U.S. personal finance apps are in a strange position in 2026. The category lost its most recognizable brand when Intuit shut down Mint at the start of 2024. At the same time, the population using personal finance apps weekly has grown to roughly 38% of U.S. adults, the highest share ever recorded by Federal Reserve consumer surveys. The category is bigger than it has ever been, the user base is more sophisticated, and the leading apps look almost nothing like Mint did.

What replaced Mint is not a single dominant successor. Monarch, Copilot, Rocket Money, YNAB, Empower, and Apple Wallet’s own savings and budgeting features have together absorbed most of the abandoned audience. The newer entrants have stronger unit economics, are better integrated with the underlying data aggregators, and have built features around real consumer behavior rather than around the assumption that users will manually categorize every transaction.

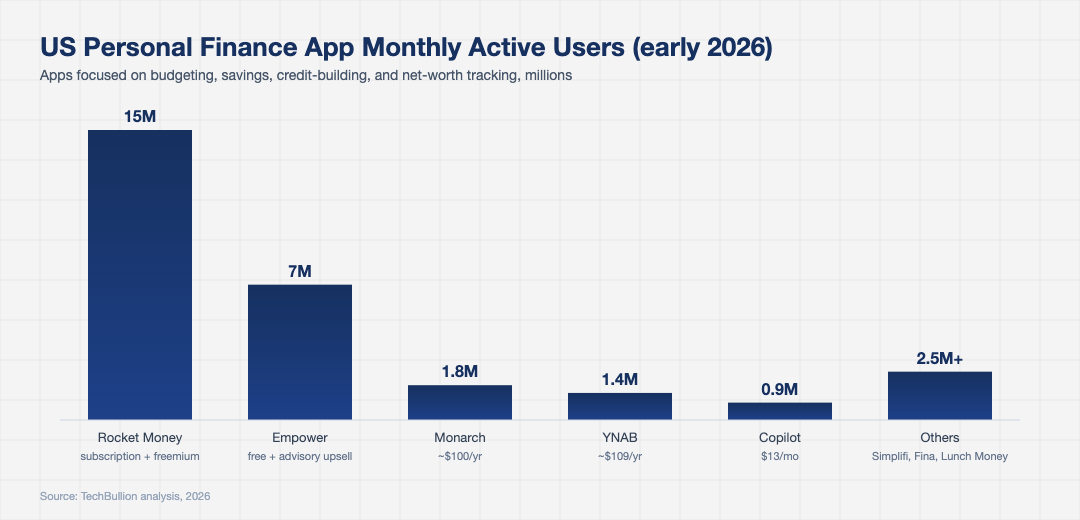

The state of US personal finance app usage in 2026

Apptopia and Sensor Tower data for early 2026 show roughly 95 million U.S. monthly active users of personal finance apps, counting only apps focused on budgeting, savings, credit-building, and net worth tracking. Robinhood, Cash App, Venmo and the brokerage apps are excluded from that count. The leaders by MAU are Rocket Money at roughly 15 million, Empower (formerly Personal Capital) at around 7 million, Monarch at 1.8 million, YNAB at 1.4 million, Copilot at 0.9 million, and a long tail of newer entrants that includes Fina, Lunch Money and Quicken Simplifi.

Behind the user counts is a meaningful shift in demographics. The 2025 Federal Reserve Survey of Consumer Finances found that under-35 U.S. adults are now twice as likely as over-55 adults to use a budgeting or net-worth app weekly. That pattern reverses what the personal finance category looked like a decade ago, when it skewed older and higher-income. The newer apps have specifically optimized for the cohort that does most of its banking on a phone and rarely sees a printed statement.

The features that actually drive retention

Several years of A/B testing across the category have converged on a small number of features that meaningfully affect user retention. The first is automatic and reliable transaction categorization. The user does not want to label every Starbucks coffee. The apps that use Plaid, MX and Finicity data combined with custom merchant-name resolution achieve roughly 92% categorization accuracy out of the box, according to Monarch and Copilot product disclosures from 2025. That accuracy threshold is what separates apps users stay with from apps they uninstall.

The second is goals and savings automation. Apps that let a user set a target, automatically pull money toward it from checking, and adjust the pull rate based on cash-flow signals retain users at noticeably higher rates than apps that simply report on activity. Capital One’s 360 Performance Savings, Ally Bank’s buckets, and the savings features inside Cash App, Chime and Apple Wallet have all been built around this insight.

The third is bill management. Rocket Money built much of its growth on automated subscription cancellation and bill negotiation, and the feature has remained sticky because most U.S. households do not realize the cumulative dollar amount of their recurring subscriptions until an app shows it to them in one view. Truebill, Bobby, and several smaller apps have built versions of the same idea, and the major banks have begun shipping equivalents inside their own apps.

The fourth is credit-building. Self, Credit Karma, Experian Boost and a few newer entrants have built products that report on-time rent and utility payments to the major bureaus, which can move a low-credit-file user’s score meaningfully in months. The product category overlaps with personal finance apps and has, in many cases, been absorbed inside them.

How AI agents have changed the user experience

The most visible product shift in U.S. personal finance apps in 2025 and 2026 has been the introduction of conversational AI. Copilot, Monarch and several smaller apps have added chat interfaces that let users ask plain-English questions about their spending, set budgets through conversation, and get advice on specific scenarios. The underlying models are usually Claude, GPT-4 class, or fine-tuned variants of them, fed scoped access to the user’s transaction history.

The results are mixed. The strongest implementations, particularly Copilot’s Sherlock assistant and Monarch’s AI-powered insights, have meaningfully improved the rate at which users actually act on what their app tells them. The weaker implementations are essentially chat skins that do not deliver more value than a well-designed dashboard would. The category as a whole is still working out which conversational interactions are genuinely better than visual ones.

The regulatory framing for these features is also developing. The CFPB and the FTC have signaled that an AI agent giving specific financial advice may, depending on the framing, trigger fiduciary or registration obligations. Most personal finance apps in 2026 are careful to frame outputs as educational rather than advisory, and most route specific advice questions through a clear disclosure.

The monetization rebuild after the Mint shutdown

The single most consequential strategic question across the U.S. personal finance category in 2026 is how to make money sustainably. Mint’s shutdown was widely interpreted as Intuit acknowledging that ad-supported personal finance does not work at the scale needed to fund development against an aggressive consumer-product roadmap. The successors have mostly chosen subscription pricing.

Monarch charges roughly $100 per year, YNAB roughly $109, Copilot $13 per month, Rocket Money offers a freemium tier with paid features at $4 to $12 per month. Quicken Simplifi sits in the same range. The subscription model has stronger retention dynamics because users who pay are more likely to use, and users who use are more likely to pay. The category has effectively traded mass-market scale for sustainable per-user economics, and the financial results so far suggest the trade was the right one.

An interesting wrinkle is the bank-bundled model. Several U.S. banks, including Capital One and Chase, have begun licensing personal finance app features from third-party vendors and including them in their primary banking apps without an additional charge to customers. That is a credible threat to the standalone subscription model, but only at the apps that have not built a meaningfully differentiated product. The standalone apps that have continue to grow.

Where US personal finance apps are headed next

Three trends will define the next phase. The first is Section 1033 data portability. The CFPB’s 2024 final rule on personal financial data rights, which begins phased implementation in 2026, gives U.S. consumers an enforceable right to share their banking, credit card, payment and investment data with third-party apps. The practical effect is more reliable data, lower aggregator fees, and stronger competition between apps that can demonstrate quality of insight rather than quality of integration.

The second is the merger of personal finance apps with treasury management for sole proprietors and creators. The line between household and small-business finance is blurry for the roughly 30 million U.S. adults with side income, and several apps have begun building features specifically for that audience. Quicken and FreshBooks have both moved in this direction, and Monarch has launched a small-business beta.

The third is the expansion into goals beyond budgeting. Apple Wallet’s high-yield savings account, Robinhood Gold’s checking and brokerage bundle, and the savings features inside Chime and Cash App have all blurred the boundary between personal finance app and bank account. By 2027 it will be normal for a U.S. consumer’s primary financial app to combine deposit accounts, budgeting, credit-building, savings goals and brokerage access in a single interface. The standalone personal finance app category will remain valuable, but the most successful entries will either become full financial homes or remain as best-in-class niche tools used alongside a broader app.

The summary is that U.S. personal finance apps in 2026 are healthier than they have been in years. The category lost a brand and gained a market structure. The leaders are operating on real subscription revenue, building real product, and integrating new technology in measured ways. The next two years should see continued consolidation around a smaller set of well-funded apps that compete on insight and behavior change rather than on feature count.