Sentiment analysis for U.S. financial markets is one of those techniques that has been claimed as a competitive edge for so long that the actual track record gets obscured. The honest reading is that sentiment analysis produces value in specific use cases and produces noise in others. The institutions that have used the technique productively over the past decade have a small set of disciplines that distinguish them from the institutions that produce strong-looking dashboards and weak trading signals.

This piece looks at where sentiment analysis for U.S. markets has settled in 2026, the use cases that consistently deliver value, the failure modes that keep recurring, and the operational disciplines that turn sentiment data into something more useful than headline noise.

News-driven sentiment for short-horizon signals

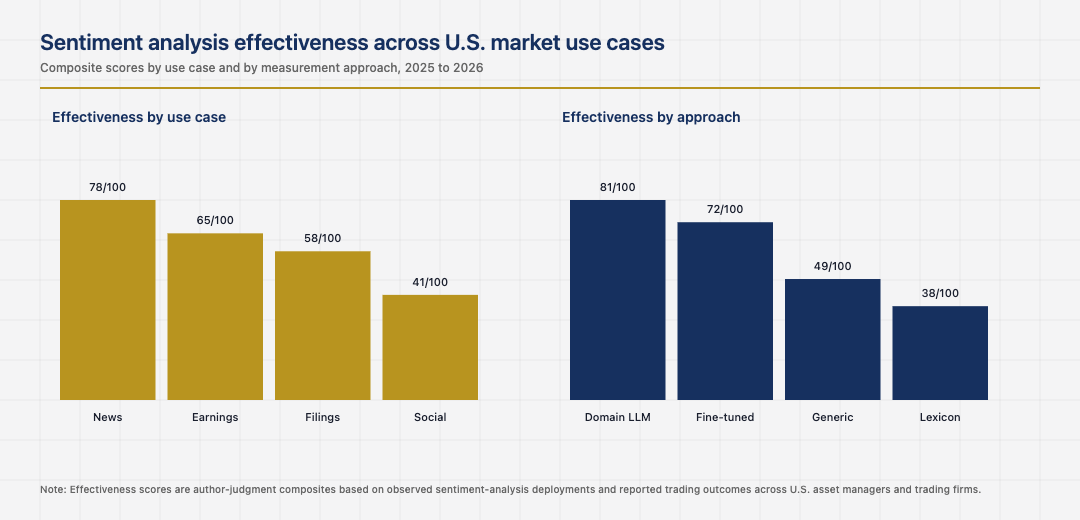

The use case where sentiment analysis has the most consistent track record is short-horizon trading on news flow. The technique processes high-volume news feeds, classifies sentiment per company or sector, and feeds the classified signal into trading systems that act on the news in seconds or sub-seconds. The institutions that built strong news-driven sentiment pipelines captured value that simpler price-only models did not.

The discipline that makes this work is rigorous classification quality. The signal is only as good as the underlying sentiment classification. The institutions that invested in domain-specific classifiers, fine-tuned on financial language, produce signals that are tradeable. The institutions that used generic sentiment models usually produce signals that are too noisy to translate into reliable strategies.

Earnings call sentiment and the longer horizon

Earnings call sentiment is a quieter and well-established use case. The transcripts of earnings calls, conference presentations, and management interviews all contain signal that can be extracted with NLP. The institutions that built earnings-call analysis capabilities produce information that fundamental analysts use to update their models. The information is not directly tradeable as a pure quantitative signal, but it improves the quality of fundamental analysis at scale.

The discipline here is integrating the NLP outputs into the analyst workflow rather than producing them as standalone signals. The institutions that built this integration capture the workflow benefit. The institutions that produced the analytics without the workflow integration usually deliver dashboards that analysts ignore in favour of reading the transcripts themselves.

Social media sentiment and the noise floor

Social media sentiment is where the marketing material most consistently outpaces the production track record. The signal in social media is real but small, the noise is large, and the manipulation risk is meaningful. The institutions that have used social-media sentiment productively have done so as one signal among many, weighted appropriately, and combined with other data sources that provide context.

The institutions that treated social media sentiment as a primary signal usually produced strategies that worked sporadically and failed expensively when manipulation events affected the underlying signal. The discipline of weighting social media signal appropriately, with context from other sources and explicit handling of manipulation risk, is what distinguishes productive use of the data from the casual version.

Domain-specific language models and the recent acceleration

The recent acceleration in sentiment analysis comes from financial-domain large language models. Models fine-tuned on earnings calls, regulatory filings, news flow, and analyst reports outperform generic sentiment models meaningfully on financial text. The institutions that adopted these models early extract more value from their text data than the institutions still using generic sentiment classifiers.

The discipline that makes this work is honest evaluation of the domain-specific models against the institution’s actual use cases. The models that work well on benchmarks may not work as well on the specific text the institution processes. The institutions that evaluate carefully deploy the models that genuinely outperform. The institutions that adopt models based on benchmark scores alone usually find their production performance disappointing.

The next phase of sentiment analysis in U.S. markets

The next phase is shaped by the integration of multimodal signals, the maturation of domain-specific foundation models, and the continuing refinement of sentiment-driven strategies as more market participants use similar techniques. The institutions that built strong sentiment-analysis foundations are well-positioned to absorb these changes. The institutions still chasing social-media-driven alpha will continue to find the technique disappointing.

Read across the full picture, sentiment analysis for U.S. markets in 2026 is a productive technique in specific categories with specific disciplines: news-driven sentiment for short-horizon signals, earnings-call sentiment for longer-horizon fundamental work, careful weighting of social-media signal, and domain-specific models evaluated against actual use cases. The institutions that respect them deliver value. The institutions that miss any one usually deliver dashboards that look impressive and trading signals that disappoint.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.