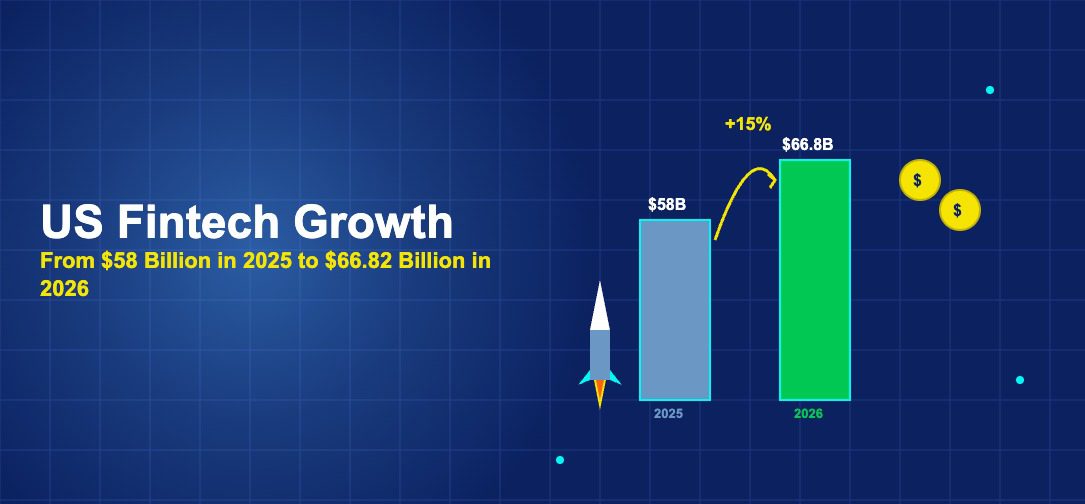

US fintech growth in 2025 and 2026 is entering a distinct phase compared to the 2018-2022 expansion cycle. The prior cycle was characterized by low interest rates enabling cheap capital, rapid customer acquisition at any cost, and valuation multiples that rewarded growth over profitability. The current cycle is characterized by higher-for-longer interest rates, profitability requirements from investors, selective capital availability, and a focus on unit economics rather than gross volume metrics.

This shift has produced a more selective fintech market. Companies with sustainable business models,genuine revenue advantages, defensible customer relationships, and paths to profitability,are growing and attracting capital. Companies that relied on cheap money and growth-at-all-costs strategies have contracted, been acquired, or failed. The survivors entering 2025-2026 are generally stronger businesses than the broader cohort that raised capital in 2020-2021.

Payment Fintech Growth Drivers

Digital payment fintech growth in 2025-2026 is driven by the continuing shift from cash and check to digital payment methods, cross-border payment expansion, and the monetization of payment data for adjacent financial services. US card payment volume continues to grow at 5-8% annually as consumers shift from cash to card, from card to digital wallet, and as B2B payments increasingly digitize.

PayPal’s growth strategy under CEO Alex Chriss focuses on profitable growth rather than gross payment volume. PayPal is investing in branded checkout optimization (making PayPal’s consumer checkout experience faster and more compelling to drive preference), Venmo monetization (converting Venmo’s social payment network into a revenue-generating financial platform), and advertising capabilities that leverage PayPal’s transaction data. These initiatives are expected to drive PayPal revenue growth of 5-8% in 2025-2026, a modest but sustainable rate for a mature fintech.

Stripe’s growth remains strong at 20%+ annually as internet commerce continues expanding and Stripe penetrates larger enterprise accounts. Stripe Terminal (in-person payments), Stripe Treasury (banking-as-a-service), and Stripe Capital (business lending) are extending Stripe’s revenue streams beyond payment processing. Stripe’s ability to retain and expand its revenue from existing customers,through cross-selling financial infrastructure products,is the primary growth driver for 2025-2026.

Block’s Cash App has become a significant financial platform for the underbanked population. Cash App’s active users spend an average of $50+ annually on fees and services, representing meaningful per-customer monetization for a free-to-use product. Block’s integration of Bitcoin trading within Cash App drives revenue during crypto market upturns and creates customer engagement that persists across market cycles. Block’s Square business faces competition from Toast (restaurants) and Shopify (e-commerce) but maintains strong positions in small business payment processing.

Neobank Growth Dynamics

US neobank growth in 2025-2026 is driven by continued customer acquisition from traditional banks, deeper product penetration within existing customer bases, and the maturation of lending and credit products that generate higher revenue per customer than basic deposit accounts.

Chime’s growth has been constrained by regulatory challenges related to its banking-as-a-service partnerships. Chime operates without a bank charter, relying on partner banks (Bancorp Bank and Stride Bank) for deposit accounts and card issuance. This model has faced scrutiny from the CFPB regarding consumer protection practices. Chime has adapted by improving its dispute resolution processes and adding the “bank” terminology it previously avoided (the CFPB had required it to clarify it is not a bank). Despite these challenges, Chime continues to grow its customer base and is preparing for an IPO.

SoFi’s growth in 2025-2026 benefits from its bank charter, which enables it to offer higher-yielding savings accounts funded by deposits rather than expensive wholesale funding. SoFi’s member growth,exceeding 10 million members by early 2025,and product diversification (banking, lending, investing, insurance distribution) create a compounding revenue advantage. Each new product adopted by an existing member increases revenue per customer without significant incremental acquisition cost.

Newer neobanks targeting specific demographics,Daylight (LGBTQ+), First Boulevard (Black Americans), Nerve (musicians), Lili (freelancers),have grown more slowly than generalist neobanks. Community-focused neobanks can build strong loyalty within their target segments but face customer acquisition and scale challenges that make achieving profitability difficult without outside capital.

BNPL Recovery and Credit Fintech

Buy-now-pay-later (BNPL) fintech is recovering from the 2022-2023 credit quality deterioration. Affirm, the largest publicly traded BNPL company in the US, has improved its credit model by focusing on longer-duration installment loans (which have lower default rates than short-term BNPL), partnering with more creditworthy merchant categories (travel, healthcare, B2B software), and raising underwriting standards for new borrower cohorts.

Affirm’s growth in 2025-2026 is driven by its partnership with Apple Pay Later’s discontinuation,Apple terminated its BNPL product in 2024 and integrated Affirm into Apple Pay in certain markets. Affirm also maintains major partnerships with Amazon and Shopify that provide substantial transaction volume. Affirm’s Gross Merchandise Volume (GMV) is expected to reach $30-35 billion in fiscal 2026, up from approximately $25 billion in fiscal 2025.

Klarna, the Swedish BNPL company with significant US operations, filed confidentially for a US IPO in 2024. Klarna has been improving profitability through cost reduction and revenue expansion into advertising services for its merchant network. The US market is a major growth focus for Klarna, where it competes with Affirm and Afterpay for BNPL market share. Klarna’s US revenue growth in 2025-2026 is expected to be in the 20-30% range as BNPL penetration of US retail continues expanding.

Investment Fintech Growth

Retail investment fintech is experiencing renewed growth after the post-2021 correction. Robinhood’s revenue grew 50%+ in 2024, driven by crypto trading recovery, Gold subscription growth, and expansion into new asset classes. Robinhood’s customer base,primarily younger investors with lower average account balances than traditional brokerage customers,is a valuable demographic for long-term product development but challenges immediate revenue generation per account.

The retirement savings market represents a significant growth opportunity for investment fintechs. Betterment and Wealthfront are expanding their retirement account offerings (IRA, 401k) to capture savings that traditionally went to Fidelity, Vanguard, and Schwab. The automation advantage of robo-advisors,automatic rebalancing, tax-loss harvesting, portfolio optimization,is particularly valuable for retirement savers who prefer set-it-and-forget-it investing. Capturing even a small share of the $35+ trillion US retirement savings market represents a substantial growth opportunity.

Regulatory Environment and Fintech Growth

The regulatory environment for US fintech in 2025-2026 is more complex than in the 2018-2022 growth phase. The CFPB has been active in fintech oversight, issuing rules on earned wage access, BNPL disclosure requirements, and data access rights under Section 1033 of the Dodd-Frank Act. These regulations impose compliance costs but also create opportunities: standardized data access rules under Section 1033 enable open banking, which is favorable for fintechs that benefit from consumer financial data portability.

The OCC’s conditional approval of fintech bank charters has been slow, with only a handful of companies receiving national bank charters. The bank charter pathway is valuable for fintechs because it enables deposit-taking without partner bank dependence, but the regulatory requirements are substantial. Fintechs operating through partner banks (banking-as-a-service models) face increasing regulatory scrutiny of the partner banks themselves, which creates compliance obligations that flow through to the fintech clients.

Despite regulatory headwinds, the structural growth drivers for US fintech remain intact. Consumer preference for digital financial services continues shifting younger demographics from traditional banks. Small business financial services,historically underserved by large banks,remain a large opportunity for fintech platforms with technology advantages in underwriting, onboarding, and product delivery. B2B financial infrastructure (embedded finance, API banking, real-time payments) is growing as more software companies integrate financial services into their platforms.

According to CB Insights’ 2024 fintech report, global fintech funding declined 40 percent between 2022 and 2024, pushing the sector toward consolidation and a sharper focus on profitability over growth at all costs.

The Boston Consulting Group projects fintech revenues will reach $1.5 trillion by 2030, with embedded finance and digital lending accounting for the largest share of projected growth.