Consensus mechanisms used to be a topic that lived in computer science papers and crypto Twitter threads. In 2026 they have become a U.S. policy and infrastructure issue, debated openly at SEC roundtables, at Federal Reserve research conferences, and inside the technology teams of every major American bank that has begun running tokenized assets in production. The reason is simple. Consensus is what makes a public ledger trustworthy without a central operator, and the U.S. financial system now has billions of dollars of regulated activity sitting on rails that rely on it.

This piece looks at where U.S.-relevant consensus design has actually arrived, what the practical trade-offs look like for builders and operators on American soil, and which signals from regulators, exchanges and institutional issuers are worth tracking through 2027.

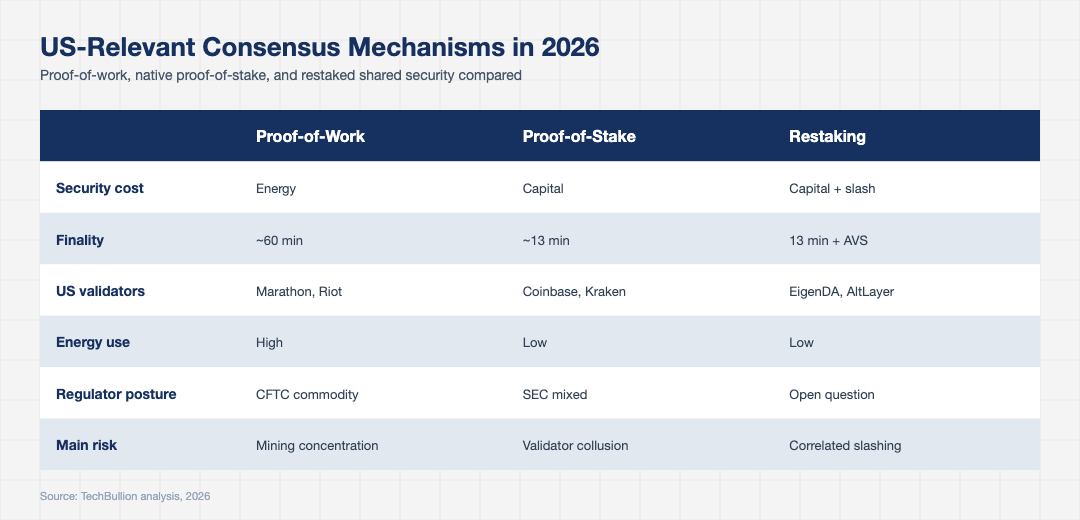

What consensus means in 2026, in plain terms

A consensus mechanism is the rule that lets thousands of computers, run by people who do not trust each other, agree on the order of transactions. In a banking system, the bank’s database is the source of truth. In a public blockchain, no single party is in charge, so the network needs a mechanical way to decide what counts as the official record. Two designs dominate the U.S.-relevant market: proof-of-work, used by Bitcoin, and proof-of-stake, used by Ethereum, Solana, Avalanche, the Cosmos chains, and most of the newer high-throughput networks.

The shorthand is that proof-of-work spends energy to secure the ledger, while proof-of-stake spends capital. Validators in proof-of-stake post a bond in the native token of the network, vote on which blocks are valid, and lose part of their bond if they misbehave. That single shift, from energy to capital, has changed everything from network economics to the way U.S. courts have begun to characterize validator income. The IRS treats staking rewards as taxable income at receipt, a position confirmed by Revenue Ruling 2023-14 and reinforced by the Service in 2024 guidance.

The slow migration from proof-of-work to proof-of-stake

Ethereum’s 2022 Merge was the watershed moment. The network’s switch from proof-of-work to proof-of-stake cut energy use by roughly 99.95% according to the Crypto Carbon Ratings Institute, and ended the industrial mining footprint that had concentrated in Pennsylvania, Texas and Washington State. The aftershocks of that decision are still being absorbed by the U.S. operating environment. Mining companies pivoted to AI compute, hosting deals with hyperscalers, or wound down. By the end of 2025 the only U.S.-listed pure-play Bitcoin miners with meaningful market caps were Marathon, Riot, CleanSpark and a handful of smaller names.

On the proof-of-stake side, the picture is denser. Coinbase, Kraken and Figment together account for a meaningful share of Ethereum staking from U.S. accounts. Lido is the largest pool overall but has actively reduced its U.S. exposure since the SEC’s 2023 actions on staking-as-a-service. The result is a more fragmented, more compliance-driven validator footprint in which U.S. participants increasingly run their own infrastructure rather than relying on offshore pools.

For institutional issuers, this matters. When BlackRock’s BUIDL fund, Franklin Templeton’s BENJI and Hamilton Lane’s tokenized vehicles chose Ethereum and Polygon as host networks, they were implicitly choosing proof-of-stake security. Their custodians, BNY Mellon and State Street among them, have spent the past two years writing internal frameworks for what they will and will not delegate, and to which validators.

Restaking and shared security are the new design pattern

The most active design conversation inside U.S. blockchain engineering teams in 2026 is not whether to use proof-of-stake. That is settled. The conversation is about restaking. Restaking lets a validator’s bond do double duty by securing not only the base chain but also additional services that opt into using that bond as collateral.

EigenLayer, founded in Seattle, is the protocol most associated with this idea, but it is no longer alone. Symbiotic, Karak and several quieter alternatives now run production deployments. The application surface that uses them includes data availability layers, oracle networks, bridges, sequencer protocols for rollups, and a growing list of permissioned services. The U.S. relevance is significant because many of the largest users of these services, including Coinbase’s Base rollup and a number of institutional bridges, are anchored on American legal entities even when their tokens are global.

The trade-off the industry is still figuring out is risk correlation. If a single validator’s bond is securing fifteen services simultaneously, a fault in one service can cascade into the others. Vitalik Buterin’s well-circulated 2024 essay on the topic argued that some restaking use cases extend the social consensus of the base chain too far. American regulators have not weighed in directly, but the OCC’s 2024 guidance on bank participation in distributed ledger arrangements made clear that any bank running a validator on a restaked chain will need to document the risk of correlated slashing.

Where US regulators have actually landed

The U.S. regulatory position on consensus mechanisms in 2026 is best described as functional rather than ideological. The SEC, after losing several elements of its 2023 enforcement campaign in court, has narrowed its claims and now focuses on staking-as-a-service offerings that combine pooled investor funds with promotional language about expected returns. Direct, self-custodied validation by an individual or institution is not, in current SEC practice, a securities offering.

The CFTC has staked out jurisdiction over the largest proof-of-work and proof-of-stake assets as commodities, a position effectively codified by the December 2024 settlement framework with two major U.S. exchanges. Treasury’s FinCEN is meanwhile focused on the wallet and intermediary layer rather than the consensus protocol itself, which has given validator operators a relatively clear lane to plan against.

The clearer policy area is taxation. The IRS now treats validator rewards as ordinary income at fair market value on receipt, and the 2024 broker reporting regulations require certain U.S. intermediaries to report digital asset transactions on Form 1099-DA beginning with the 2025 tax year. For a U.S. company that runs proof-of-stake nodes as a business, this means routine accounting workflows now look much closer to those of a regulated financial entity than to those of an unregulated software company.

What the next 24 months hold for US consensus design

Three forces will shape the U.S. picture through 2027. The first is institutional staking. BlackRock and Fidelity have both filed for spot Ethereum ETFs that include staking yield. Approval would push validator selection and slashing risk into mainstream asset manager workflows, with all the operational rigor that implies. The second is the rise of application-specific chains, often called appchains, where a small set of validators serves a single business use case rather than a public market. U.S. payment networks, supply chain consortia and tokenized fund administrators are the loudest current users of this pattern.

The third force is the slow but real pressure for verifiability. Zero-knowledge proofs let one party convince another that a computation was done correctly without revealing the inputs. Several U.S. teams have begun integrating ZK-based finality proofs into proof-of-stake rollups, which shortens the trust assumptions a U.S. participant has to make. The combination of staked capital and ZK proofs is increasingly seen as the long-run answer to skepticism that public chains can host regulated financial activity at scale.

That tightening relationship between regulators and consensus engineers also matters for end-users. The reliability of a public chain depends not on a single operator but on the discipline of dozens of independent teams who all believe the rules will be enforced. When validator economics, tax treatment and slashing rules are clear, that discipline holds. When any of those layers is ambiguous, the network has historically drifted toward either centralization or risk. The U.S. environment in 2026 is, for the first time, mostly unambiguous on the legal points that matter most for honest operators.

For builders, operators and policy teams in the United States, the practical takeaway in 2026 is that consensus design is no longer the abstract layer it was. It is a set of operational, legal and risk decisions that increasingly look like the decisions a clearinghouse, a custodian or a payment network would make. The technology has moved closer to the regulated financial system, and the regulated financial system, hesitantly, is moving closer to it.