A Structural Shift in Financial Services Revenue

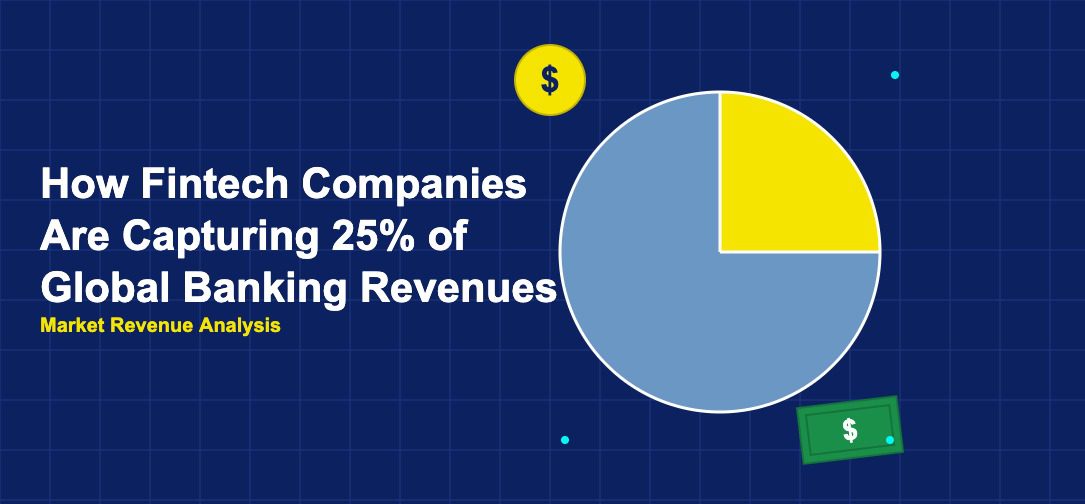

The migration of banking revenue from traditional institutions to fintech platforms has moved beyond the early disruption phase into a structural realignment of the financial services industry. Industry; Company and other leading consultancies estimates that fintech companies now capture approximately 25% of global banking revenues, a share that has grown steadily over the past decade and shows no signs of plateauing. This represents hundreds of billions of dollars in annual revenue that has shifted from incumbent banks to technology-driven competitors.

The revenue capture is not evenly distributed across banking activities. Fintech companies have made the deepest inroads in payments, consumer lending, and wealth management, while corporate banking and complex capital markets activities remain more firmly held by traditional institutions. Understanding where fintech has gained revenue share, and why, reveals the competitive dynamics reshaping global banking.

Payments Revenue Under Pressure

Payments represent the banking activity where fintech has captured the most revenue. Traditional banks have long relied on interchange fees, foreign exchange spreads, and transaction processing charges as reliable revenue streams. Fintech companies have systematically attacked each of these revenue pools by offering cheaper, faster, and more transparent alternatives.

The Boston Consulting Group projects fintech revenues will reach $1.5 trillion by 2030, with embedded finance and digital lending accounting for the largest share of projected growth.

According to CB Insights’ 2024 fintech report, global fintech funding declined 40 percent between 2022 and 2024, pushing the sector toward consolidation and a sharper focus on profitability over growth at all costs.

In domestic payments, companies like Square, Stripe, and PayPal have captured significant merchant acquiring revenue by offering simpler onboarding, better technology integration, and more competitive pricing than traditional merchant services providers. In international payments, platforms like Wise have compressed the foreign exchange margins that banks traditionally charged, offering exchange rates close to the mid-market rate and transparent fee structures that expose the hidden costs of traditional bank transfers.

The rise of real-time payment systems, many of them government-led initiatives like India&’s UPI and Brazil&’s Pix, has further reduced the revenue banks extract from payments by providing free or low-cost payment rails that bypass traditional bank-controlled infrastructure.

Consumer Lending Disrupted by Digital Platforms

Consumer lending, one of the most profitable activities for retail banks, has seen substantial revenue migration to fintech platforms. Digital lenders have captured market share across personal loans, point-of-sale financing, student loan refinancing, and small-dollar credit products. Their advantage stems from lower operating costs, faster approval processes, and the ability to reach customers through digital channels rather than branch networks.

Buy-now-pay-later platforms like Klarna, Affirm, and Afterpay have been particularly effective at capturing lending revenue that previously flowed to credit card issuers. By offering interest-free installment plans at the point of sale, these platforms attract consumers who might otherwise have used credit cards, diverting interchange and interest revenue away from traditional card issuers.

have captured a meaningful share of new consumer loan origination in several major markets, with the share continuing to grow as borrower comfort with digital lending increases and traditional banks struggle to match the speed and convenience of fintech alternatives.

Wealth Management Fees Under Competitive Pressure

Traditional wealth management has relied on advisory fees and management charges that typically range from 0.75% to 1.5% of assets under management annually. Robo-advisory platforms from companies like Betterment, Wealthfront, and Nutmeg have offered comparable portfolio management services for fees of 0.25% to 0.50%, forcing traditional wealth managers to justify their pricing or reduce their fees.

Trading platforms like Robinhood disrupted brokerage revenue by introducing commission-free stock trading, a model that most major brokerages subsequently adopted. While Robinhood generates revenue through other mechanisms including payment for order flow and premium subscriptions, the impact on industry pricing was significant. Billions of dollars in annual commission revenue evaporated across the brokerage industry within a few years of commission-free trading becoming mainstream.

Small Business Banking Revenue Shifting

Small and medium-sized business banking represents another area where fintech companies have gained significant ground. Traditional banks have historically found it difficult to serve small businesses profitably, leading to high fees, rigid product offerings, and poor digital experiences. Fintech companies have stepped into this gap with digital business accounts, automated bookkeeping tools, integrated payment solutions, and fast-approval business loans.

Companies like Mercury, Brex, and Ramp in the United States, Tide and Starling in the United Kingdom, and various regional players in other markets have attracted millions of small business customers. These platforms typically generate revenue through interchange on business card spending, fees on financial products, and subscription charges for premium features. Each dollar of revenue they generate from small business customers represents revenue that incumbent banks are not collecting.

Why Traditional Banks Are Losing Revenue Share

Several structural factors explain why fintech companies have been able to capture banking revenue so effectively. First, fintech companies operate with fundamentally lower cost structures. They do not maintain branch networks, they employ fewer people per customer served, and their technology platforms are designed for efficiency rather than retrofitted onto legacy systems.

Second, fintech companies have generally offered better customer experiences. Mobile-first design, instant onboarding, transparent pricing, and responsive customer service have set new expectations that traditional banks struggle to match with their older technology infrastructure and organizational structures.

Third, fintech companies have been faster to innovate. The product development cycles at most fintech companies are measured in weeks, while traditional banks often require months or years to launch new products due to legacy technology constraints and complex internal approval processes.

How Banks Are Responding

Traditional banks are not passive observers of this revenue migration. Many have invested billions of dollars in digital transformation programs aimed at modernizing their technology, improving customer experiences, and launching competitive digital products. Some have acquired fintech companies outright, bringing their technology and talent in-house. Others have formed partnerships, using fintech infrastructure to enhance their own offerings.

Several large banks have launched their own digital-only banking brands, creating separate entities that can operate with fintech-like speed and culture while drawing on the parent bank&’s balance sheet and regulatory licenses. JPMorgan Chase&’s digital capabilities, Goldman Sachs&’ Marcus platform, and similar initiatives from major banks around the world represent significant competitive responses to fintech disruption.

The Revenue Share Outlook

Most industry analysts expect fintech&’s share of banking revenue to continue growing, though the pace of growth may vary by segment and geography. Areas where fintech penetration is already high, like payments and consumer lending in developed markets, may see slower incremental growth. Areas where digitization is still in early stages, like insurance, corporate banking, and financial services in many emerging markets, offer more room for continued revenue capture.

The long-term equilibrium between fintech companies and traditional banks is likely to be more collaborative than purely competitive. Many fintech companies depend on banking infrastructure, licenses, and balance sheets to operate. Many banks find that partnering with fintech companies produces better outcomes than trying to build competitive products internally. The 25% revenue share figure represents a snapshot of an ongoing transformation that will continue reshaping the industry for years to come.