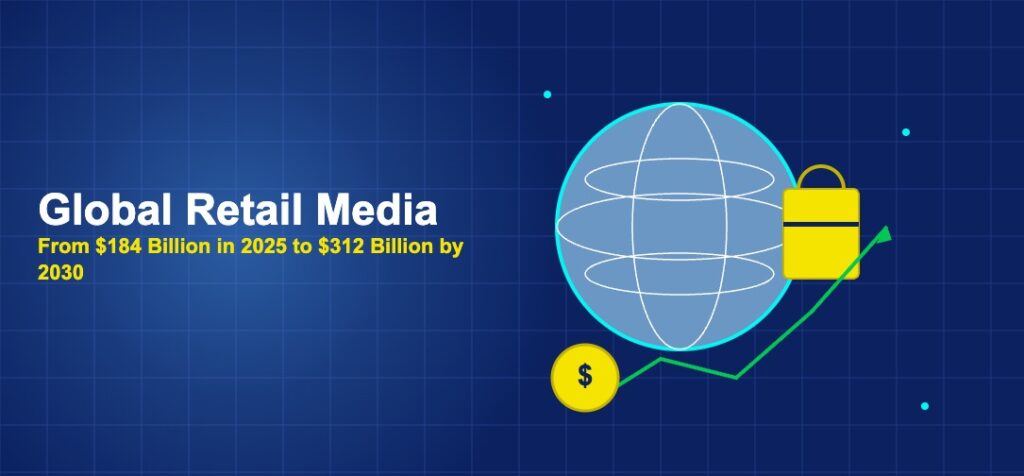

Global retail media advertising revenue reached 184 billion dollars in 2025, establishing it as one of the fastest-growing segments in the worldwide advertising industry. Projections from leading research firms indicate this figure will climb to 312 billion dollars by 2030, representing a compound annual growth rate of approximately 11.2 percent over the five-year period.

The expansion of retail media from a primarily US phenomenon into a global advertising category marks a significant shift in how consumer brands approach marketing worldwide. What began as sponsored product listings on Amazon has evolved into a sophisticated global advertising ecosystem spanning dozens of countries, hundreds of retail platforms and virtually every product category sold to consumers.

The 184 billion dollar global figure for 2025 reflects contributions from every major market. The United States accounts for roughly 37 percent of global retail media spending, followed by China at 28 percent, the United Kingdom at 7 percent, Germany at 5 percent and Japan at 4 percent. The remaining 19 percent is distributed across dozens of smaller markets, many of which are experiencing growth rates that exceed even the global average.

Regional growth patterns shaping the global market

North America remains the most mature retail media market, with the United States leading global spending at approximately 69 billion dollars in 2025. Canada contributes an additional 4.2 billion dollars, with retail media adoption accelerating among Canadian retailers who have studied the success of their American counterparts. The North American market is expected to grow at roughly 14 percent annually through 2030, somewhat slower than the global average due to its relative maturity.

The Asia-Pacific region represents the most dynamic growth opportunity in global retail media. China’s retail media market, dominated by platforms like Alibaba, JD.com and Pinduoduo, reached an estimated 52 billion dollars in 2025. Unlike Western markets where retail media evolved from e-commerce advertising, Chinese platforms have integrated advertising so deeply into the shopping experience that the boundary between content, commerce and advertising has largely disappeared.

Southeast Asian markets including Indonesia, Thailand, Vietnam and the Philippines are experiencing retail media growth rates exceeding 30 percent annually. Platforms like Shopee and Lazada have built advertising businesses that mirror the models pioneered by Amazon and Alibaba, adapted for markets where mobile commerce dominates and average order values are lower. India’s retail media market is also expanding rapidly, driven by Flipkart, Amazon India and the emerging advertising capabilities of quick-commerce platforms like Blinkit and Zepto.

European retail media growth has been steady if less spectacular than Asian markets. The United Kingdom leads the continent with approximately 13 billion dollars in retail media spending, driven by sophisticated advertising platforms operated by Tesco, Sainsbury’s and Amazon UK. Germany, France and the Netherlands have all developed active retail media ecosystems, though regulatory frameworks around data usage have shaped the development of European retail media in ways that differ from the US and Asian models.

Technology infrastructure enabling global scale

The technology platforms underpinning retail media have evolved significantly as the market has scaled globally. First-generation retail media technology consisted primarily of basic sponsored product placements managed through simple self-service interfaces. Current platforms offer sophisticated programmatic buying capabilities, real-time bidding, cross-channel campaign management and advanced analytics powered by machine learning.

Cloud infrastructure investments by major retail media platforms have been substantial. Amazon, Walmart and other leading retailers have built dedicated advertising technology stacks that process billions of bid requests daily, serve personalized ad creative in milliseconds and provide advertisers with near-real-time reporting on campaign performance. These systems require significant ongoing investment but generate returns that justify the expenditure through advertising revenue margins that typically exceed 70 percent.

The emergence of retail media management platforms has facilitated the market’s growth by reducing complexity for advertisers operating across multiple retail media networks. Companies like Criteo, CitrusAd and Pacvue provide unified interfaces that allow brands to manage campaigns across dozens of retail media platforms from a single dashboard. These intermediary platforms have been particularly important for mid-market brands that lack the resources to maintain dedicated teams for each retail media network.

Data clean room technology has become increasingly important as retail media scales globally. These secure computing environments allow retailers and advertisers to combine their respective datasets for targeting and measurement purposes without either party exposing raw data to the other. The adoption of data clean rooms has been accelerated by privacy regulations in Europe and growing privacy consciousness in other markets, providing a technical solution that satisfies both regulatory requirements and advertiser demand for data-driven targeting.

Advertiser adoption across industries

The advertiser base for global retail media has expanded well beyond the consumer packaged goods companies that were early adopters. While CPG brands still account for the largest category of retail media spending at approximately 32 percent globally, other industries are increasing their investments at faster rates. Technology and electronics brands now represent 16 percent of global retail media spend, followed by health and wellness at 13 percent, apparel and fashion at 11 percent and home goods at 8 percent.

Financial services companies represent one of the most interesting emerging categories in retail media. Banks, insurance companies and fintech firms are using retail media platforms to reach consumers at moments of purchase intent, leveraging retailer data to identify audiences with specific financial needs. This category grew by an estimated 45 percent in 2025 and is expected to continue expanding as retailers develop more sophisticated audience targeting capabilities.

The automotive industry has also begun directing meaningful budgets toward retail media, particularly in markets where vehicle accessories, parts and related services are sold through online retail platforms. While the absolute spend remains modest compared to traditional automotive advertising channels, the growth trajectory suggests that retail media will become a standard component of automotive marketing strategies within the next several years.

Small and medium-sized businesses represent a significant growth opportunity for retail media globally. Self-service advertising tools offered by major platforms have lowered the barriers to entry, allowing businesses with modest marketing budgets to participate in retail media. Amazon’s advertising platform alone serves over three million active advertisers, the majority of which are small businesses spending less than one thousand dollars per month.

Challenges and opportunities on the path to 312 billion dollars

Despite strong growth projections, the global retail media market faces several challenges that could influence its trajectory toward 312 billion dollars by 2030. Measurement standardization remains an unresolved issue, with different platforms using different methodologies to count impressions, attribute sales and report return on advertising spend. The lack of common standards makes it difficult for advertisers to compare performance across platforms and allocate budgets optimally.

Regulatory risk represents another potential headwind. European regulators have already imposed restrictions on how retail platforms can use consumer data for advertising purposes, and similar regulatory frameworks are under development in other jurisdictions. While retail media’s reliance on first-party data provides some insulation from privacy regulations, the evolving regulatory landscape could constrain certain targeting capabilities and increase compliance costs for retail media operators.

The concentration of retail media spending among a small number of platforms creates competitive concerns that could attract regulatory scrutiny. In the United States, Amazon captures roughly 73 percent of all retail media spending, a level of market dominance that exceeds even Google’s share of search advertising. Regulators in multiple jurisdictions have begun examining whether dominant retail platforms are leveraging their market position to disadvantage competing advertisers or extract excessive fees from brands.

Despite these challenges, the fundamental drivers of retail media growth remain strong. The continued shift of consumer purchasing toward digital channels creates more advertising inventory, the deprecation of third-party cookies increases the value of retailer first-party data, and the measurable performance of retail media campaigns makes it easier for marketers to justify budget increases. These structural tailwinds suggest that the 312 billion dollar projection for 2030 is achievable and potentially conservative, particularly if emerging markets accelerate their adoption of digital commerce and the retail media advertising models that accompany it.

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.