A decade ago a US bank mobile app was a thin window onto the bank’s existing systems. Open it, see a balance, transfer between two accounts, log out. Today, the same app is the primary product channel for the majority of US bank customers, the most measured surface area in the company, and the place where most of the engineering investment now lands. Mobile banking app development has moved from an interface problem to the central discipline inside US bank technology.

What Mobile Banking App Development Now Covers

Inside a typical US bank, mobile banking app development covers far more than the screen. The discipline spans native iOS and Android engineering, cross platform frameworks where they are used, the real-time-transactions/”>API layer behind the app, the authentication and identity flow that lets a user in, the push notification infrastructure that brings users back, the analytics pipeline that measures behaviour, and the experimentation platform that allows teams to ship variants safely.

The teams that own these layers used to be scattered across the bank. Today, at every large US institution, mobile app development is run as a unified product engineering organization, with senior leaders who report directly to the head of consumer banking or the chief technology officer. The reorganization happened because mobile is no longer a feature. It is the bank’s primary distribution channel.

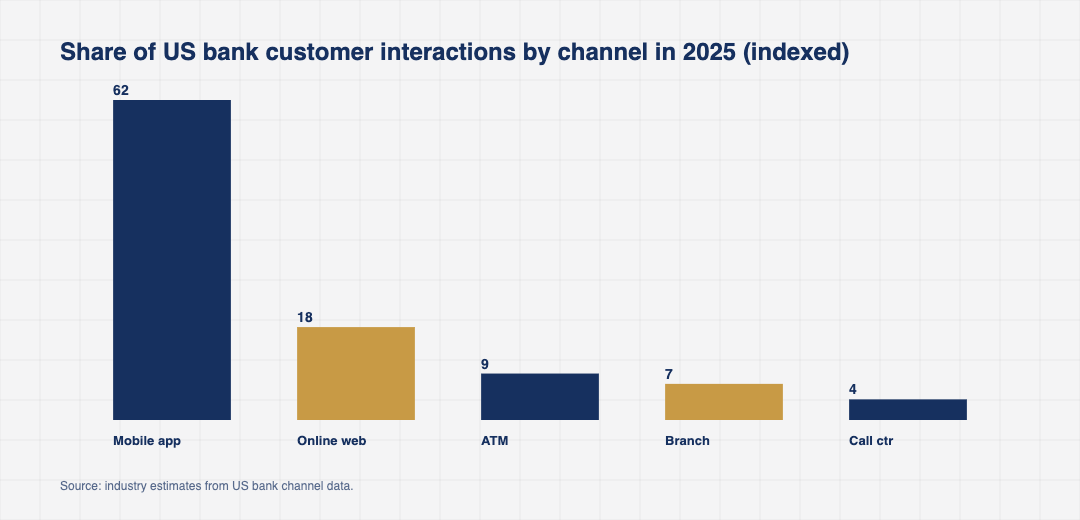

The FDIC’s 2023 National Survey of Unbanked and Underbanked Households confirms the shift. Mobile banking was the primary access method for 48.3% of banked households in 2023, the largest single share since the agency began tracking the channel, ahead of online banking, ATMs, and bank branches. The mobile share rises sharply in younger age cohorts.

The Workloads Where Mobile Investment Now Concentrates

Three areas inside the US mobile banking estate absorb most of the investment.

The first is onboarding. The flow that turns a downloaded app into a funded account, with identity verification, account opening, debit card issuance, and initial funding, is the most measured surface in the app. A one percent improvement in completion rate at a large US bank translates to thousands of additional funded accounts per month.

The second is payments. P2P transfers through Zelle, real time payments through RTP and FedNow, bill pay, card controls, and tap to pay are core mobile experiences. The competitive bar has been set by Cash App, Venmo, and the neobanks, and incumbent US banks have invested heavily to keep parity.

The third is intelligence. Spend tracking, cash flow forecasting, savings nudges, fraud alerts, and personalized offers all run on the mobile surface, and most of them depend on machine learning models that need to be trained, monitored, and retrained in production.

A fourth area, customer support inside the app, has expanded significantly. In app chat, callback scheduling, and AI assisted triage handle a meaningful share of total US bank service contacts. The result has been lower contact center load and faster customer resolution for issues that used to require a phone call.

How Mobile Banking App Development Stacks Against Other Channels

The shift in channel mix is well documented and continuing.

The mobile app handles the everyday interactions. The branch handles the high friction or high consequence events, including mortgage closings, business account opening, and certain types of dispute resolution. The website still carries a meaningful share, particularly for older customers and complex transactions, but its share has been declining year on year.

The ATM remains important for cash, although the cash share of total US consumer payments is structurally declining and the ATM network is being optimized accordingly. The call center handles the cases that the app cannot, and is increasingly the channel where US banks invest in voice AI to handle routine inquiries.

The Friction Points US Mobile Banking Teams Manage

Four frictions come up repeatedly inside US bank mobile organizations.

The first is the platform fragmentation cost. Native iOS and Android development requires two codebases, two release pipelines, and two sets of engineers. Cross platform frameworks like React Native and Flutter have made meaningful inroads, but the largest US banks still invest in native development for the customer facing path because the experience and performance gap is real.

The second is app store dependence. Apple and Google control distribution, review timelines, and platform rules. A US bank that needs to ship a critical fix on a Friday afternoon is at the mercy of the app store review queue. Banks have responded with feature flags, remote configuration, and over the air content updates, but the fundamental dependency remains.

The third is security. The mobile app is the primary attack surface for account takeover, social engineering, and mobile malware. US banks invest heavily in device attestation, behavioural biometrics, jailbreak and root detection, and runtime application self protection. The cost shows up clearly in the security operations budget.

The fourth is accessibility. US banks are subject to ADA expectations and to a growing set of state and federal accessibility requirements. Building and maintaining an accessible mobile experience across two platforms is real engineering work, and the standards continue to rise.

A fifth and increasingly visible friction is the engineering productivity curve. As mobile codebases at large US banks have grown past a million lines, build times, test runtimes, and release pipeline duration have all become real concerns. The investment in build infrastructure, modularization, and code health is now a permanent line in the mobile organization budget.

Where Mobile Banking App Development Is Heading

Three signals shape the next five years.

The first is the consolidation of the mobile platform layer. Internal mobile platforms at US banks now provide shared infrastructure for authentication, navigation, design system components, observability, and experimentation. Product teams build on top of the platform rather than reinventing it. The investment in the platform has paid off in faster product development cycles.

The second is on device intelligence. Apple and Google have moved more machine learning capability onto the device, and US banks have started using it for fraud signals, document capture, and personalization. The privacy implications of on device inference, where customer data does not leave the phone, are a meaningful selling point in a privacy aware US market.

The third is the slow but visible shift toward what the industry calls super app behaviours. US banks have not built true super apps, and probably will not, but the consumer expectation that a mobile bank app should also handle bill management, subscription tracking, identity wallet functions, and small business banking has reshaped the roadmap inside every large US institution.

For US bank technology executives, the practical question is no longer how big to make the mobile team. It is how to manage the dependency on Apple and Google, how to keep the engineering productivity high as the codebase grows, and how to invest in the next generation of mobile capabilities without losing the table stakes that customers already expect.

A fourth signal is the slow rise of progressive web app and instant app patterns for low risk surfaces. US banks have started using these patterns for marketing pages, calculators, and shareable artefacts, where the friction of an app install is too high but the experience needs to be richer than a static page.

The thin window onto the bank’s systems has become the bank itself for most US customers. That is a different product, run by different teams, measured by different metrics, and funded at a different scale. Mobile banking app development is now the most visible piece of US bank technology, and the choices being made inside those teams will shape how the next decade of US consumer banking actually feels in the hand. For founders selling tools into the US mobile banking stack, the practical implication is that the buyer is no longer a side project lead. It is a senior product engineering executive with a real budget and an exacting bar.