For four decades, a comfortable assumption sat beneath much of professional investing: buy a reasonable asset, apply leverage, ride multiple expansion, and wealth follows. Falling interest rates did a great deal of the work, and financial engineering did much of the rest.

That era has ended, and the data now shows it plainly. Across private equity, venture capital, search funds and family office portfolios, the returns increasingly accrue to investors and operators who build value inside businesses rather than those who simply transact around them. McKinsey’s most recent Global Private Markets Report puts it bluntly: the conditions that once amplified returns, declining rates, expanding multiples and abundant leverage, have passed, and alpha “will be made” rather than found.

This article sets out the evidence: what the numbers say about where returns actually come from, which investment models prove the point most decisively, and what it means for anyone allocating capital, or seeking it, in the decade ahead.

The end of the free ride: what drove private equity returns until now

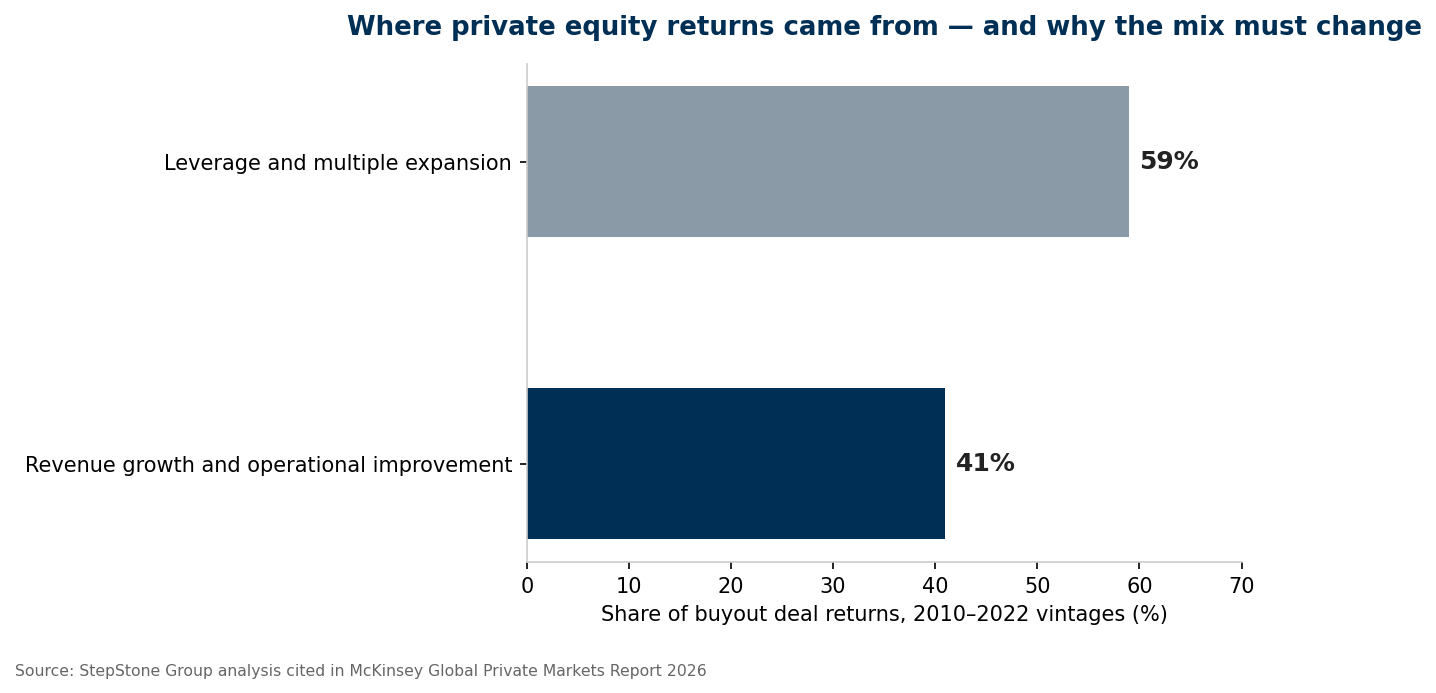

The most important dataset in this debate comes from StepStone Group, cited in McKinsey’s Global Private Markets Report 2026. For buyout deals completed between 2010 and 2022, leverage and multiple expansion accounted for 59% of returns. Barely two-fifths of the wealth generated in private equity’s golden decade came from making companies genuinely better, growing revenue, widening margins, improving operations.

That mix was rational while it lasted. Cheap debt magnified equity returns, and a rising tide of valuation multiples meant a business bought at eight times earnings could be sold at eleven without changing much at all. But neither lever is reliably available any more. Borrowing costs remain structurally higher than the 2010s, and entry multiples across most sectors leave little room for further expansion.

The consequences are already visible in the holding data. According to McKinsey, more than 16,000 portfolio companies globally have now been held for over four years, 52% of total buyout-backed inventory, the highest level on record, and the typical company in a general partner’s portfolio is held for more than six and a half years. Assets bought on the assumption of a quick re-rating are waiting for value that was never built.

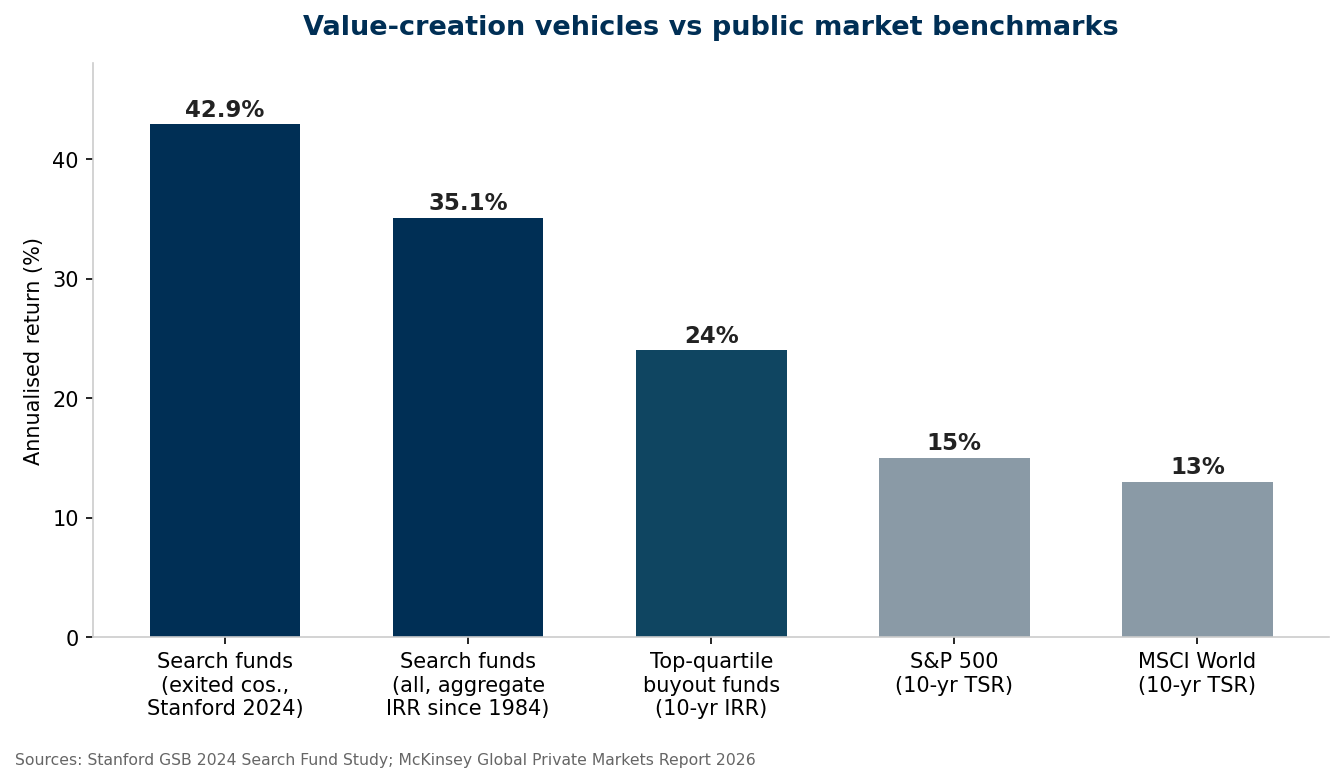

Yet the industry itself is far from shrinking. Private equity deal value rose 19% in 2025 to $2.6 trillion, and exit value climbed 41% to $1.3 trillion, the second-highest year on record. Capital is flowing, but it is flowing towards a different skill set. Over the past decade, top-quartile buyout funds have generated internal rates of return of roughly 24%, against a 15% total shareholder return for the S&P 500. The dispersion between top-quartile and median managers is widening, and the differentiator, fund after fund, is operational value creation: pricing, procurement, sales effectiveness, technology adoption and management upgrades, applied early and consistently in the hold period.

For limited partners, the practical lesson is that manager selection now matters more than asset-class selection. The question to ask any general partner is no longer “what can you buy?” but “what can you build, and can you prove you have done it before without leverage doing the work?”

The purest natural experiment: search fund returns

If private equity offers circumstantial evidence that value creation drives wealth, search funds offer something closer to a controlled experiment. The model strips out almost everything except operating skill: a single entrepreneur raises modest capital, acquires one established small business, typically profitable, unglamorous and founder-owned, and then runs it personally for five to seven years. There is no portfolio effect, limited financial engineering and no brand halo. Returns depend almost entirely on whether the operator makes the business better.

The results are remarkable. Stanford Graduate School of Business, which has tracked the asset class since 1984, reported in its 2024 Search Fund Study, covering 681 first-time funds in the United States and Canada, an aggregate pre-tax internal rate of return of 35.1% and a return on invested capital of 4.5 times. For companies that have completed a full cycle and exited, the IRR rises to 42.9% . Roughly 70% of acquired companies generate positive returns for their investors, with the most common outcome falling in the two-to-five-times range.

Set those figures against any mainstream benchmark and the gap is striking. These are small businesses, the median purchase price in the latest study was $14.4 million, bought at modest multiples and grown through unglamorous operational work: professionalising finance functions, building sales teams, modernising systems. The wealth is created, not captured.

Investors have noticed. A record 94 traditional search funds launched in 2023 alone, and the model is spreading rapidly beyond North America. For family offices and high-net-worth investors in particular, search funds have become a way to back operators directly, at the point where capital and competence meet, which is precisely where the data says returns now live.

Venture capital: the same law at greater extremes

Venture capital has always been the asset class most honest about this principle, because the power law leaves nowhere to hide. A venture fund cannot financially engineer its way to a 10x outcome; it can only back, and help build, companies that create extraordinary value.

The current cycle illustrates how violently capital concentrates around perceived value creation. Global venture funding reached $97 billion in the third quarter of 2025, up 38% year on year, according to Crunchbase data, with quarterly totals above $90 billion for four consecutive quarters. Yet roughly a third of all investment in that quarter went to just 18 companies raising rounds of $500 million or more, and around 46% of global venture dollars flowed to artificial intelligence companies alone.

One can debate whether the AI cohort will justify those valuations. What is not debatable is the underlying logic of allocation: investors are paying enormous premiums for businesses they believe are creating step-change value, new capabilities, new productivity, new markets, and starving everything that merely participates in a sector. In a world where capital is abundant but conviction is scarce, demonstrated value creation is the only currency that clears.

For founders, the implication is uncomfortable but clarifying. The fundraising market no longer rewards presence; it rewards proof. Revenue quality, retention, unit economics and genuine technical differentiation, the measurable artefacts of value creation, determine access to capital far more than narrative does.

Family offices: how the most patient capital votes

Family offices manage wealth that has already been created, usually through the founding and building of an operating business. How they allocate it is therefore a useful signal of what experienced wealth creators believe about where returns come from.

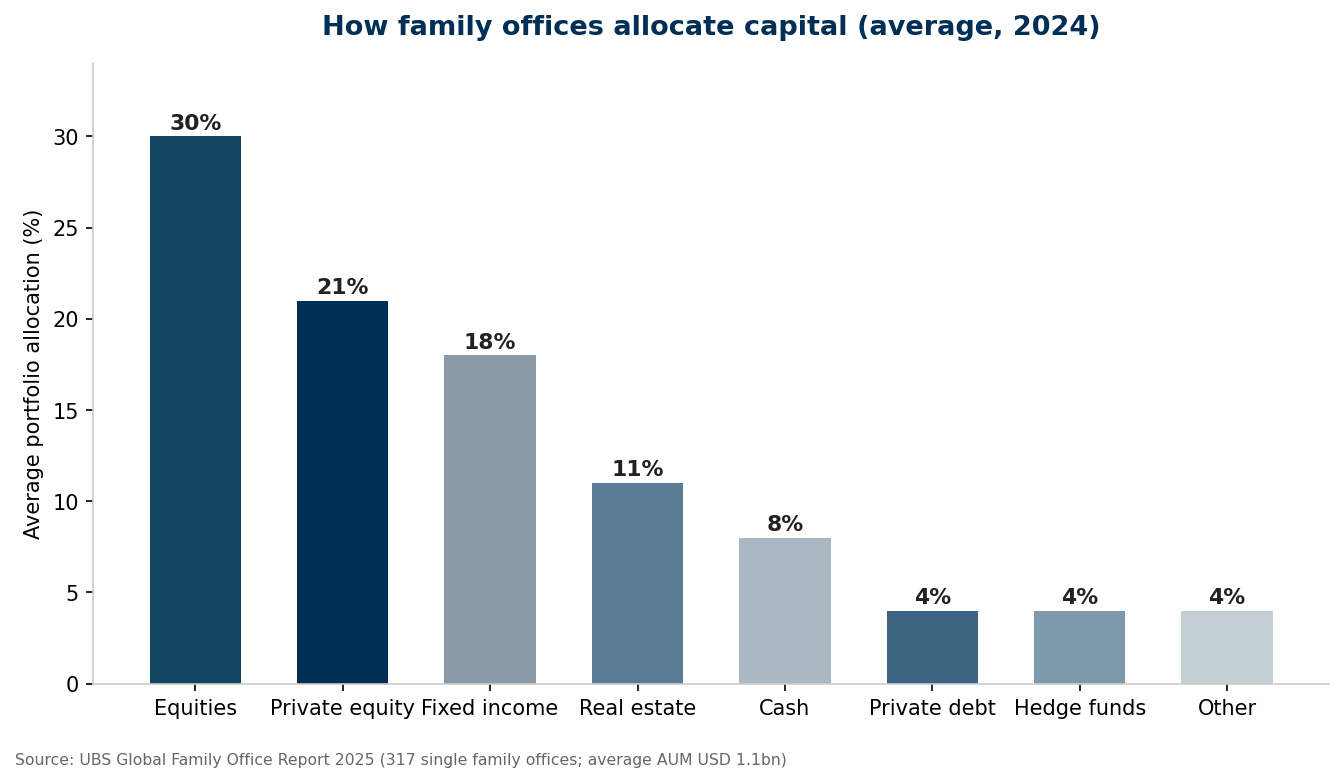

The UBS Global Family Office Report 2025, surveying 317 single family offices with an average of $1.1 billion under management and average family net worth of $2.7 billion, found alternatives comprising 44% of the average portfolio, with private equity the largest single alternative allocation at 21%. Direct investments make up more than 40% of those private equity allocations: families choosing specific operating businesses, often in industries they know intimately, rather than simply buying diversified exposure.

The report also records a tactical pause: average private equity allocations slipped from 22 to 21%, reflecting subdued exits and higher financing costs across the industry. But the long-term intent is unambiguous, a third or more of family offices expect to increase private equity exposure, both direct and fund-based, over the next five years, alongside notable interest in backing emerging managers.

Read together, the family office data describes a sophisticated investor base doing exactly what the returns evidence recommends: holding meaningful exposure to ownership of productive businesses, prioritising direct relationships with operators, and treating illiquidity not as a cost but as the price of access to genuine value creation.

The value creation playbook: what the evidence rewards

Across all four investor classes, the same handful of capabilities separate the wealth creators from the rest. The research points to five.

First, buy or build below intrinsic value, then earn the rest. Search funds work partly because small, founder-owned businesses trade at modest multiples; the discipline at entry creates the headroom for operational gains to compound.

Second, treat operations as the primary return lever, not the residual one. McKinsey’s analysis of top-performing funds consistently shows operational improvement supplying the majority of value in the best deals, pricing, procurement, go-to-market and technology, pursued from day one rather than year three.

Third, hold long enough for compounding to work. The family office preference for long-duration ownership is not sentimentality; it is arithmetic. Operational improvements compound, whereas multiple arbitrage is a one-off.

Fourth, back people over structures. Stanford’s data shows search fund returns hinge overwhelmingly on operator quality, and venture capital’s power law is, at root, a power law of founding teams. Capital allocation is increasingly talent allocation.

Fifth, build proprietary access. Whether it is a sponsor’s deal network, a family office’s industry relationships or a founder’s distribution advantage, the entities that see opportunities before they are auctioned consistently pay less for more value.

The conclusion the data forces

Strip away the asset-class labels and a single pattern remains. The 59% of historical private equity returns supplied by leverage and multiples is not coming back. The 35% IRRs of search funds, the concentration of venture capital into genuine builders, and the deliberate, ownership-heavy allocations of the world’s wealthiest families all point the same way.

Wealth is downstream of value. It always was, the past decade’s cheap money simply obscured the relationship. As that distortion unwinds, capital is reorganising itself around the people and institutions who can demonstrably make businesses worth more: better run, faster growing, more durable. For investors, that means selecting for operating capability with the same rigour once reserved for financial structuring. For founders and operators, it means the most reliable path to attracting capital has become refreshingly old-fashioned: create value first, and the wealth, and the investors, will follow.

Questions Worth Asking

What does “value creation” actually mean in investing?

Value creation refers to increasing the intrinsic worth of a business through real improvement, revenue growth, margin expansion, operational efficiency and stronger management, rather than through financial engineering such as leverage or buying at one multiple and selling at a higher one. The StepStone analysis cited by McKinsey shows the financial-engineering share of private equity returns (59% for 2010–2022 deals) is structurally declining.

Why do search funds deliver such high returns?

Stanford GSB’s 2024 study attributes the asset class’s 35.1% aggregate IRR to a combination of low entry multiples on small, profitable businesses and intensive hands-on operating improvement by a dedicated entrepreneur-CEO. Returns are driven almost entirely by making the acquired company better, which is why operator quality is the strongest predictor of outcomes.

Are family offices reducing their private markets exposure?

Only tactically. UBS’s 2025 report shows average private equity allocations easing from 22 to 21% amid a slow exit environment, but a third or more of family offices intend to increase private equity exposure over the next five years, and direct investments remain over 40% of their private equity holdings.

What should founders take from this evidence? That capital now follows proof of value creation rather than narrative. Demonstrable unit economics, retention, operational discipline and a credible plan to compound intrinsic value are the strongest fundraising assets a founder can hold, across venture capital, private equity and family office capital alike.