Florida levies no personal income tax, so you can pick any 529 plan in the country without forfeiting a deduction (South Florida Reporter). In 2024 the SECURE 2.0 rule sweetened the deal: according to Life Money USA, unused 529 dollars can roll into the beneficiary’s Roth IRA—tax- and penalty-free—up to $35,000 after 15 years.

Fees are now the real villain. Morningstar’s latest medal table shows only a few Gold-rated, low-cost plans—Illinois, Utah, Massachusetts, Pennsylvania, and Alaska—keep expense drag near one-tenth of a percent.

In the pages ahead we rank the seven best options for Florida savers, so you can grow more tuition dollars and spend more time cheering “Go Gators.”

Ready? Let’s put your no-tax freedom to work.

How we ranked the plans

Before we crown any winners, you deserve to see the playbook.

Transparency keeps this guide honest and makes your choice easier.

We judged every direct-sold 529 plan through a five-pillar lens that mirrors what smart fiduciary advisors track. Each pillar carries a clear weight, so you can see exactly why one plan rises and another stumbles.

Cost sits first in the lineup at 30 percent.

Fees never sleep; they nibble at returns each year. A tenth of a percent may sound small, yet on a $50,000 balance it drains roughly $50 a year, money your future graduate will never see. Plans charging under about 0.15 percent scored highest.

Bright Start 529’s own fee table lists its index Enrollment Year Portfolios at just 0.10 percent a year, and the plan’s average cost across all portfolios runs 0.24 percent—about half the 0.49 percent national 529 average.

That concrete price tag shows exactly how staying below the 0.15 percent cut-off preserves more tuition dollars for your future graduate.

Investment quality claims 25 percent.

We looked for diversified, age-based portfolios, sensible glide paths, and proven managers such as Vanguard, Dimensional, or Fidelity’s index suite. Morningstar’s latest medal table provided an outside gut check: only Gold or upper-Silver plans made our short list.

Flexibility and features earn 15 percent.

Can you tailor a portfolio or stick with autopilot? Does the plan accept payroll deposits, enable easy gifting, and support the new Roth rollover rules that let leftover dollars grow for retirement? Plans that answered “yes” climbed quickly.

Customer experience also claims 15 percent.

We opened demo accounts, clicked through enrollment flows, and timed how fast contributions hit the market. Same-day investing, clean dashboards, and responsive support teams helped separate frictionless leaders from “it’s fine” laggards.

Finally, Florida-specific utility rounds out the last 15 percent.

Strong creditor protection, nationwide portability if you move, and zero residency strings were non-negotiable. Remember, you have no state tax carrot to keep you local, so the plan must travel well wherever life takes you.

Add up the scores and you get our ranked seven.

Simple math, clear criteria, and a straight path to the best place for your hard-earned tuition dollars.

1 Bright Start (Illinois)

Bright Start wins because the Illinois Bright Start 529 college savings plan couples a sub-0.10 percent program charge with a Morningstar Gold rating earned over more than 25 years of helping families nationwide save $12.5 billion for college. The program charge hovers near 0.10 percent, and the age-based index tracks land around 0.13 percent all-in. On a $25,000 balance you pay about $30 a year, then watch the savings compound over 18 years instead of leaking away.

Morningstar keeps awarding Bright Start its top medal thanks to tight state oversight and glide paths that stay on course as assets grow. The team trims costs whenever scale allows, and that vigilance shows up in performance tables where Bright Start often outpaces pricier peers.

Flexibility is another edge. Parents can choose an all-index track and forget it or switch to a blended series that adds active managers such as Dodge & Cox and T. Rowe Price at a modest cost. A capital-preservation option sits ready for students who start college soon. Same-day investing, shareable gifting links, and a clean dashboard make the experience smooth on both desktop and phone.

For Florida savers, every basis point matters because there is no home-state tax perk. Bright Start squeezes fees, travels well if you move, supports the new 529-to-Roth rollover, and invests cash the moment it lands. That is why Illinois tops our list for Sunshine State families.

2 my529 (Utah)

Bright Start feels like a reliable sedan, while Utah’s my529 plays the sports car. The plan keeps costs low and lets you fine-tune every setting under the hood.

Fees stay razor-thin, sitting just above Illinois yet still well below the national average. More of every dollar you deposit continues to compound instead of covering overhead.

Control is the real feature. Choose a prebuilt age-based track and let it glide, or build your own mix from more than twenty funds, including Dimensional’s factor-tilted options. Set a 90-10 stock-bond split until sophomore year, then ease to 40-60 by senior spring with a few clicks.

The user experience matches the engineering. Contributions invest the same day, gifting links reach grandparents in seconds, and the dashboard shows each holding in plain language. my529 also rolled out the 529-to-Roth feature early, so shifting leftover funds into your child’s retirement account is straightforward.

Pick Utah if you like to tinker, crave flexibility, or simply want a low-cost plan that adapts to your investment view. Power users feel right at home, and set-and-forget investors can still coast with confidence.

3 Vanguard 529 (Nevada)

Sometimes you just want the classics. Vanguard’s Nevada plan sticks to the proven index-fund recipe: simple, low cost, and reliable.

All-in expenses hover around 0.12 percent on the age-based track, placing this plan among the nation’s cheapest. Every basis point saved buys future textbooks.

The lineup offers three enrollment portfolios: Aggressive, Moderate, and Conservative. Each glides from stock-heavy in the early years to bond-heavy as college nears. Prefer to build your own mix? Static choices such as 100 percent Equity, 60/40 Balanced, or Short-Term Bond stand ready. No active bets or exotic assets, just broad-market exposure that tracks its benchmarks.

Simplicity extends to the experience. If you already use Vanguard for a brokerage or IRA, the 529 appears in the same dashboard with one login. Contributions invest the same day, and a share-a-link tool lets relatives gift money without routing numbers.

For Florida savers who want a set-and-forget plan from a brand they already trust, Nevada’s Vanguard 529 is the easy button: low fees, market-matching returns, and almost no learning curve.

4 Pennsylvania 529 investment plan

Pennsylvania sliced its fees in 2023 and never looked back. The index age-based portfolios now cost roughly 0.20 to 0.25 percent, a drop that lifted the plan into Morningstar’s Gold tier.

Think of it as Vanguard with a twist. Portfolios rely on Vanguard index funds—Total Stock, Total International, and Total Bond—but add an optional Socially Responsible Equity slice for savers who want ESG exposure without hunting for niche products.

Governance also impresses. The state treasury, not a third-party contractor, negotiates fees and oversees strategy. When assets grow, management shares the savings with investors instead of pocketing them.

User experience checks all the boxes: same-day investing, zero maintenance fees, and a polished site run by Ascensus. You can open an account over lunch, send a gifting link before dinner, and switch funds twice a year without paperwork headaches.

For Floridians, Pennsylvania is the “indexed but interesting” pick—diversified, ESG-friendly, and still cheap enough to keep more dollars compounding for tuition.

5 U.Fund College Investing Plan (Massachusetts)

Fidelity runs the show in Massachusetts and it shows. U.Fund delivers institutional-grade Fidelity index funds inside a clean portal and prices the index track near 0.15 percent, keeping it firmly in the low-fee club.

Choice is the hook. Stay fully passive with the Index Age-Based series, lean into Fidelity’s active managers with the Active track, or split the difference in Blend. Each path glides from stock-heavy in diapers to bond-heavy by senior year, so you avoid rebalancing stress.

Parents already using Fidelity for a 401(k) will feel at home. The 529 appears in the same dashboard, shares the same two-factor login, and funds from the same linked bank within seconds. Automation is smooth, and support routes through Fidelity’s nationwide call center, helpful even on a Saturday morning.

An underrated perk is the inflation-protected bond portfolio. If you worry about tuition rising faster than CPI, parking late-stage dollars in the TIPS sleeve adds a hedge most plans skip.

Bottom line: U.Fund suits families who love Fidelity’s interface or want the option to add active management without giving up the fee edge Florida’s free-agent status provides.

6 Invest529 (Virginia)

Virginia often lands on “best 529” lists for one reason: it trims fees to the bone while adding features most rivals skip. Index portfolios cost about 0.10 percent, matching Utah’s price and beating many robo-advisors that claim to be cheap.

The plan’s multi-manager design blends Vanguard index funds with specialty sleeves from Dimensional and Aberdeen, giving you broad diversification without gimmicks. For students close to move-in day, the Stable Value portfolio stands out. It recently paid about 3 percent while protecting principal, a rare safety net when you want to lock in gains yet earn more than a money market.

Account setup feels smooth. Virginia’s in-house tech team built a clean interface; contributions invest the same day, and you can open with no minimum—ideal if you want to start with $25 from a baby-shower check. Gifting takes seconds through a shareable link, and there are no annual maintenance or paper-statement fees hiding in the fine print.

For Florida families, Invest529 is the budget pick with a twist: ultra-low costs now and a safe harbor later. If your plan calls for dialing down risk as college nears without giving up yield, Virginia deserves a hard look.

7 New York 529 direct plan

New York shows how size breeds efficiency. With more than $40 billion under management, the program’s scale drives index-track fees to roughly 0.11 percent, only a touch above Utah and Virginia. Because the plan owns institutional share classes in bulk, investors feel each Vanguard expense cut almost at once.

The menu stays pure index. Three glide paths—Conservative, Moderate, and Growth—cover the risk spectrum, while fourteen single-fund options let hands-on savers build a custom mix. Need a 60 / 30 / 10 split among U.S. equity, international equity, and bonds? Pick three funds and you are set. A socially responsible balanced option is available for value-aligned investors.

Federal law lets you change investments twice a year, which suits most buy-and-hold families. Online account opening takes about ten minutes, contributions invest the same day, and a ugift code turns birthdays and holidays into easy 529 deposits.

Why should a Floridian care about a New York tax break they cannot claim? Because relatives in New York can. If Grandma on Long Island wants her own deduction, funding your child’s NY 529 keeps everyone happy and all dollars in one place. Even without that angle, razor-thin costs and a high account cap above $520,000 make this plan attractive for aggressive savers.

In short, New York offers Vanguard index funds at wholesale pricing, a simple gifting portal, and the comfort of a program large enough to keep fees drifting lower over time.

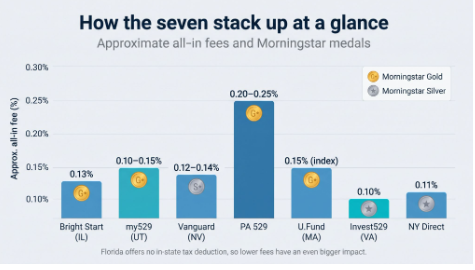

How the seven stack up at a glance

We toured each plan’s highlights earlier. Now the numbers sit side by side so you can compare fees, ratings, and standout perks in seconds.

| Plan | Approx. all-in fee | Morningstar medal | Unique edge | Best fit |

| Bright Start (IL) | 0.13 percent | Gold | Index and active tracks; same-day investing | Cost hawks who still want choice |

| my529 (UT) | 0.10–0.15 percent | Gold | Build-your-own portfolios with DFA funds | DIY tinkerers, factor fans |

| Vanguard 529 (NV) | 0.12–0.14 percent | Silver | Pure Vanguard index lineup in one login | Set-and-forget index investors |

| PA 529 Investment | 0.20–0.25 percent | Gold | ESG equity option within an all-index menu | Value-driven savers seeking ESG |

| U.Fund (MA) | 0.15 percent (index) | Gold | Choose Index, Active, or Blend tracks | Fidelity loyalists, active-curious |

| Invest529 (VA) | 0.10 percent | Silver | Stable Value portfolio with guaranteed rate | Fee minimalists planning a risk off-ramp |

| NY Direct Plan | 0.11 percent | Silver | Huge scale keeps fees sliding lower | Big savers, relatives in NY gifting |

Remember, Florida offers no in-state tax incentive, so the fee column matters most over 18 years of compounding. If two plans tie on cost, let user experience or a special feature—like Virginia’s Stable Value or Pennsylvania’s ESG sleeve—break the tie for you.

Florida 529 FAQs: quick answers before you hit “open account”

Can I pick Utah’s plan and still pay the University of Florida?

Yes. A 529 from any state pays qualified expenses at nearly every accredited U.S. college—and many abroad.

What if we move to Georgia next year?

Your plan moves with you. If the new state offers a deduction on its own 529, you can open a second account there or roll assets over once every 12 months without tax or penalties.

Will a 529 hurt my child’s financial-aid package?

When a parent owns the account, FAFSA counts up to 5.64 percent of the balance, a mild hit compared with assets held in the student’s name. New FAFSA rules also exclude grandparent-owned 529 withdrawals from student income.

What if my child wins a full scholarship?

You have options:

- Use the money for grad school, trade school, or up to $10,000 of student loans.

- Change the beneficiary to a sibling—or even yourself.

- Withdraw up to the scholarship amount penalty-free (earnings are taxable).

- Keep the account for future grandkids; it never expires.

- Starting in 2024, roll up to $35,000 into your child’s Roth IRA once the 529 is 15 years old and annual Roth limits allow

How much can we contribute?

There is no federal cap, only gift-tax rules. In 2026 a couple can front-load $190,000 using the five-year election without touching their lifetime exemption. Each plan sets a lifetime ceiling—Florida’s is $500,000, New York’s is $520,000—so most families run out of tuition bills before hitting the limit.

Do I need both a Prepaid plan and a 529 savings plan?

It depends on your risk tolerance. Prepaid locks in Florida public tuition but caps growth at inflation. A 529 savings plan pursues market returns and covers housing, books, or out-of-state costs. Many families pair a two-year Prepaid contract for certainty with a low-fee 529 for everything else.

Still have a question? Drop it in the comments, or open an account and let compounding do the talking.

Conclusion

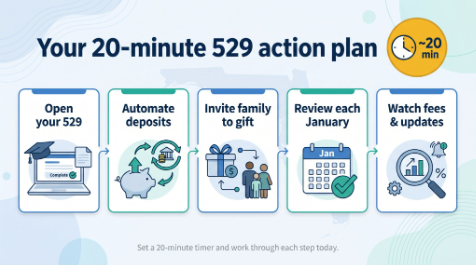

Your 20-minute action plan

- Open a plan today. Pick the plan that fits your style—maybe Utah for custom control or Illinois for rock-bottom fees—and click “Open account.” Keep the child’s Social Security number handy; it is the only curveball in the form.

- Automate contributions. Link your checking account and schedule a monthly draft. Even $100 a month can grow to about $35,000 over 18 years at a six-percent annual return.

- Invite the cheering section. Inside your dashboard, create a gifting link or ugift code. Send it to grandparents before the next birthday so each $50 gift becomes future tuition, not clutter.

- Review once a year. Every January, confirm that contributions continue and that the glide path still matches your time horizon. If college is less than three years away, shift some dollars to a conservative or stable-value option to lock in gains.

- Stay curious. Bookmark fee-change notices from your plan and Morningstar’s annual 529 report. When a plan cuts costs, you benefit automatically.

Set a timer for twenty minutes, start at step one, and let compound interest handle the rest.