China is cranking out T1100 carbon fiber at industrial scale, a material with roughly 7 GPa tensile strength that has long lived on the aerospace top shelf. That move from lab batches to mass output threatens to rattle a market long dominated by Japan and the United States, with Toray as the benchmark. Lighter, stronger composites could ripple through fighter airframes, launch vehicles, offshore wind blades, and EV chassis, trading metal for serious energy savings. It also fortifies Beijing’s supply chain amid Western export curbs and may push global prices lower as capacity builds. The stakes span defense credibility to consumer tech, measured not just in geopolitics but in gigapascals.

Breaking new ground in carbon fiber production

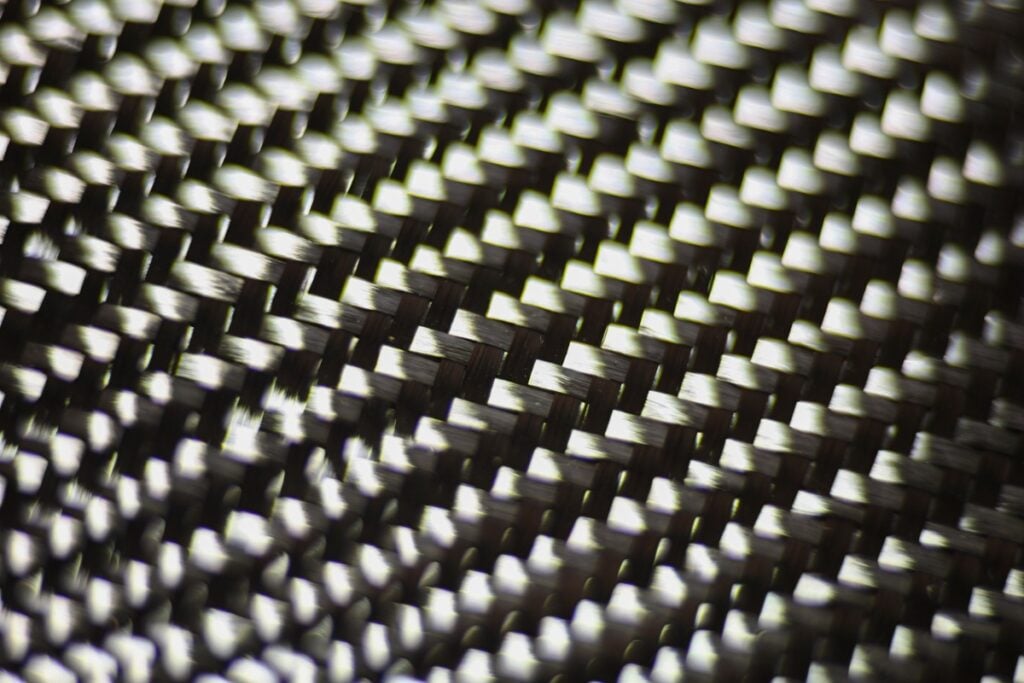

Material science rarely grabs headlines, yet it often refactors power dynamics across industries. China says it has moved the ultra-strong carbon fiber needle with mass production of T1100, a grade rated at a tensile strength of 7 gigapascals. If production quality and yield hold, that puts Beijing in a stronger position across defense, aerospace, energy, and advanced transport, where lighter structures translate into real performance and cost advantages.

Rivaling industry heavyweights

For decades, the highest tiers of carbon fiber were the domain of Japan and the United States, with Toray setting many of the benchmarks for what flies and what orbits. China’s push signals a shift from lab-grade breakthroughs to industrial throughput. Aviation-grade fibers often top out near 5 gigapascals, which helps explain why a credible T1100-class capacity could unsettle entrenched supply relationships.

Boosting energy efficiency with advanced materials

Weight is the tax on every journey. In aerospace, fewer pounds mean longer range or bigger payloads, whether you are talking commercial jets or launch vehicles. The same logic now drives electric vehicles, where shaving mass improves range without upsizing packs. Offshore wind is another lever: longer, lighter blades made with high-spec fibers endure fatigue, raise capacity factors, and cut maintenance over time.

Strategic independence and global competition

Beijing’s material push sits squarely within a broader effort to secure supply chains amid export controls and licensing by U.S. regulators. Strategic autonomy is not just policy language, it affects prices and availability for downstream buyers. If Chinese producers sustain volume and quality, expect tougher price competition and fresh scrutiny from the U.S. Department of Commerce on how these products touch American aerospace and defense programs.

Expanding possibilities beyond defense

The immediate applications point to missiles, aircraft, and spacecraft, but the spillover could be wider. Automakers hunting weight savings, rail and bridge projects seeking durability, and energy developers targeting higher uptime may all chase T1100-class properties. The open question for U.S. buyers is not interest, it is access: who can source, at what spec, and under what rules, as materials policy and markets collide again.

Source: https://www.vizonfiber.com/es/global-carbon-fiber-industry-witnesses-historic-breakthroughs-in-q1-q2-2026-from-t1200-mass-production-to-aerospace-supply-chain-expansion