Stablecoins have become one of the most practical yield instruments in crypto. The shift is structural, not cyclical. Supply has expanded into the hundreds of billions, with USDT and USDC dominating liquidity, and capital is increasingly being deployed not for speculation, but for income generation.

At the same time, traditional savings products have not kept pace. In Europe, bank deposits still yield roughly 1%–3% annually. Stablecoin markets operate under different constraints, and that gap is what makes this segment suitable for getting passive income in crypto.

Key Takeaways

- Stablecoins allow you to earn yield without exposure to crypto price volatility.

Most sustainable returns in 2026 cluster between 3% and 8%, with higher yields tied to higher risk structures. - CeFi, DeFi, and yield-bearing assets each offer different trade-offs between simplicity, control, and risk.

- Liquidity and transparency matter more than headline APY.

- Platforms that combine fiat access with crypto savings reduce friction and improve capital efficiency.

How Stablecoins Differ From Regular Savings Accounts

A bank savings account is fundamentally a liability on a bank’s balance sheet. The bank controls how deposits are used, and returns are shaped by central bank policy and regulatory constraints.

Stablecoins operate in open markets. They are used as working capital across exchanges, lending protocols, and trading desks. That capital is constantly borrowed, redeployed, and repriced.

Instead of fixed rates determined by a bank, stablecoin yields reflect real-time demand for liquidity. Access is continuous, and the infrastructure is often transparent, especially in DeFi. But with more flexibility comes higher yield, though without the protections of traditional deposit systems.

Fiat vs Stablecoins Savings

| Feature | Bank Savings | Stablecoin Savings |

| Currency | EUR, USD | USDT, USDC, DAI |

| Access | Limited hours | 24/7 |

| Yield source | Bank lending | Crypto borrowing demand |

| Transparency | Opaque | Often on-chain |

| Rates | Low | Market-driven |

Why Interest Rates on Stablecoins Are Higher Than Banks

The difference in yield comes down to how capital is sourced and used.

Banks rely on a mix of deposits and central bank funding. That reduces their need to compete aggressively for retail capital. Stablecoin markets do not have that advantage. Borrowers—traders, market makers, institutions—need immediate access to dollar liquidity, and they pay for it.

That demand drives yields upward. When borrowing activity increases, rates follow. When demand slows, yields compress.

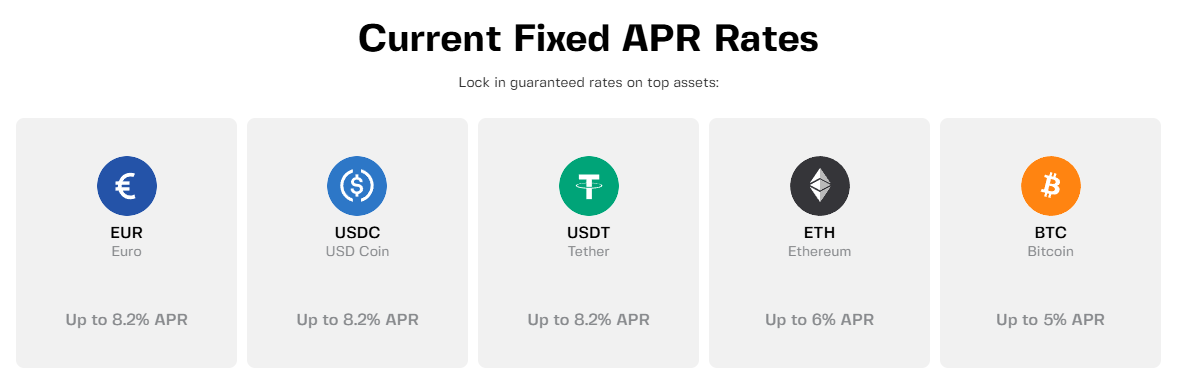

In practice, this results in a broad range. Conservative lending markets such as Aave or Compound typically offer 2%–6% APY. More structured or custodial platforms can reach 6%–8% or higher. For example, Clapp.finance offers 5.2% APR on stablecoins on flexible saving accounts, and on fixed accounts the rates reach over 8%.

Main Ways to Earn Interest on Stablecoins

The stablecoin yield landscape has matured into three distinct models. Each reflects a different balance between usability and control.

1. CeFi (Centralized Finance)

Centralized platforms remain the most accessible. You deposit USDT or USDC, and the platform lends it onward to borrowers. The experience resembles a digital savings account. Rates are predictable, and the operational burden is minimal. The trade-off is custodial exposure—you rely on the platform’s risk management and solvency.

Clapp fits into this category but extends it. It combines savings with fiat on/off-ramps. Users can deposit Euros via SEPA and start earning instantly. Clapp also offers portfolio tools, and credit access, thus integrating yield into a broader financial workflow. You can move between euros and stablecoins, allocate funds, and manage positions without leaving the platform.

2. DeFi (Decentralized Finance)

Decentralized finance takes a different route. You supply liquidity directly into lending markets. Protocols such as Aave or Compound determine rates algorithmically based on utilization. This removes intermediaries and increases transparency, but it requires active management and a clear understanding of smart contract risk.

3. Structured and Hybrid Yield

A third category has emerged around structured yield. These strategies combine lending, liquidity provision, and sometimes derivatives or real-world asset exposure. They can improve returns but introduce additional complexity and layered risk.

How to Start Earn Stablecoin Yield on Clapp

For users who want to get passive income on stablecoins without managing multiple platforms, the process is straightforward. Clapp is a crypto-financial platform that combines trading, savings, and payments in one app. It supports both fiat and crypto deposits with no fees, making it a practical entry point for earning yield on USDT or USDC.

- Create an account and deposit funds

You begin by funding your account. Clapp supports both fiat and crypto deposits, with no fees on either side. That removes a common friction point at the entry stage.

- Convert to stablecoins (if needed)

Once funds are available, you can convert euros into stablecoins directly within the app. From there, you choose how to allocate capital.

- Choose a savings product

Clapp offers two types of savings accounts:

Flexible savings accounts prioritize liquidity. Funds remain accessible at all times, interest accrues daily, and compounding happens automatically .

Fixed savings accounts take a different approach. You commit funds for a defined period and lock in a higher rate, which remains stable regardless of market changes.

From that point, the system is passive. Interest accrues in the background, and you can withdraw or reallocate capital depending on the structure you chose.

What matters here is not just yield. It is the ability to move between fiat and crypto, manage savings, and deploy capital without switching platforms.

Key Factors That Affect Earnings

Stablecoin yield is dynamic. It reflects underlying market conditions rather than fixed promises.

Borrowing demand is the primary driver. When traders need leverage, rates increase. When markets are quiet, yields decline.

Liquidity also plays a role. Fully flexible products typically offer lower returns than fixed-term deposits, because the capital can be withdrawn at any time.

The structure of the yield matters as well. Lending-based yield tends to be more stable. Incentive-driven yield—where platforms distribute tokens—can inflate APY figures but may not be sustainable.

Understanding these differences is more important than comparing headline rates.

Risks to Consider

Stablecoins reduce price volatility, but they introduce a different set of risks.

Custodial platforms carry counterparty risk. If a platform mismanages funds or faces liquidity issues, withdrawals may be affected.

DeFi protocols eliminate that layer but introduce smart contract risk. Exploits, bugs, or governance failures can result in losses.

There is also asset-level risk. Not all stablecoins are equal in terms of transparency and backing. Historical issues around reserve disclosures have shown that this risk is not theoretical.

Regulation adds another dimension. As stablecoins become more integrated into financial systems, oversight is increasing, which may affect available yield products.

How to Maximize Stablecoin Yield Safely

A practical approach is to separate capital by function. Keep a portion in liquid accounts for flexibility. Allocate another portion to fixed-term products for higher returns. Use DeFi selectively if you understand the mechanics.

Diversification across platforms reduces dependency on any single provider. Transparency should guide allocation decisions. If the source of yield is unclear, the return is difficult to evaluate.

The objective is not to extract the highest possible APY. It is to build a stable, repeatable income stream.

Stablecoins Can Serve a Passive Income Tool

Stablecoins now sit between traditional savings and capital markets. They provide access to yield without exposure to volatility, and they operate on infrastructure that allows capital to move continuously.

The advantage is not only higher returns. It is efficiency. Funds can be deployed, withdrawn, and redeployed without friction.

Platforms that combine savings, fiat integration, and portfolio tools make this model practical. They reduce the operational overhead that used to define crypto yield strategies.

For investors focused on passive income in crypto, stablecoins are no longer a secondary option. They are a core allocation layer—one that prioritizes consistency over speculation and turns idle capital into a productive asset.