon both operate institutional tokenised deposit products at smaller scale. The OCC’s December 2025 guidance, confirming that nationally chartered banks may use distributed ledger infrastructure for permitted banking activities without a separate filing, accelerated this category materially.

What the reserves actually hold

The aggregate reserves backing U.S.-accessible stablecoins held by issuers complying with the GENIUS Act are now disclosed in monthly attestations. The composition is conservative: roughly 87 percent of total reserves sits in U.S. Treasury bills with maturities under 90 days, 9 percent sits in cash held at federally insured banks, and 4 percent sits in repurchase agreements collateralised by Treasuries. The Treasury bill share has grown over time, partly because the yield differential matters at this scale and partly because Treasury bills satisfy the GENIUS Act reserve composition rules with the most operational simplicity.

The aggregate effect on the U.S. Treasury market is now a measurable line item. Stablecoin reserves represent roughly $186 billion of the $5.5 trillion T-bill market by January 2026, about 3.4 percent. The Treasury Department has flagged this concentration in its quarterly refunding announcements, partly as a market-stability disclosure and partly as a recognition that this is now a non-trivial buyer category in short-dated paper.

What the GENIUS Act left open

Several questions remain unsettled. The first is whether stablecoin issuers should be subject to bank-level capital and liquidity requirements when their float crosses certain thresholds. The OCC and the Federal Reserve are reportedly drafting joint guidance, with a working consensus that issuers above $50 billion in float will be supervised under a federal charter with capital ratios closer to a money market fund than a commercial bank.

The second is the tax and reporting treatment of stablecoin transactions for ordinary users. The IRS issued guidance in February 2026 that began to clarify the obligations but stopped short of resolving them. The expected next step, according to two of the law firms whose research we reviewed, is a joint OECD framework that will land sometime in 2026 or early 2027. Until then, accounting practice across the U.S. industry varies more than it should.

The third, more technical question is whether yield-bearing stablecoins, which pay holders a portion of the reserve interest, should be classified as money market fund shares or as bank deposits. The SEC has not signalled which it will treat them as, and the answer matters for fund disclosure, custody, and investor protection rules. A few smaller issuers have launched yield-bearing variants in anticipation of the answer; the major issuers have stayed out of that segment until the SEC decides.

The retail user experience has matured alongside the regulatory framework. Two years ago, a U.S. consumer who held USDC had to navigate a clumsy on-ramp process at a centralised exchange and worry about whether their stablecoin would still hold its peg next month. By the start of 2026, the most common entry point is a neobank app (Cash App, Robinhood, Venmo) that offers stablecoin balances as a savings option, often paying a fraction of the underlying reserve interest. Cash App’s stablecoin product, launched in mid-2025, reached 4.6 million U.S. users by January 2026. Robinhood Wallet’s similar product is at 3.1 million. The category has crossed the threshold where ordinary users think about a stablecoin balance the way a previous generation thought about a money market account.

The practical implication is that the U.S. stablecoin market is now growing through ordinary consumer acquisition channels rather than crypto-trading flows. That changes the elasticity of the demand. The growth from here is tied to neobank distribution, Treasury bill yield, and the cost of legacy savings-product alternatives, rather than to crypto market sentiment.

What 2026 will probably reveal about stablecoin mechanisms in America

Three questions will shape the year. First, whether the OCC and Federal Reserve guidance on capital and liquidity requirements lands, and at what threshold. The most likely outcome is a tiered framework that triggers at $50 billion in float, with progressively stricter requirements above that. Second, whether at least one major U.S. bank issues a publicly distributed deposit token aimed at consumers as well as institutions. Bank of America is the name most often mentioned, with a planned launch in the second half of 2026. Third, whether the SEC clarifies the treatment of yield-bearing stablecoins. A yes-classification as money market fund shares would push the segment toward registered investment products. A no-classification as bank-deposit equivalents would push it the other way.

What will probably not happen is consolidation among the top two issuers. USDC and Tether occupy distinct geographies and institutional positions, and neither has commercial pressure to merge or be acquired. The smaller issuers are more likely to consolidate or exit, with one or two large bank-issued products absorbing demand from the smaller specialty issuers over the course of the year.

By the end of 2026 the U.S. stablecoin market will probably look like the U.S. money-market fund industry: concentrated, regulated, dull, and large. That dullness is a feature. It is the condition under which a financial product moves from speculative novelty into ordinary infrastructure, and it is the condition the U.S. stablecoin industry has been working toward for the past three years.