The phrase “evolution of banking” tends to attract a particular kind of slide deck. A timeline runs from the Medici family through the joint-stock bank to the iPhone wallet. The story is true. It is also incomplete. The most consequential evolution of American banking is happening right now, and the evidence for it sits inside the boring details of how banks fund themselves, supervise themselves, and partner with the technology firms that increasingly own their customer experience.

This piece looks at where U.S. banking is actually evolving in 2026: the deposit franchise, the credit franchise, the partnership perimeter, the supervisory perimeter, and the architectural rebuild that ties them together. The framing favours operators making decisions about competitive position rather than narrators describing a settled past.

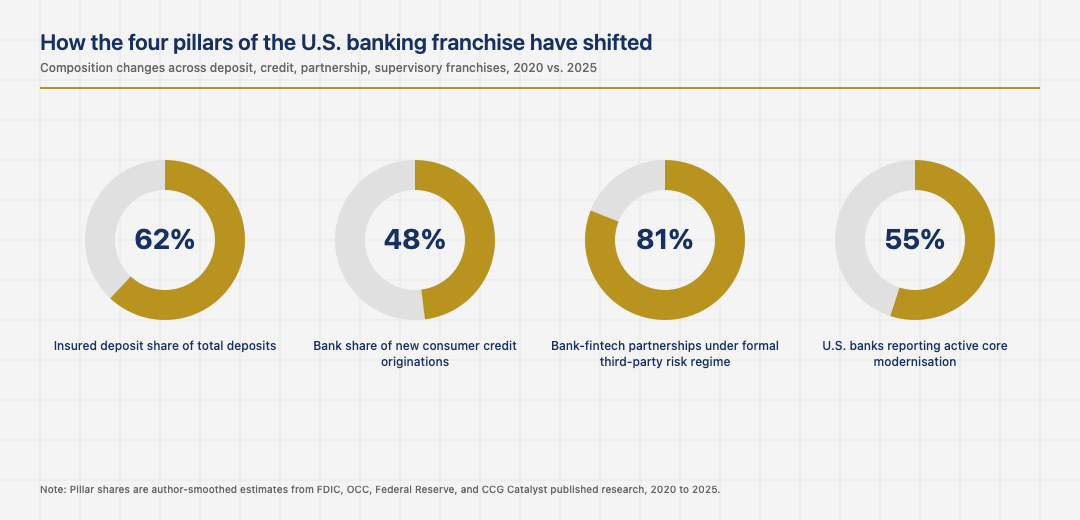

The deposit franchise has lost its certainty

For most of the postwar era, U.S. bank deposits were the cheapest, stickiest funding source in the financial system. The 2023 regional banking stress changed that. High-velocity digital deposit movement, social-media-driven runs, and depositor concentration in uninsured tiers all forced supervisors and bank treasurers to reread their own franchise. The result is a banking system that pays more for funding, manages liquidity more conservatively, and prices customer relationships with new precision.

The competitive implication is that the value of a sticky retail deposit base has gone up, not down. Banks with diversified, granular, primarily insured deposits are now meaningfully more valuable than banks with concentrated commercial deposits and uninsured tiers. The deposit franchise is the franchise again, in a way it had not been since the 1970s, and the operators who internalised that early are accumulating share at the expense of the ones who treated deposits as a commodity.

The credit franchise is more contested than ever

U.S. bank lending faces structural competitive pressure from non-bank lenders across nearly every category. Private credit funds have taken share in middle-market commercial lending. Marketplace lenders have taken share in unsecured consumer credit. Buy-now-pay-later providers have taken share in retail point-of-sale financing. Regional banks find themselves competing for the same loan with non-bank capital that does not have to hold the same regulatory capital against it.

The bank response has been a combination of capital efficiency improvements, partnerships with non-bank originators, and selective retreat from segments where the regulatory capital cost makes the lending uneconomic. The result is a credit market in which the marginal U.S. consumer or small-business loan is increasingly originated by a non-bank, sometimes funded by a bank, often securitised through a structure that diffuses the credit risk across pension funds and insurance balance sheets.

The partnership perimeter has hardened

The bank-fintech partnership model is the structural innovation of the past decade. The Synapse collapse in 2024, the OCC’s tightened third-party risk guidance, and several enforcement actions against sponsorship banks have all combined to harden the perimeter of what those partnerships look like. Banks now demand higher capital reserves, deeper compliance integration, more conservative end-user fund handling, and clearer wind-down playbooks from their fintech partners.

The partnerships that survive this hardening are stronger and more limited. The ones that do not survive get unwound, often through forced migrations of end-user balances to other sponsorship banks. The medium-term consequence is a more concentrated bank-fintech partnership market in which fewer banks act as sponsors, the ones who do are larger and better resourced, and the fintech partners that win their attention have to come with a level of operational maturity that prior cycles did not require.

The supervisory perimeter is wider and clearer

U.S. banking supervision has expanded in scope and clarity over the past two years. The CFPB’s 1033 final rule sets the customer data perimeter. The OCC’s third-party risk guidance sets the partnership perimeter. The Federal Reserve’s stress tests have been recalibrated for the post-SVB era. The combined effect is a supervisory environment that asks more of banks but tells them more clearly what is being asked.

For operators, the practical consequence is that the supervisory clock and the product clock are increasingly synchronised. New product launches require supervisory engagement earlier in the development cycle. Partnership structures require third-party-risk diligence that takes weeks rather than days. The operators who plan for this cadence ship their products with fewer surprises. The operators who treat supervision as a final-stage hurdle find their launches delayed in ways that compound across the year.

The architectural rebuild and the next decade

Underneath all four of these shifts sits a quiet architectural rebuild. Core banking modernisation programs at major U.S. institutions have moved from PowerPoint into production. The shift from monolithic mainframes to modular cloud-native cores is uneven, expensive, and structurally permanent. Vendors like Thought Machine, 10x Banking, and FIS Modern Banking Platform are seeing real production deployments, not just pilot programs.

The reason this matters is that the next decade of bank competitive position will be defined by the speed at which a bank can launch and modify products. Modernised cores enable that speed. Legacy cores constrain it. The operators who finish their core modernisation programs in this cycle will compound their advantage in the next cycle. The ones who defer it will spend the next decade explaining to their boards why their cost-to-launch ratio is structurally worse than the competitor’s.

Read across these five dimensions, U.S. banking in 2026 is in the middle of a more profound evolution than the surface narrative suggests. The deposit franchise has been revalued. The credit franchise has been redistributed. The partnership perimeter has been hardened. The supervisory perimeter has been widened. The architectural foundation is being rebuilt in production. The banks that internalise the full picture and build for it are the ones who define the next decade. The ones who treat any single dimension as the whole story underestimate what is actually happening.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.