Executive Summary

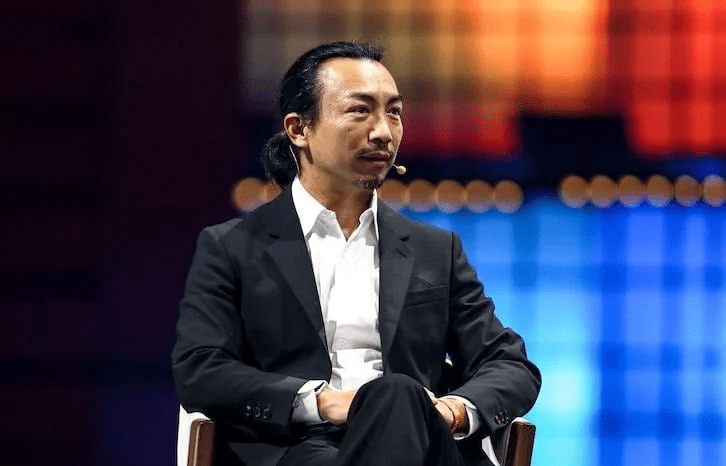

A second federal RICO complaint has been filed against Cere Network CEO Fred Jin and Lime co-founder Brad Bao, bringing total claimed damages to $157 million across two lawsuits in the Northern District of California. The new complaint identifies Jin as the alleged architect of a cryptocurrency fraud scheme and accuses Bao of lending his mainstream credibility and approving key financial decisions from his position on the board. Filed by San Francisco investor Josef Qu (Case No. 3:26-cv-01235), the suit introduces several allegations absent from the first $100 million action filed by Goopal Digital Limited in February: federal securities fraud claims under the Securities Exchange Act, specific blockchain forensic evidence via Etherscan transaction records, a detailed accounting of $16.6 million lost in DeFi protocols, allegations that Jin funded a new AI venture called CEF AI Inc. with stolen investor proceeds, and a request to freeze the defendants’ cryptocurrency wallets, bank accounts, and luxury real estate in Germany and Florida. The complaint names ten causes of action and the same roster of defendants. For anyone following the intersection of crypto fraud litigation and Silicon Valley reputation, this second filing transforms what was already a significant case into something that looks increasingly like a pattern.

Why the Second Lawsuit Changes the Picture

The first Goopal Digital lawsuit against Jin and Bao was filed in February, and at the time the case was already notable: $100 million in RICO claims, a connection to a convicted wash trading firm, and two prominent figures from the tech world named as defendants. The question was whether this would remain an isolated legal action or the beginning of something larger.

Now there is an answer. The Josef Qu complaint filed weeks later is not a copycat suit. It brings substantially new evidence, new legal theories, and new factual allegations that go well beyond the original filing. The combined $157 million in claimed damages is the headline number, but the real story is in the details: securities fraud claims that were not in the first suit, blockchain evidence that was, prior ventures by Jin that establish a pattern of conduct stretching back to 2016, and allegations that proceeds from the alleged Cere Network fraud are being actively recycled into a new AI venture. Each of these elements independently raises the stakes. Together, they create a litigation picture that federal regulators are increasingly likely to notice.

The New Legal Theories: Securities Fraud Enters the Frame

The first Goopal lawsuit asserted six causes of action: RICO, RICO conspiracy, fraud, aiding and abetting fraud, negligent misrepresentation, and breach of advisory and token sale agreements. These are serious claims, but they operate primarily within the framework of racketeering and common law fraud.

The Qu complaint adds four more, and the additions are significant. Securities fraud under Section 10(b) of the Securities Exchange Act prohibits the use of manipulative or deceptive devices in connection with the purchase or sale of securities. Section 20(a) imposes liability on individuals who exercise control over entities that violate securities laws. The complaint also adds theft and breach of the implied covenant of good faith and fair dealing, bringing the total to ten causes of action.

The securities fraud claims matter for several reasons. First, they implicitly argue that CERE tokens are securities under the Howey test, which, if the court agrees, could have implications for similar token offerings industry-wide. Second, the complaint alleges that Jin, as CEO and primary decision-maker, made material misrepresentations to investors about fund usage, lockup restrictions, and the project’s financial health. Third, the Section 20(a) “control person” liability creates a direct legal pathway to hold Bao accountable for his board role, regardless of whether he personally executed the alleged scheme. Fourth, securities fraud claims invite SEC attention in a way that RICO claims alone may not.

The Blockchain Paper Trail: Etherscan Evidence and $16.6 Million in DeFi Losses

If the securities fraud claims represent a legal escalation, the blockchain evidence represents an evidentiary one. The Qu complaint cites specific Etherscan transaction records purporting to show the movement of tokens and funds from Cere Network corporate wallets. This is forensic-grade evidence on a public, immutable ledger, the kind of paper trail that is extremely difficult to dispute or explain away.

The complaint provides a detailed accounting of approximately $16.6 million that was allegedly lost in high-risk decentralized finance investments made with investor capital: $6.51 million in the Mochi Protocol, $3.27 million in a CVX/ETH liquidity pool, $780,000 in Maple Finance, and $345,000 in the Neutrino USDN protocol. The complaint alleges Jin directed these investments without investor consent or disclosure, characterizing them as unauthorized and reckless bets that no fiduciary should have made with funds entrusted by investors.

Both lawsuits allege that additional proceeds from the insider sell-off, totaling approximately $41.78 million, were routed through a network of shell companies registered in Delaware, the British Virgin Islands, Panama, and Germany, and into personal accounts controlled by Jin, his wife Maren Schwarzer, and his brother Xin Jin. The new complaint adds that funds were also used to purchase luxury real estate in Germany and Florida.

The Gotbit Connection: A Convicted Market Maker and New Blockchain Detail

In the first lawsuit, both complaints allege that Jin and his associates engaged Gotbit Ltd. to deploy automated trading bots that conducted wash trading during the November 2021 token launch, generating fake volume to create the appearance of genuine market activity while insiders systematically liquidated their positions.

Gotbit’s founder, Aleksei Andryunin, was subsequently convicted of wire fraud and market manipulation as part of the DOJ’s Operation Token Mirrors, a federal sting operation that targeted crypto market-making firms engaged in wash trading. The Qu complaint adds new blockchain detail to this allegation, citing Etherscan evidence showing token movements from corporate wallets to exchange wallets on the first day of trading. The combination of a convicted market maker and on-chain evidence showing coordinated token movements is a powerful evidentiary pairing.

Funler, Bitlearn, Cere Network, CEF AI: The Serial Venture Allegation

The first Goopal complaint briefly referenced Jin’s involvement in earlier ventures. The Qu complaint expands this into a more detailed narrative of what it characterizes as a repeating pattern.

Before Cere Network, Jin allegedly ran a project called Funler, later rebranded as Funler Chain, between 2016 and 2018. The complaint alleges that Funler raised approximately $10 million from investors before its token lost roughly 95 percent of its value. A subsequent venture called Bitlearn, launched in 2018, allegedly followed an identical trajectory. Cere Network was the third act, raising approximately $42.96 million before its token declined more than 99.8 percent from its launch price.

The fourth act, according to the complaint, is already underway. The filing alleges that Jin has launched a new artificial intelligence venture, CEF AI Inc., funded with proceeds from the alleged Cere Network fraud. The plaintiff is seeking a constructive trust over CEF AI’s assets and injunctive relief to freeze the company’s holdings. If these allegations are substantiated, the implication is stark: the alleged fraud has not ended, it has merely changed industries.

Jin’s Alleged Role as Architect of the Scheme

An honest analysis of this case requires understanding the distinct roles each defendant allegedly played. The complaint identifies Jin as the central figure behind the alleged fraud. As CEO and co-founder of Cere Network, Jin allegedly controlled the treasury wallets, directed the Gotbit wash trading arrangement, authorized the high-risk DeFi investments that lost $16.6 million, and personally oversaw the movement of investor funds into accounts held by himself, his wife Maren Schwarzer, and his brother Xin Jin. The filing describes Jin as having final authority over all major financial decisions at Cere Network from its inception through the alleged scheme.

Jin also allegedly made direct misrepresentations to investors about how their capital would be deployed, the status of lockup agreements on insider tokens, and the overall financial health of the project. The complaint states that Jin personally assured investors their tokens were subject to vesting schedules while simultaneously moving insider allocations to exchanges for immediate liquidation on launch day. The complaint further alleges that Jin personally controlled the token distribution process and withheld investor allocations, even as he and other insiders moved their own tokens to exchanges within hours of the November 2021 launch.

What Bao Is Specifically Accused Of, and His Prior Legal History

Bao’s exposure comes through his position on Cere Network’s board of directors, where the complaint alleges he served as an enabler of Jin’s conduct rather than its primary architect.

Both lawsuits allege that Bao received director’s fees and early token allocations, lent his name and Lime pedigree to the project to attract investors, and approved financial transactions that moved funds into accounts controlled by Jin. The new complaint adds Section 20(a) “control person” liability, which creates a legal pathway to hold Bao responsible as someone who exercised control over an entity that violated federal securities laws. This is a more aggressive legal theory than anything in the first suit.

The Cere Network lawsuits are not Bao’s first encounter with litigation. He has previously faced a fraud action involving the City of San Francisco and a separate lawsuit brought by prominent venture firm Khosla Ventures, which alleged fraud and intentional interference in connection with a collapsed $30 million acquisition deal. The accumulation of legal exposure across multiple fronts, now including two federal RICO suits with a combined $157 million in claimed damages, represents a significant escalation for a figure whose public reputation was built on transforming urban transportation.

The Investors Who Got Nothing

Plaintiff Josef Qu invested in Cere Network through a Simple Agreement for Future Tokens in 2019, which entitled him to 27,777,778 CERE tokens. According to the complaint, Qu never received any of his tokens despite confirmed entitlement and repeated requests. The filing alleges that Jin personally controlled the token distribution process and withheld investor allocations even as he and other insiders moved their own tokens to exchanges and began liquidating within hours of the November 2021 launch.

The first lawsuit’s plaintiffs tell a similar story: Vivian Liu and Goopal Digital claim they were owed a combined 53.3 million tokens and received none. The CERE token reached $0.47 on launch day and now trades at approximately $0.00061, a decline of more than 99.8 percent. The recurring narrative of investors who were promised tokens, never received them, and watched insiders sell is central to both lawsuits’ RICO claims.

Named Defendants and Case Details

Both lawsuits name the same core defendants: Fred Jin (Cere Network CEO), Brad Bao (Lime co-founder, Cere board member), Maren Schwarzer (Jin’s wife), Xin Jin (Jin’s brother), Martijn Broersma (Cere CMO), François Granade (Cere director), and corporate entities Cerebellum Network Inc., Interdata Network Ltd., and CEF AI Inc.

The new lawsuit is Josef Qu v. Fred Jin et al., Case No. 3:26-cv-01235, with the plaintiff represented by Laith D. Mosely and Joshua C. Williams of Raines Feldman Littrell LLP. The related first lawsuit is Goopal Digital Limited et al. v. Fred Jin et al., Case No. 3:26-cv-00857, with plaintiffs represented by John K. Ly and Jennifer L. Chor of Liang Ly LLP. Both cases are pending in the U.S. District Court for the Northern District of California.

What This Means for Regulatory Scrutiny

Two federal RICO lawsuits in a matter of weeks, totaling $157 million, with securities fraud claims and documented ties to a convicted market manipulation firm. This is the kind of fact pattern that tends to attract regulatory attention.

The SEC has made token offerings a priority enforcement area, and the allegations in the Qu complaint, including material misrepresentations to SAFT investors, insider selling in violation of lockup agreements, and wash trading through a firm whose founder was convicted in a DOJ sting, fall squarely within that mandate. The DOJ’s existing familiarity with Gotbit through Operation Token Mirrors provides an established investigative thread that could be extended to examine related token launches. And the allegation that stolen funds are being deployed into a new AI venture suggests the conduct may be ongoing, which is typically the trigger that moves regulators from monitoring to action.

None of this means enforcement action is imminent or certain. But the combination of escalating civil litigation, securities fraud claims, blockchain evidence, convicted co-conspirators, and allegations of active fund recycling creates a situation where regulatory inaction would itself be notable.

What This Tells Us About Crypto’s Accountability Problem

In the first Goopal lawsuit, there is a broader point about the gap between the names on a crypto project’s leadership page and the actual oversight those individuals provide. The second lawsuit reinforces that observation and extends it.

The Cere Network case is becoming a case study in how prominent reputations from traditional tech can be leveraged to give crypto projects an appearance of credibility that may not correspond to the underlying reality. It is also becoming a case study in what happens when that gap is eventually exposed: not one lawsuit, but two; not one set of legal theories, but an expanding arsenal; not a static set of allegations, but a growing body of forensic evidence that accumulates with each new filing.

For investors evaluating early-stage crypto projects, the practical lesson has not changed since our first article: a prominent board member is not a substitute for verifiable on-chain transparency, and the presence of a well-known name is a marketing asset, not a guarantee of fiduciary oversight. What has changed is the stakes. When the same defendants face $157 million in combined federal claims from multiple independent plaintiffs, the question shifts from whether something went wrong to how far the consequences will reach.

FAQ

What is a RICO lawsuit?

RICO stands for the Racketeer Influenced and Corrupt Organizations Act, a federal law originally designed to combat organized crime. It allows plaintiffs to sue defendants who engage in a “pattern of racketeering activity,” meaning two or more related criminal acts within a ten-year period. RICO claims carry significant weight because they can result in treble damages and require the court to evaluate whether the alleged conduct reflects an ongoing enterprise rather than an isolated incident.

How is the second lawsuit different from the first?

The Qu complaint introduces federal securities fraud claims under Section 10(b) and Section 20(a) of the Securities Exchange Act, which were absent from the first lawsuit. It also adds theft as a standalone claim, brings the total causes of action to ten, cites specific blockchain forensic evidence via Etherscan, details $16.6 million in DeFi protocol losses, alleges that Jin funded a new AI venture with stolen proceeds, and requests an asset freeze covering cryptocurrency wallets, bank accounts, and real property in Germany and Florida.

Who are the defendants?

Both lawsuits name Fred Jin (Cere Network CEO), Brad Bao (Lime co-founder), Maren Schwarzer (Jin’s wife), Xin Jin (Jin’s brother), Martijn Broersma (Cere CMO), François Granade (Cere director), and corporate entities Cerebellum Network Inc., Interdata Network Ltd., and CEF AI Inc.

What is CEF AI Inc.?

According to the Qu complaint, CEF AI Inc. is a new artificial intelligence venture launched by Fred Jin that was allegedly funded with proceeds from the Cere Network fraud. The plaintiff is seeking a constructive trust over CEF AI’s assets and injunctive relief to freeze the company’s holdings.

Could this lead to SEC or DOJ action?

The allegations in both complaints, including material misrepresentations to SAFT investors, insider selling in violation of lockup agreements, wash trading through a firm whose founder was convicted in the DOJ’s Operation Token Mirrors, and securities fraud claims, fall within the SEC’s enforcement priorities around token offerings. The DOJ’s existing investigative thread through the Gotbit prosecution could also extend to related token launches. While no regulatory action has been announced, the escalating civil litigation creates the type of fact pattern that historically attracts federal scrutiny.

What should crypto investors take away from this case?

A prominent name on a project’s board or advisory team is not a substitute for verifiable transparency. Investors should insist on on-chain confirmation of vesting schedules and lockup claims, independent validation of stated partnerships and revenue, and clear governance structures that impose real accountability on board members and advisors. When multiple independent lawsuits allege the same pattern of conduct, the risk assessment should be treated as qualitatively different from a single complaint.

Disclaimer: This article is for informational and educational purposes only. The allegations described are from the complaints filed in the cases and have not been proven in court. All defendants are presumed innocent until proven guilty. Nothing in this article constitutes legal or investment advice. Readers should conduct their own research and consult with qualified professionals before making any investment decisions.