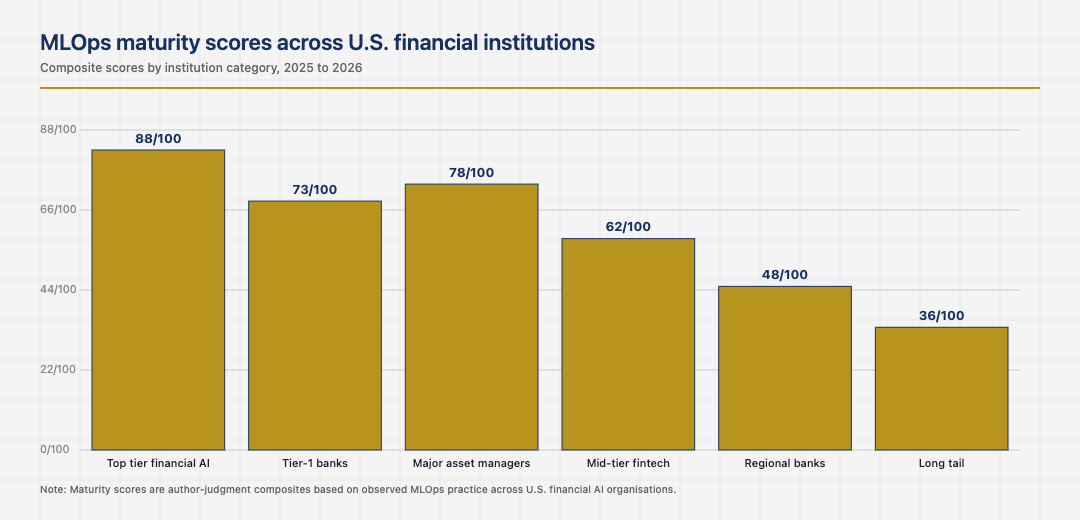

MLOps in U.S. financial services has matured significantly over the past five years. The institutions that built strong machine learning operations capabilities are deploying models faster, monitoring them more reliably, and recovering from model failures more cleanly than the institutions that have not. The differentiation now sits in the operational discipline around the lifecycle of models, not in the choice of platform or vendor.

This piece looks at where MLOps in U.S. financial services has settled in 2026, the platform decisions that have largely converged, the operational disciplines that distinguish productive programs from sprawling ones, and the supervisory environment that constrains how MLOps must work in regulated finance.

The platform layer has commoditised

The MLOps platform layer in U.S. finance has largely commoditised. The major cloud providers, the open-source ecosystem, and the specialised vendors have all converged on a recognisable stack: feature stores, model registries, training pipelines, model serving infrastructure, and monitoring layers. The choice between vendors matters less than the discipline of using whichever platform the institution has chosen consistently.

The institutions that picked a platform and standardised on it have cleaner operations than the institutions that allowed each model team to choose its own tools. The standardisation reduces operational complexity, simplifies hiring, and makes the model risk management easier. The institutions that did not standardise usually have parallel platforms with similar capabilities and unclear ownership of cross-cutting concerns like security and compliance.

Feature stores and the offline-online consistency problem

Feature stores are now standard infrastructure in mature U.S. financial MLOps deployments. The technique addresses the offline-online consistency problem: features computed for training must match the features available at inference time. The institutions that built strong feature store infrastructure produce models whose production performance matches their offline evaluation. The institutions that did not usually have a recurring class of model performance regressions traceable to feature drift between training and serving.

The operational discipline that makes feature stores work is consistent attention to feature versioning, lineage tracking, and the relationship between feature pipelines and model deployment. The institutions that treat feature engineering as a disciplined practice with the same rigour as model engineering capture the operational benefit. The institutions that treat features as code that anyone can write at any time usually have the consistency problems the feature store was supposed to solve.

Model registry and the lifecycle question

The model registry is the system of record for every model the institution operates. Mature MLOps deployments treat the registry as authoritative: every model in production has a registry entry, every registry entry has a clear ownership and lifecycle status, and the supervisory evidence about each model lives alongside the model itself. The institutions that built strong registries answer supervisory questions easily. The institutions that built weak registries usually have models in production that the registry does not know about, which is exactly the kind of finding that supervisors flag.

The discipline that makes registries work is integrating registry updates into the deployment pipeline. Models cannot reach production without a registry entry. Registry entries cannot be retired without explicit decommissioning. The institutions that built these guardrails have model inventories they can defend. The institutions that did not usually have shadow models that the registry does not capture, which complicates both operations and supervisory engagement.

Monitoring and the drift detection layer

Model monitoring in U.S. financial MLOps has evolved from periodic retraining to continuous monitoring with explicit drift detection. The institutions that built monitoring infrastructure that catches data drift, prediction drift, and performance drift in production deploy models with more confidence than the institutions that rely on scheduled re-evaluation. The discipline of continuous monitoring is now the supervisory expectation as well as the operational best practice.

The institutions that built strong monitoring respond to drift before it causes customer impact. The institutions that did not usually find out about drift through customer complaints or supervisory inquiries, both of which are more expensive than catching the drift earlier in the monitoring layer would have been. The investment in monitoring is modest. The benefit accumulates across every model the institution operates.

The next phase of MLOps in U.S. financial services

The next phase is shaped by the integration of large language model operations with traditional MLOps platforms, the maturation of vector storage and retrieval infrastructure, and the continuing tightening of supervisory expectations around model deployment. The institutions that built strong MLOps foundations in feature stores, registries, and monitoring will absorb the changes cleanly. The institutions that have not will continue to face the choice between deferring AI deployment and building operational infrastructure under regulatory pressure.

Read across the full picture, MLOps in U.S. financial services in 2026 is a settled discipline with specific patterns: standardised platform choice, strong feature store infrastructure, authoritative model registry, continuous monitoring with drift detection. The institutions that respect them deploy models reliably and pass exams cleanly. The institutions that miss any one usually have either model deployment delays or supervisory findings that the missing discipline would have prevented.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.