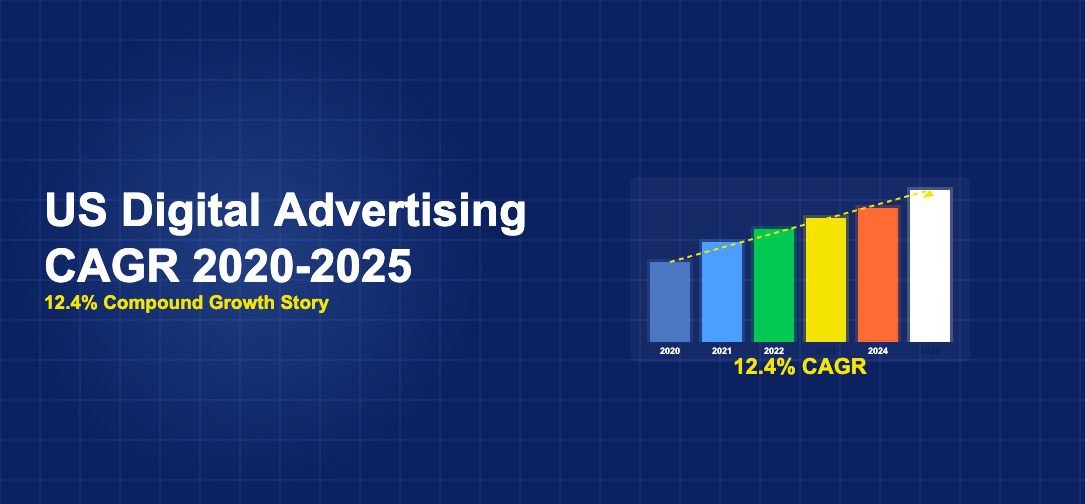

, every year between 2020 and 2025, the US digital advertising market added more money than the entire industry had earned in any single year before 2010. The cumulative gain over those five years came to roughly $210 billion. A compound annual growth rate smooths all of it into one number: 12.4%.

That figure does not announce itself. It sits quietly in the footnotes of eMarketer&’s forecast reports, where it is easy to treat as a background detail rather than the central fact. But 12.4% compounded annually for five consecutive years means the market did not just grow. It doubled. It crossed $300 billion for the first time, then added another $60 billion on top of that before the period closed.

The five years between 2020 and 2025 compressed what might otherwise have taken a decade into half the time. Understanding that rate, and the conditions that held it together, matters for anyone trying to read where US digital advertising goes from here.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

The Numbers Behind the Rate

eMarketer puts total US digital advertising spend at approximately $152 billion in 2020. By 2025, that figure stood at $361.9 billion, the largest single market total in the history of the medium and the largest dollar gain on record for a single year. The 12.4% CAGR is the smoothed annualised rate of expansion across the full five-year arc.

What that rate does not show is how unevenly the growth distributed across the period. 2021 was the standout year: brands that had cut budgets in the first half of 2020 returned to market simultaneously, competing for the same digital inventory at a moment when e-commerce adoption had permanently shifted consumer behaviour. Spend jumped by roughly $59 billion in twelve months, the largest single-year dollar increase the market had recorded to that point.

2022 and 2023 were slower by comparison, as inflation began squeezing consumer spending and advertisers recalibrated after the third-party cookie deprecation timeline made programmatic planning more uncertain. Growth continued, but the pace moderated. Then 2024 and 2025 delivered a second acceleration, driven by connected TV, retail media networks, and the improved targeting accuracy that AI-optimised platforms had been building toward for several years.

Four Conditions That Held the CAGR Together

A compound growth rate this consistent across five years is not a coincidence. Four structural conditions reinforced each other throughout the period.

The first was mobile penetration. Smartphone adoption in the United States did not plateau during this period. It deepened, reaching into demographics and usage patterns that had previously underindexed. More time on mobile meant more inventory, more auctions, and more reach into the moments that used to belong exclusively to television. Mobile advertising&’s share of total digital ad spend grew through the period, and the additional volume gave platforms more signal to work with, improving targeting quality in a feedback loop that made spend more efficient year after year.

The second was the structural shift of commerce online. The pandemic compressed several years of e-commerce adoption into months. Once those purchasing habits locked in, they created a permanent demand for performance-oriented digital advertising. Brands that had relied on in-store discovery had to build digital acquisition capabilities quickly. Retail media networks grew to meet that demand, giving advertisers access to first-party purchase-intent data at a scale that search and social could not replicate. By 2025, US retail media advertising was approaching $70 billion on its own.

The third was the expanding inventory base. The period saw Netflix, Disney+, and Hulu each launch or expand advertising tiers, bringing connected TV into the mainstream of digital ad buying. CTV inventory carried television-level CPMs but digital-level targeting and measurement, which made it attractive to budgets that had never previously touched streaming. Every new premium inventory pool that entered the programmatic ecosystem gave advertisers somewhere productive to put incremental spend.

The fourth was measurement improvement. AI-optimised bidding, better attribution modelling, and the slow but steady build-out of privacy-preserving measurement frameworks gave advertisers more confidence that their spend was working. Higher measurable ROI is one of the most reliable drivers of higher ad budgets, and the period from 2020 to 2025 delivered consistent improvement in advertisers&’ ability to demonstrate returns from digital channels.

How 12.4% Compares

Putting the CAGR in context requires a comparison. Over the same 2020 to 2025 window, US GDP growth averaged approximately 5.1% annually in nominal terms. Total global advertising spend grew at a rate well below the US digital figure, held down by slower-growing traditional formats and smaller international markets. Even within digital advertising globally, the US rate outpaced the world average, reflecting the concentration of platform investment and advertiser sophistication in the American market.

The figure also sits above the long-term CAGR for US digital advertising going back to the mid-2000s, when the industry was expanding from a much smaller base. Growing at 12.4% annually on a base that was already $152 billion is a materially different achievement from growing at the same rate on a base of $15 billion. The compounding math at scale is harder to sustain, which makes the five-year run more significant, not less.

What the Rate Signals Going Forward

The 12.4% CAGR ended in 2025 but the conditions that produced it have not reversed. eMarketer&’s forecasts for 2026 put the US digital advertising market at approximately $413 billion, implying year-on-year growth of around 14%. If that holds, the market will have grown faster in 2026 than the five-year average CAGR suggests, which points to acceleration rather than deceleration at the end of the period.

The drivers are consistent with what held the 2020 to 2025 arc together. Retail media is still growing faster than the broader market. Connected TV is still pulling TV budgets into digital channels. AI-driven performance optimisation continues to improve, keeping spend efficient enough to justify increases. And the underlying scale of the US digital economy, which determines the ceiling for advertising inventory, is still expanding.

That does not mean the rate is permanent. Any significant deterioration in consumer spending, a regulatory shift that materially restricts targeting, or a platform-level disruption could change the trajectory. But as of the close of the five-year period, none of those conditions had materialised at a scale large enough to slow the compound engine below double digits.

The Practical Meaning of Compounding

The most useful way to understand what 12.4% compounding actually produces is in dollar terms. A market that starts at $152 billion and grows at 12.4% annually does not just add $18.8 billion in year one. In year five, the same 12.4% rate applies to a base that is already $320 billion. That means the final year&’s gain, in absolute terms, is more than double the first year&’s gain, even though the rate is identical.

This is why the market added $41.9 billion in 2025 alone. The rate did not accelerate. The base did. And a base that reached $361.9 billion by the end of 2025 means that even a slightly lower rate in 2026 will still generate a larger dollar increase than any previous year. That is the arithmetic of sustained compound growth on a large base, and it is what the US digital advertising market&’s five-year CAGR actually represents.