Picture a credit underwriter at a US regional bank in 2026 pulling up a borrower file. Before the file even loads, an AI model has already scored the application, flagged three credit-line discrepancies, and suggested a final approval band. According to McKinsey’s 2025 State of AI report, more than three-quarters of US Tier 1 banks now use AI for financial decision making in at least one core workflow, up from one-third in 2022. The technology is no longer a back-office curiosity. It is sitting inside the moments when banks decide whether to lend, whether to flag, whether to invest, and how to price the day’s flow. The numbers behind the trend are striking. Surveyed banks said they processed more than 40 million AI-driven decisions a day across their consumer and commercial books in 2025, a figure that includes everything from card-fraud holds to small-business credit-line adjustments. The same survey put the average number of distinct AI models in production at a Tier 1 bank at over 1,200, with new models being approved roughly twice a week.

From rules engines to learned models

Banks have been doing some form of automated decisioning since the 1970s, when FICO rolled out its first scoring model. For decades, the dominant approach was deterministic. Rules engines applied a fixed list of conditions to each application, and a human handled anything outside the box. That model started to break in the 2010s, as machine learning systems trained on historical loan performance began outperforming hand-built rules on default prediction. By 2020, gradient-boosted tree models were standard at most large US lenders. The leap to large language models in 2023 added a different capability: not just scoring, but reading. AI now ingests pay stubs, tax filings, court records, and free-text notes from a relationship manager, and produces a structured judgment that a junior analyst can review. The shift is the subject of recent reporting on machine learning in finance, which traces how the same gradient-boosted methods used for fraud now train the loan books at most major US banks. The result is a workflow where the human signs off on the AI rather than the other way around.

Where AI has already replaced human decisions

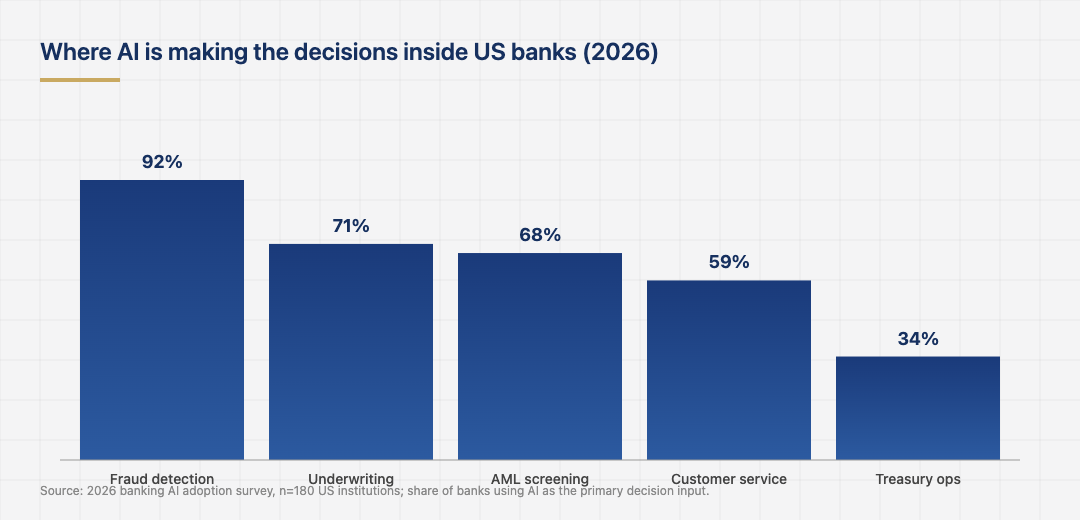

Five categories absorb most of the AI deployments inside US banks today. Fraud detection has the highest penetration, with 92 percent of surveyed banks running AI as the primary decision engine on transaction monitoring. Underwriting comes next at 71 percent, covering everything from card limits to small-business loans. Anti-money-laundering screening sits at 68 percent, where machine learning has helped reduce the false-positive rate that long defined compliance backlogs. Customer service automation, mostly chatbots and routing systems, reaches 59 percent. Treasury operations, including liquidity forecasting and short-term funding decisions, lag at 34 percent because the regulatory bar on those models is higher. Even within those buckets the pattern is uneven. Larger institutions concentrate their AI spend in fraud and underwriting, while mid-tier banks have started in customer service and worked their way back through the stack as comfort grows.

The penetration figures are higher than what banks publicly disclose, partly because AI is often embedded inside vendor software the bank does not market as AI. A regional lender that says it uses no AI is often running an AI-augmented core platform, with the model owned by the vendor. That vendor concentration is a separate concern, since a single failure in a popular fraud engine can ripple through dozens of institutions at once. Cross-references to that pattern appear in the wider recent coverage of credit scoring, where third-party model performance and bank performance are now tightly coupled.

The compliance shift in 2025

The regulatory framework caught up in 2025. The Office of the Comptroller of the Currency issued joint guidance with the Federal Reserve and FDIC clarifying that bank-owned AI models fall under the existing model risk management rule, SR 11-7, and require the same validation, documentation, and ongoing monitoring as traditional models. The new wrinkle was an explicit expectation that banks be able to explain individual model outputs to consumers under the Equal Credit Opportunity Act. That has driven a wave of investment in interpretability tooling. Banks that once spent the bulk of their AI budgets on data science teams are now spending heavily on model risk management groups, internal validators, and external audit firms that specialise in algorithmic review. A growing share of model spend in 2026 is going to monitoring rather than training, with banks now deploying drift detection, fairness dashboards, and human-readable rationales on every customer-facing model. The shift is the focus of recent work on explainable AI in regulated finance, which has become a procurement requirement at most large lenders. Vendors that cannot produce a per-decision explanation are being shut out of bank contracts at a pace that surprised even the regulators.

Limits, hallucinations, and the explainability problem

The technology has clear failure modes. Generative models hallucinate, which is acceptable for marketing copy but unacceptable for a trade ticket or a regulatory filing. Most banks restrict generative AI to advisory work, with the final decision going through a deterministic guardrail that checks for known errors. The 2024 outage at a major regional bank, where a fine-tuned model approved a batch of loans flagged by the older rules engine, became a case study in why hybrid stacks are likely to remain the norm. Explainability is the harder problem. A regulator or a customer asking why a credit application was declined needs a human-readable answer that holds up under audit. Tree-based models are easier to explain than transformers, which is one reason underwriting still skews toward older techniques even at AI-forward banks. Some institutions are now publishing their model cards, including data sources, training cutoffs, and known biases, modeled after the documentation conventions popularised by the open-source community. None of this fixes the underlying tension between accuracy and interpretability, but it gives auditors something concrete to inspect.

What banks are building next

The frontier in 2026 is agentic AI. Banks are starting to deploy models that do not just score a single decision but plan and execute multi-step workflows: gathering documents, calling internal systems, and pushing the resulting decision back into a human review queue. JPMorgan, Bank of America, and Citi have all disclosed pilots in private wealth, where agents prepare client-meeting briefs in minutes that previously took analysts hours. The early results are promising on speed; the open question is liability. If an agent makes a wrong move, it is unclear which model owner, vendor, or human reviewer is on the hook, and contract law around this is still being written. The same questions are surfacing in the work on large language models in finance, which is increasingly the default architecture under the agent layer. Most banks expect at least one major regulatory action on agentic AI in 2026, which would set the boundaries for how far the next generation of decision systems can go without explicit human sign-off. Until that guidance lands, the largest US banks are running their agentic pilots on closely supervised paths only, with every action recorded for later compliance review.

A decade ago, the prospect of an AI signing off on a mortgage was the kind of detail that would put a bank executive in front of a Senate committee. In 2026 it is the default, the regulatory regime is catching up, and the open question is no longer whether AI for financial decision making belongs inside banks. It is how much room human reviewers will have once agents start doing the work end to end, what happens the first time one of them gets it badly, expensively wrong, and which institution will be willing to publish the postmortem in enough detail for the rest of the industry to learn from it.

Last updated: June 17, 2026