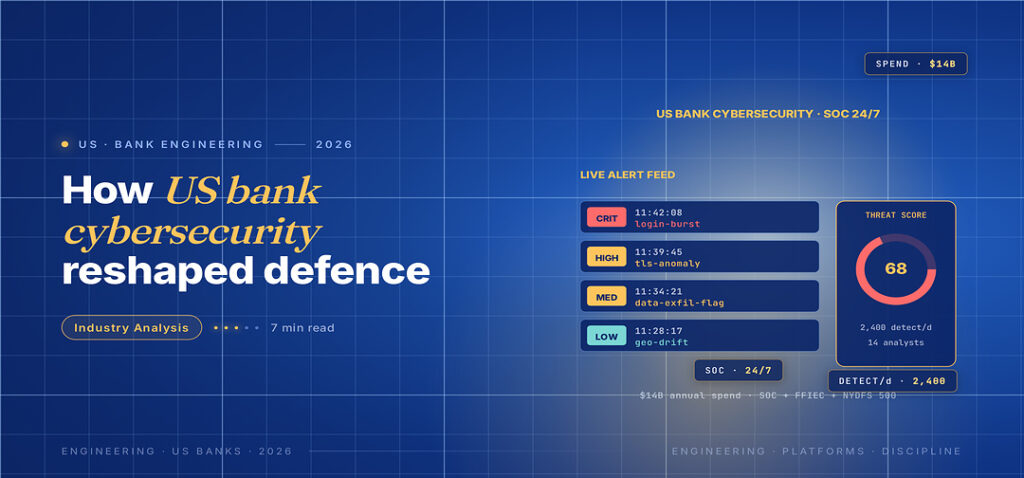

At 3:14 a.m. on a Sunday in March, the security operations centre at a top-five US bank caught a credential stuffing attack from a botnet running across seventeen countries. Within forty minutes the team had blocked the campaign, rotated the affected service account keys, and filed the required SAR. The customer-facing impact was zero. The cost of preventing that single incident, prorated across the bank’s overall cybersecurity budget, ran into the low single-digit millions. That kind of routine, expensive defensive work now consumes more than fourteen billion dollars a year across the US financial sector, and the shape of how the money is spent has changed enough to be worth a closer look.

What US financial cybersecurity actually covers in 2026

The cybersecurity function inside a US bank or large fintech covers at least seven distinct programmes. Identity and access management is the largest of these, both in budget and in operational risk weight. Threat detection and response sits next to it, with security operations centres now running on SIEM platforms (Splunk, Microsoft Sentinel, Sumo Logic) augmented by SOAR automation and increasingly by purpose-built AI assistants.

Data security covers tokenisation, encryption-in-transit and at-rest, plus the data loss prevention controls. Vulnerability management runs continuous scanning and patching pipelines across thousands of services. Application security has shifted left, with SAST, DAST and SBOM tracking embedded in CI pipelines rather than running as a separate compliance gate. Cloud security has its own posture management tooling and shared responsibility model with AWS, Azure and Google Cloud. Third-party and vendor risk now consumes a non-trivial share of the budget thanks to recent supply chain incidents.

The threat surface has expanded faster than headcount. The same fintech that operated on twenty internal services in 2019 now runs hundreds of microservices, several thousand API endpoints, multiple cloud accounts and an increasingly federated workforce. The US payment rails fintechs sit on are favourite targets, and the cybersecurity programmes that defend them have evolved accordingly.

How US banks and fintechs now organise the defensive function

The organisational pattern that has emerged at the largest US institutions has three layers. A central CISO function owns strategy, policy, governance and the relationship with the board and regulators. A platform security team builds the tooling, the detection content and the automated response playbooks that the rest of the organisation consumes. A federated security engineering capability embeds inside product engineering teams to handle threat modelling, code review and security-relevant design decisions at build time.

The shift from a centralised gating model to a federated build-time model has been the most consequential cultural change. Security teams that act as gatekeepers tend to be circumvented. Security teams that act as platform providers, with golden paths and high-quality defaults, tend to be used. The largest US banks have spent the last three years rebuilding their internal security tooling around the platform model, and the defect rates in production have responded accordingly.

Regulatory expectations have also tightened. The SEC’s cyber disclosure rule, finalised in 2023, requires public companies to disclose material cybersecurity incidents within four business days. The NYDFS Part 500 amendment in late 2023 raised the bar on CISO governance, multi-factor authentication and incident response testing. The OCC, Federal Reserve and FDIC issued joint guidance on third-party risk in mid-2023 that has reshaped vendor management programmes across the industry. ACH-related fraud remains a regular discussion topic across these regulatory regimes.

The CISO reporting line at the largest US banks has elevated. Most now report directly to the CEO or a board-level technology and risk committee. The change reflects the speed at which cyber incidents can affect a bank’s reputation, customer trust and regulatory standing. A CISO who used to manage a fifty-person team a decade ago now oversees several hundred and influences capital allocation decisions across product, infrastructure and partnership.

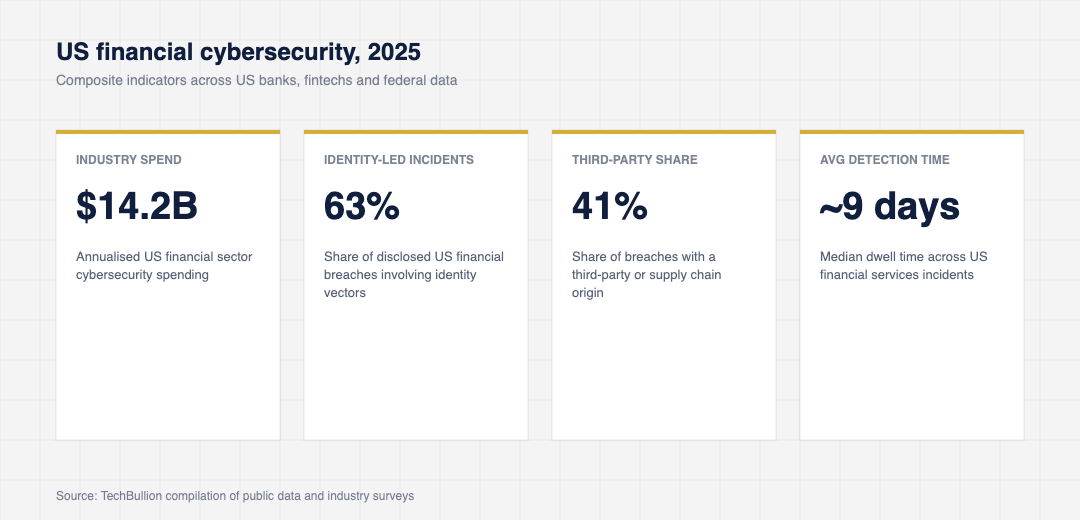

A scoreboard for US financial cybersecurity in 2025

The composite figures below pull from FBI IC3 data, the Verizon DBIR, Mandiant M-Trends, the FFIEC examination findings, and recently disclosed cybersecurity spending breakdowns from the top-25 US banks.

The numbers that have moved the most are the share of incidents involving identity (credential stuffing, social engineering, MFA fatigue) and the share of breaches involving third-party access. Identity-related incidents now dominate the top of the list, which has shifted budgets toward IAM, phishing-resistant authentication (FIDO2, passkeys), and identity governance. Third-party incidents have prompted a re-think of vendor risk programmes, with continuous monitoring replacing point-in-time questionnaires.

Zero trust architecture has moved from buzzword to baseline. Most large US banks have rebuilt their internal network model around identity-based access rather than network-perimeter controls, and the major vendors (Zscaler, Netskope, Cloudflare, Palo Alto Networks) have shipped financial-services-specific reference architectures. The migration is not finished at any institution, but the direction of travel is clear and is reflected in regulatory expectations.

The threats that still keep US bank CISOs awake

Three categories of threat dominate the 2026 CISO conversation. The first is ransomware against critical third parties. The 2023 MOVEit incident, the 2024 Snowflake-customer incident wave and several smaller supply-chain compromises showed that the most dangerous incidents often start outside the bank’s perimeter. Defending against this requires investing in vendor visibility and rapid incident communication paths.

The second is AI-augmented social engineering. Voice cloning, deepfake video and language-model-generated phishing have lowered the cost of high-quality social engineering by an order of magnitude. Bank fraud teams have responded with behavioural biometrics, out-of-band confirmations and customer education campaigns, but the threat surface keeps expanding.

The third is the convergence of cyber and fraud. The traditional separation between cyber (breaches, intrusions) and fraud (account takeover, payment fraud) has dissolved at most large US banks. A modern incident typically involves both teams, and the operating model is still being worked out. Banking innovation that scales globally increasingly depends on resolving this organisational seam between cyber and fraud.

Insurance economics have tightened too. Cyber insurance premiums for large US banks roughly tripled between 2021 and 2024 and have since stabilised, but underwriters now require evidence of MFA coverage, endpoint detection, immutable backups and tested incident response before issuing or renewing coverage. The insurance market has effectively become a private regulator of cybersecurity hygiene across the US financial sector.

What US fintech founders should understand about cybersecurity now

For a US fintech founder building anything that handles consumer or business money, three rules apply. The first is that the regulatory floor is non-negotiable. Multi-factor authentication, encryption at rest and in transit, role-based access control and immutable audit logging are not advanced features. They are the baseline. A fintech that tries to ship to a regulated partner bank without these will lose the partnership during due diligence.

The second is that incident readiness matters more than incident prevention. Every fintech will have an incident at some point. The ones that survive have rehearsed runbooks, clear customer communication templates, established legal and regulatory notification paths, and a board-level conversation about cyber that started before the incident. The ones that do not survive usually learn this during the first serious event, when it is too late.

The third is that the talent strategy is a real lever. The strongest CISOs available to US fintechs are now compensated competitively with engineering leads, and the security engineers who can ship platform-level controls (rather than only audit ones) are among the most valuable hires a young fintech can make. The total cost of getting cyber wrong, in regulatory fines, customer attrition and remediation expense, is much higher than the cost of getting the hiring right.

The Sunday-morning incident that ended with zero customer impact is the visible artefact of an invisible discipline. The $14 billion the US financial sector now spends on that discipline is the price of operating at the scale and speed customers expect, and the operators who treat that spend as an investment rather than a cost tend to outlast the operators who do not.

For threat-landscape context across the US financial sector, see the FS-ISAC Navigating Cyber 2024 threat report.