SHAP values, the SHapley Additive exPlanations attribution method derived from cooperative game theory, have become the dominant explainability technique in U.S. financial machine learning. The technique is now standard in credit underwriting, fraud detection, marketing-response modelling, and any other category where supervisors expect explainable outputs from otherwise complex models. The interesting questions are no longer whether to use SHAP but how to use it well, where its limitations bind, and how to integrate SHAP outputs into the regulatory and operational workflows that surround financial machine learning.

This piece looks at where SHAP values have settled in U.S. finance, the implementation patterns that work, the misuses that cause supervisory problems, and the operational disciplines that make SHAP useful rather than performative.

The technique that became the supervisory default

SHAP became the supervisory default for model explainability in U.S. finance through a combination of factors. The technique has a clean theoretical foundation, produces additive explanations that decision-makers can interpret without specialised training, and works across most of the model families used in production. The Federal Reserve, OCC, and CFPB all reference SHAP-style attribution in supervisory feedback as an acceptable approach to model explainability.

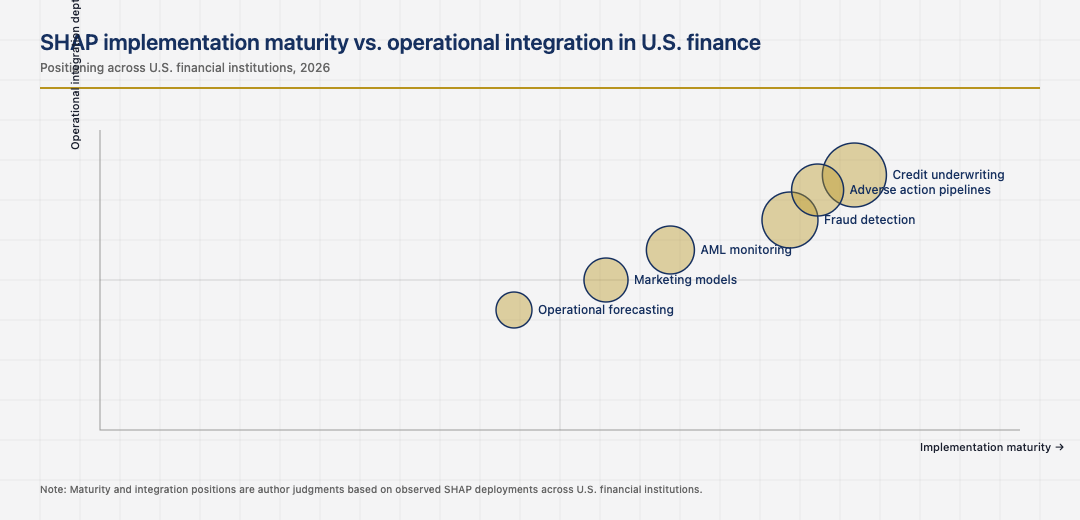

The institutions that adopted SHAP early built the supporting infrastructure for it. SHAP value computation at production scale, SHAP-based monitoring dashboards, and SHAP-driven adverse-action notices all became standard tooling. The institutions that did not adopt SHAP early have either restricted their model deployment to simpler models or now face the cost of building SHAP infrastructure under regulatory pressure.

Implementation discipline and the latency tradeoff

SHAP value computation is computationally expensive. The full Shapley calculation is exponential in the number of features and intractable for typical financial models. Production implementations use approximations: TreeSHAP for tree-based models, KernelSHAP for general black-box models, and DeepSHAP for neural networks. Each approximation has its own tradeoffs between speed and fidelity.

The institutions that match the SHAP variant to the model family produce explanations that are both fast enough for production use and accurate enough for supervisory defensibility. The institutions that try to use the most general approximation universally usually face latency problems that limit operational use. The discipline of matching the SHAP variant to the model is unglamorous and consequential.

The limitations and the misuse patterns

SHAP has limitations that mature implementations respect. Feature correlation produces unstable attributions across runs. Interaction effects are summarised but not always preserved cleanly. The choice of background dataset for the Shapley calculation can shift the attributions meaningfully. The institutions that document these limitations and design around them produce trustworthy SHAP outputs. The institutions that present SHAP attributions without acknowledging the underlying tradeoffs usually find their explanations questioned by supervisors who have seen too many overconfident SHAP-based justifications.

The misuse pattern that draws the most supervisory attention is using SHAP to justify model behaviour after the fact rather than to interrogate model behaviour during development. Models that were not designed for explainability and then have SHAP attached late in development usually produce SHAP outputs that confirm the model’s existing decisions without surfacing the underlying biases or edge cases that should have been addressed earlier. The mature pattern is using SHAP throughout development as a tool for understanding and improving the model, not just at deployment as a tool for justifying it.

Adverse action notices and the customer-facing application

U.S. credit decisioning models are subject to adverse action notice requirements when an application is declined or offered worse terms than requested. The notice must explain the reasons for the decision in terms the consumer can understand. SHAP attribution has become the standard mechanism for producing these reasons in machine-learning-based credit decisions. The institutions that built clean SHAP-to-adverse-action pipelines satisfy the regulatory requirement while still using modern modelling techniques. The institutions that did not have either restricted themselves to simpler models or face the cost of building the pipeline under regulatory pressure.

The discipline that makes SHAP-based adverse action notices work is mapping SHAP attributions to consumer-friendly reason codes that the consumer can act on. Raw SHAP values are not consumer-friendly. The translation from SHAP attribution to readable reason requires careful design. The institutions that invested in this translation deliver notices that satisfy regulators and inform consumers. The institutions that did not deliver notices that satisfy neither.

The next phase of SHAP and explainability in U.S. finance

The next phase is shaped by the integration of SHAP-style attribution with large language model explanations, the maturation of alternative explainability techniques like counterfactual analysis, and the continuing supervisory pressure for explainable model deployment. The institutions that built strong SHAP infrastructure in the previous phase will absorb these changes cleanly. The institutions that did not will continue to face the choice between simpler models and a costly retrofit of explainability tooling onto more complex ones.

Read across the full picture, SHAP values in U.S. finance in 2026 are a settled supervisory default with specific implementation patterns: matching SHAP variants to model families, respecting the technique’s limitations, using SHAP throughout development rather than only at deployment, and translating SHAP attributions into customer-friendly outputs. The institutions that respect them deliver trustworthy explanations. The institutions that miss any one usually have explainability that satisfies the supervisor’s filing requirements but not the supervisor’s substantive questions.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.

Last updated: June 17, 2026