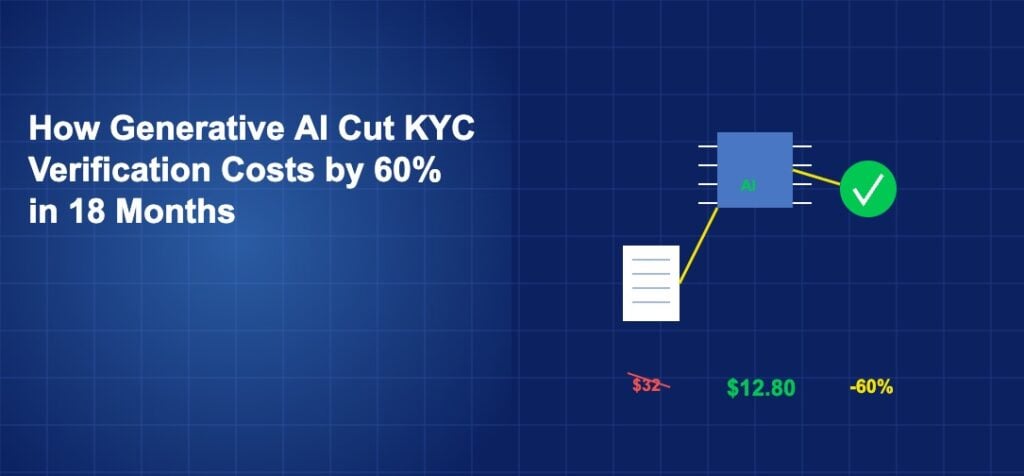

Generative AI has cut the cost of know-your-customer verification by 60% in the past 18 months. Banks and fintech companies that processed KYC checks at an average cost of $32 per customer in mid-2024 now spend $12.80 using AI-automated workflows, according to a McKinsey analysis published in January 2026. The shift did not happen through one product or one vendor. It happened because large language models became capable of reading, extracting, and cross-referencing identity documents at a speed and accuracy that manual reviewers cannot match.

What KYC Costs and Why It Matters

Global spending on KYC and anti-money laundering compliance reached $61 billion in 2025, according to LexisNexis Risk Solutions. That figure includes staff costs, technology, regulatory filings, and the revenue lost from slow onboarding processes. For a mid-size bank processing 200,000 new accounts per year at $32 each, KYC alone costs $6.4 million annually.

The time cost compounds the dollar cost. Manual KYC review takes an average of 24 hours per consumer account and up to 90 days for corporate accounts with complex ownership structures. During that wait, potential customers abandon applications. A 2025 survey by Signicat found that 68% of consumers in Europe had abandoned a financial product application due to a lengthy identity verification process.

Over 70% of financial institutions are investing in fintech partnerships, and KYC automation is one of the most common starting points for those partnerships.

How Generative AI Changes the Process

Traditional KYC automation used optical character recognition (OCR) to read documents and rules-based systems to flag mismatches. These systems were brittle. A passport photographed at an angle, a utility bill in a non-standard format, or a corporate filing in a foreign language would fail automated processing and require human review. The fallback rate for traditional OCR-based KYC systems averaged 35%, according to Accenture.

Large language models reduce the fallback rate to under 8%. They can read documents in over 100 languages, interpret handwritten text, extract data from non-standardized formats, and reason about whether information across multiple documents is consistent. A customer submits a passport, a bank statement, and a utility bill. The AI reads all three, verifies that the name, address, and date of birth are consistent, checks the passport against known forgery patterns, and produces a risk score. The entire process takes under 90 seconds.

Fintech platforms are growing faster than traditional banks, and faster KYC is one of the reasons. A fintech that onboards customers in two minutes captures the applicants that banks lose during a two-week manual review.

The Vendors Building AI-Powered KYC

Several companies have emerged as leaders in AI-powered KYC. Onfido, acquired by Entrust in 2024, processes over 30 million identity verifications annually using a combination of document analysis and biometric liveness detection. Jumio has verified over 1 billion identities since its founding and reported that its AI models reduced false rejection rates by 43% between 2024 and 2025.

Chainalysis and Elliptic, originally focused on blockchain analytics, now offer AI-powered KYC for crypto exchanges and traditional financial institutions. Persona, a San Francisco-based identity platform, raised $200 million at a $1.5 billion valuation in 2025 to expand its AI verification capabilities, per Crunchbase.

The large cloud providers are also competing. AWS offers Amazon Textract for document processing and Amazon Rekognition for facial matching. Google Cloud provides Document AI. Microsoft Azure has Form Recognizer. These general-purpose tools are being packaged into KYC-specific workflows by system integrators and specialized fintech companies.

Fintech infrastructure platforms represent a $150 billion opportunity, and identity verification infrastructure is one of the fastest-growing segments.

Regulatory Acceptance and Limitations

Regulators are cautiously accepting AI-powered KYC. The Financial Action Task Force published guidance in October 2025 stating that AI-based identity verification is acceptable under its recommendations, provided that institutions maintain human oversight for high-risk cases and can explain how AI decisions are made.

The EU’s AI Act, which takes full effect in August 2026, classifies AI used for biometric identification as high-risk, requiring conformity assessments, documentation, and human oversight. Financial institutions using AI for KYC in Europe must register their systems, conduct regular audits, and demonstrate that the AI does not discriminate based on race, gender, or national origin.

In the United States, the OCC and FinCEN issued joint guidance in 2025 permitting AI-assisted KYC, with the caveat that banks remain responsible for compliance regardless of the technology used. If an AI system approves a customer who later turns out to be on a sanctions list, the bank bears the regulatory penalty, not the AI vendor.

Global fintech revenue is expected to grow at a 23% CAGR, and compliance technology is growing even faster. The regtech market, which includes KYC, AML, and sanctions screening, is projected to reach $44 billion by 2028, according to Grand View Research.

What Comes Next

The 60% cost reduction is likely the beginning, not the end. As AI models improve and training data expands, fallback rates will continue to drop. Perpetual KYC, where AI continuously monitors customer data for changes rather than checking once at onboarding, is already in pilot at several large banks. HSBC and Standard Chartered both reported running perpetual KYC programs using AI in their 2025 annual reports.

Fintech adoption rates surpass 64% globally, and frictionless onboarding powered by AI is one of the drivers of that adoption. The $61 billion spent on KYC and AML compliance globally is a cost that AI is compressing rapidly. The banks and fintechs that adopt fastest will onboard customers faster, at lower cost, and with lower abandonment rates.

The direction of this market is clear even if the precise timeline remains uncertain. The underlying technology and business model advantages that are driving these shifts will only strengthen as adoption scales and competition intensifies. The organisations and institutions that position themselves on the right side of these trends now will be best equipped to thrive in the financial services landscape of the next decade.

The competitive dynamics are shifting in favour of organisations that combine technological capability with deep market understanding. Pure technology plays without industry expertise struggle to navigate regulatory complexity and customer trust requirements. Legacy institutions without modern technology struggle to match the speed and cost efficiency of digital-first competitors. The winners will be those that bring both elements together effectively.