Sit in on the morning standup of any U.S. fintech that processes more than a billion dollars a year in 2026, and the same three roles will be in the room: a treasury lead reviewing yesterday’s settlement, a risk lead surfacing the queue of held-for-review transactions, and an engineering lead reading the auth-rate dashboard to spot regressions. Ten years earlier those three people would have been in three different meetings at three different times of day. The function that has emerged to glue them together is payment operations management, and in 2026 it is the discipline that increasingly determines whether a U.S. fintech runs at the same operational quality as the major banks. The discipline is new enough that the job titles are still settling, and important enough that almost every company doing serious payments volume is now investing in it ahead of the supervisory bar that is rising around it.

What payment operations management actually means

Payment operations management, often abbreviated as PayOps inside fintechs that have adopted the term, is the cross-functional practice of running the day-to-day flow of payments through an organisation. It includes monitoring authorisation rates and intervening when they regress, managing settlement and reconciliation across multiple acquirers and rails, handling exception queues for held or returned transactions, providing treasury with the live view of available cash that real-time banking now requires, and providing risk with the live view of suspicious patterns. The discipline cuts across what used to be three separate departments: finance, risk, and engineering. The reason it had to become a single function is that the rails it sits on stopped operating on overnight cycles.

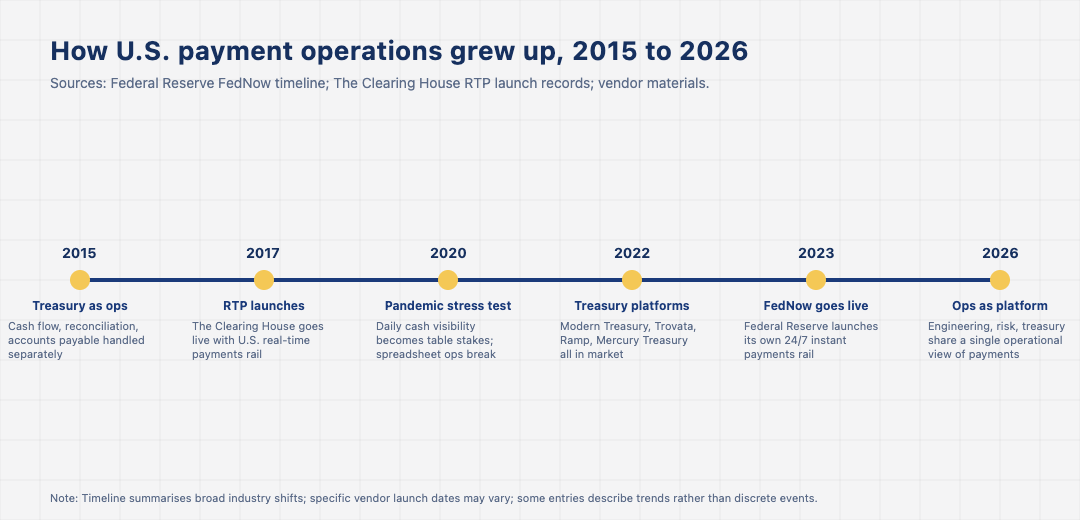

Before the introduction of FedNow in 2023 and the maturation of The Clearing House’s RTP rail, U.S. payment operations could afford to be a daily-batch process. Banks moved files overnight; reconciliation happened in the morning; exceptions were worked through during business hours and resolved within a day. With instant rails, the same operational model breaks down. A payment that arrives at 2 am needs to be acknowledged, recorded, and reconciled before the next one arrives at 2:01 am. The cumulative effect of moving multiple rails to 24/7 is that the back office has to be 24/7 too, which is impossible without significant automation, and the automation only works if the underlying ledger is event-driven rather than batch-driven.

The vendor layer that has emerged

The infrastructure that supports U.S. payment operations management in 2026 is mostly built on a small number of vendor categories. Modern Treasury, founded in 2018, is the most explicitly positioned PayOps platform, providing a unified API and dashboard for managing money movement across multiple bank rails. Trovata, Tesorio, and Nilus offer treasury-side platforms that provide the live cash view. Ramp, Brex, and Mercury Treasury have built operations layers into their broader product set. The acquirer-side equivalents are Stripe Treasury, Adyen for Platforms, and Square Banking, all bundled into the broader PSP product but accessed through the same operational dashboards.

The architecture pattern that has emerged is convergence: the platforms that started as treasury-only are adding risk and engineering surfaces, the platforms that started as engineering-only are adding treasury and risk surfaces, and the difference between them is increasingly the centre of gravity of the team that bought them. The competitive question for the next several years is whether the category consolidates into a smaller number of platforms or remains a layered stack of specialists. Some early signals point to consolidation: Modern Treasury has steadily added risk surfaces, while Stripe Treasury continues to absorb adjacent functionality and several smaller specialists have been quietly acquired through 2024 and 2025. The TechBullion piece on payments systems and infrastructure covers the broader rail set this all sits on.

The metrics that actually matter

The maturity of a U.S. fintech’s payment operations function in 2026 can be inferred from a small number of metrics. The first is auth rate variance. A well-run operation has an auth rate that is stable to within a few basis points day to day, with regressions investigated within hours. The second is reconciliation lag. The leading edge of the category reconciles all rails to within minutes; the lagging edge runs daily. The third is exception-queue dwell time. A modern operation moves transactions out of held queues within hours; a less mature one lets them sit for days. The fourth is incident response time when something breaks. A mature operation has runbooks, dashboards, and on-call rotations that look like an engineering ops team. A less mature one has people emailing screenshots.

None of these metrics are externally reported in any standardised way, but they correlate strongly with the kind of public outcomes investors do see: net dollar retention, fraud-loss ratios, and the operational margin of the payments business unit. Companies that invest in payment operations early tend to outgrow the competitors that defer it, in a pattern that has become legible enough that investors now ask about it explicitly during fundraises. Several diligence frameworks circulating among payment-focused VCs in 2025 included a payment operations maturity scorecard as a standard checkbox. The TechBullion piece on why banking infrastructure is becoming digital sets out how this fits with the broader vendor landscape.

The supervisory expectations that are tightening

Bank regulators have been increasingly explicit through 2024 and 2025 that operational maturity is a supervisory matter. The OCC, the Federal Reserve, and the FDIC have all issued or refreshed guidance on payments operational risk that touches on the same issues fintechs are addressing internally: real-time settlement, third-party risk, exception management, and the controls that surround them. For fintechs that operate through bank partnerships, these expectations cascade through the partner bank into contractual requirements that the fintech has to meet to keep the partnership. For fintechs that operate as banks themselves, the expectations apply directly.

The practical effect on companies that have invested early in PayOps is minimal: they were already meeting the standard before it was formalised. The effect on companies that deferred the investment is a sometimes-painful catch-up project that often starts with hiring an experienced payment operations leader and ends with replacing several pieces of infrastructure. Either way, the supervisory direction reinforces the trajectory the category was already on, which is toward a higher operational baseline that all U.S. fintechs of any meaningful scale will eventually have to meet.

What founders and operations leaders should design for

For founders building any product that touches money movement at meaningful scale in 2026, the practical implications are: hire for PayOps earlier than feels necessary, pick a treasury and ops platform before the cost of doing it manually becomes the binding constraint, design from day one for 24/7 rails rather than overnight batch, and assume the supervisory bar will continue to rise across the rest of the decade. The companies that internalise these decisions early have a structural operational advantage. The TechBullion piece on why banking innovation is accelerating worldwide situates the U.S. PayOps story alongside the broader global pattern, where the same convergence is visibly underway in the U.K., Brazil, and India ahead of the U.S. on several specific dimensions.

Payment operations management in the U.S. in 2026 is what banking back-office work looked like in the 1990s, except faster, more visible, and more cross-functional. The discipline did not exist as a named function ten years ago. It is now the connective tissue between treasury, risk, and engineering at every meaningful U.S. fintech. The companies that build it well will be the ones that can grow without operational disasters in the rest of the decade. The companies that defer it will find that the rails do not wait, and that the cost of catching up rises faster than the volume that drove the need.