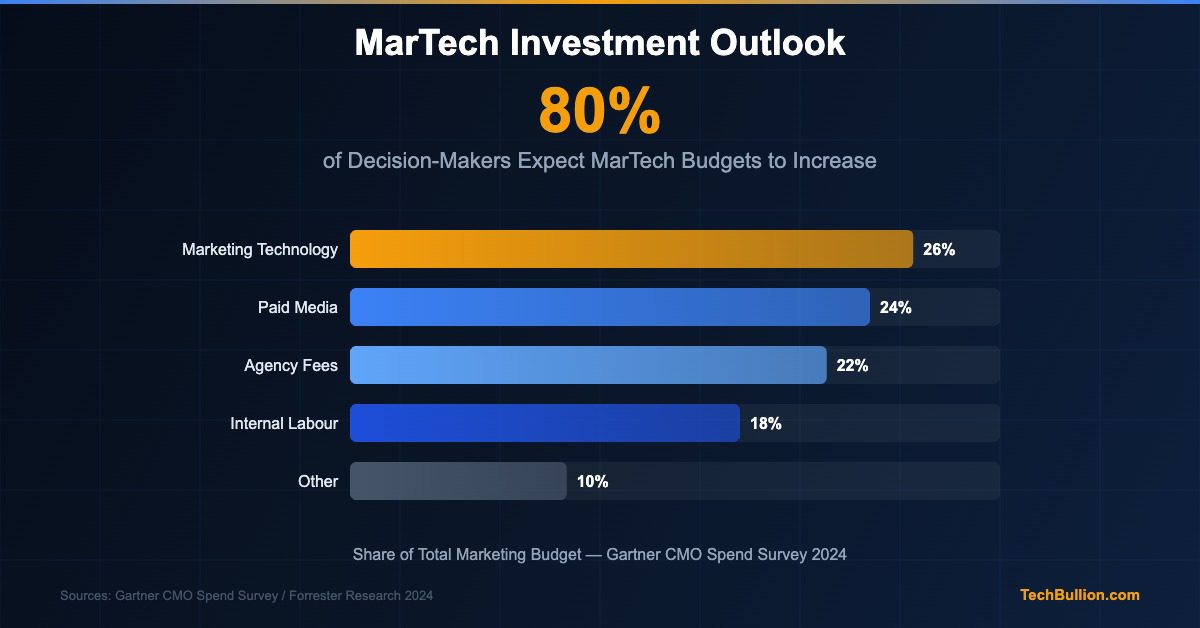

Marketing technology has become the single largest line item in many marketing budgets, and the trajectory of that investment shows no sign of reversing. According to Gartner’s annual CMO Spend Survey, marketing technology accounted for approximately 26 percent of total marketing budget allocation in 2024, ahead of paid media, agency fees, and internal labour costs. Across the broader market, approximately 80 percent of marketing technology decision-makers expect their budgets to increase over the next three to five years — a figure consistent with the broader momentum driving the $589 billion global MarTech market towards its projected $1.27 trillion valuation by 2031.

The Scale of Current MarTech Spending

The global scale of MarTech investment is significant. Research from Forrester indicates that enterprise organisations with revenues above $1 billion spend an average of 3 to 5 percent of total revenue on marketing technology, with the largest enterprises in sectors including financial services, retail, and technology exceeding this range. For a Fortune 500 company with $10 billion in revenue, that represents $300 to $500 million in annual MarTech expenditure. The diversity of organisations investing in MarTech reflects the universality of the digital marketing challenge — whether running B2B lead generation, B2C e-commerce, or subscription-based services, the need for platforms that manage customer data, automate campaign execution, and measure performance is common across sectors and geographies.

Why Budgets Keep Expanding

Several structural factors explain why MarTech budgets continue to grow year on year, even in periods of broader economic caution. The first is the competitive dynamic in digital marketing. When industry leaders invest in sophisticated MarTech capabilities — advanced personalisation, real-time data activation, AI-driven campaign optimisation — they create performance advantages that competitors must match to remain viable. This competitive pressure drives industry-wide budget escalation.

The second factor is the expanding scope of what MarTech covers. The 15,000-tool MarTech ecosystem continues to grow, with new categories emerging as digital marketing channels proliferate. The third factor is the deprecation of third-party data infrastructure. As documented in the analysis of Customer Data Platforms, the removal of cookie-based tracking from major browsers has forced organisations to build first-party data infrastructure at scale — an investment that flows directly into MarTech budgets.

The ROI Calculation Driving Continued Investment

Marketing technology investment is driven by measurable returns. McKinsey research published in 2024 found that companies in the top quartile of marketing technology adoption achieve customer acquisition costs 20 to 30 percent below industry median and customer lifetime value 15 to 25 percent above median. The ROI from marketing automation alone is well documented — Nucleus Research estimates it delivers an average return of $5.44 for every dollar invested. For CRM technology, Salesforce’s research indicates companies using its platform report an average 37 percent increase in revenue and 45 percent improvement in customer satisfaction.

Investment Patterns Across Company Size and Sector

Enterprise organisations tend to invest in complex, integrated stacks built around a small number of core platforms — typically a major CRM, a marketing automation suite, an analytics platform, and increasingly a CDP. SMBs increasingly invest in all-in-one platforms — HubSpot, Zoho, Klaviyo — that provide a range of capabilities within a single subscription. Sector differences are also significant: retail and e-commerce companies invest heavily in personalisation technology, financial services firms invest in compliance-safe automation, and technology companies typically invest earlier in data infrastructure and analytics tooling.

The Geographic Dimension

North America accounts for 35.8 percent of global MarTech market share, reflecting the depth of marketing technology investment in the United States and Canada. Europe is the second-largest investment region, with GDPR compliance requirements simultaneously increasing cost and driving investment in first-party data infrastructure. Asia Pacific is growing fastest, with the 19.9 percent compound annual growth rate for the overall market partly reflecting this geographic expansion.

Looking Ahead

The outlook for MarTech through 2034 points to continued strong investment growth. The convergence of artificial intelligence with marketing technology is creating entirely new categories of spend, as organisations invest in AI-driven content generation, predictive analytics, and real-time personalisation capabilities. The AI-driven transformation of MarTech is expected to be one of the primary budget drivers over the next decade. For CFOs and CMOs evaluating their strategy, the data is consistent: the 80 percent of decision-makers expecting budget growth are responding rationally to a market where returns from well-deployed marketing technology are measurable and the competitive pressure to invest is real.

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.

Industry Adoption and Implementation Trends

Adoption patterns across industries reveal significant variation in implementation maturity and strategic priorities. Financial services and healthcare organizations have led enterprise adoption, driven by regulatory requirements and the potential for operational efficiency gains. According to Deloitte’s industry outlook, more than 60 percent of large enterprises now allocate dedicated budgets to digital transformation initiatives, up from 35 percent in 2020. Mid-market companies have followed, though their implementations tend to focus on specific pain points rather than comprehensive overhauls.

For more coverage on related topics, explore our dedicated section on technology insights.

Risk Factors and Strategic Considerations

Several factors could moderate the growth trajectory that current projections suggest. Macroeconomic uncertainty, including persistent inflation in key markets and tightening credit conditions, may constrain capital expenditure budgets in the near term. Regulatory fragmentation across jurisdictions creates compliance costs that disproportionately affect smaller operators. Talent shortages in specialized technical roles remain a bottleneck, with demand for qualified professionals exceeding supply by an estimated two-to-one ratio in most developed markets according to PwC’s workforce analysis. Organizations that address these constraints proactively will be better positioned to capture market share.

Industry Adoption and Implementation Trends

Adoption patterns across industries reveal significant variation in implementation maturity and strategic priorities. Financial services and healthcare organizations have led enterprise adoption, driven by regulatory requirements and the potential for operational efficiency gains. According to Deloitte’s industry outlook, more than 60 percent of large enterprises now allocate dedicated budgets to digital transformation initiatives, up from 35 percent in 2020. Mid-market companies have followed, though their implementations tend to focus on specific pain points rather than comprehensive overhauls.

Readers interested in this space may also find value in our reporting on AI-powered marketing.