Reinforcement learning for trading is a topic that attracts more pitch decks than production deployments. The technique has clear theoretical appeal: an agent that learns trading policies through interaction with the market, optimising for cumulative reward over a sequence of decisions. The reality of applying it to U.S. financial markets is more constrained, more expensive, and more often disappointing than the marketing material suggests. The institutions that use reinforcement learning productively for trading have a small set of disciplines that distinguish them from the institutions that produce strong backtests and weak production results.

This piece looks at where reinforcement learning genuinely belongs in U.S. financial trading, the disciplines that distinguish productive deployments from sprawling experiments, the failure modes that distinguish theory from practice, and the operational realities that determine whether reinforcement learning capabilities pay back their cost.

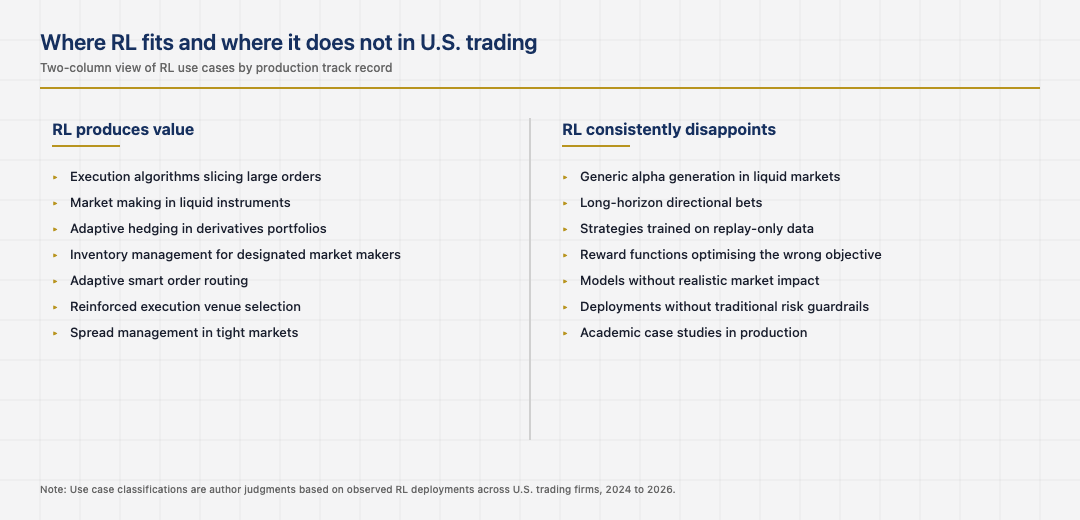

Two columns of where RL works and where it does not

The cleanest way to think about reinforcement learning in U.S. financial trading is as two columns: where it produces value and where it consistently disappoints. The where-it-works column includes execution algorithms that decide how to slice large orders across time and venues, market making in liquid instruments where the agent learns inventory and spread management, and adaptive hedging strategies in derivatives portfolios. Each of these has tractable state spaces, clear reward signals on tractable time horizons, and rich enough simulation environments to make training feasible.

The where-it-disappoints column includes generic alpha-generating strategies in liquid markets, attempts to learn long-horizon directional bets, and most of the academic-paper case studies that look strong on historical data and underperform when deployed against live markets. The institutions that respect this division build productive RL programs. The institutions that ignore the division usually have a portfolio of impressive backtests and disappointing production performance, with the disappointment usually attributed to anything except the original choice to apply RL where it did not fit.

The simulation environment and the gap to live markets

The biggest single challenge in RL for trading is the simulation environment. Training requires interacting with a market that responds to the agent’s actions, and historical data does not respond to actions. The institutions that built sophisticated simulation environments, with realistic market impact models, queue dynamics, and counterparty behaviour, train agents that perform meaningfully in production. The institutions that trained against historical replay without market response usually have agents whose backtested performance does not survive contact with live markets.

The investment in simulation environment is significant. Building one that approximates the actual market response well enough to support useful training takes years of effort and continuous refinement. The institutions that paid the cost early are now extracting it across every RL strategy they develop. The institutions that did not are still delivering strategies that look strong in backtests and fall apart in production.

Reward design and the operational consequence

Reward design is where RL practitioners spend the most time and where the most consequential mistakes happen. A reward function that captures the wrong thing produces an agent that optimises the wrong objective, sometimes in surprising ways. The mature pattern in U.S. trading RL is treating reward design as iterative, with extensive testing of how the agent behaves under different reward formulations and explicit handling of edge cases that simpler reward functions would optimise toward in undesirable ways.

The institutions that take reward design seriously produce agents whose behaviour matches the strategic intent. The institutions that treat reward design as a final-step formality usually find their agents producing technically high reward and operationally problematic outcomes, which is where the regulatory and risk-management questions tend to focus.

Risk management and the supervisory perimeter

Reinforcement learning agents that trade need risk management that supervisors can evaluate. Position limits, drawdown thresholds, and clear escalation triggers are all necessary regardless of the underlying technique. The institutions that built these guardrails into their RL deployments satisfy supervisory expectations. The institutions that treated RL as exempt from traditional trading risk management usually find their deployments restricted under regulatory pressure.

The supervisory expectation around algorithmic trading in U.S. markets has hardened over the past decade. The Federal Reserve and the SEC have both spoken to the need for clear governance, testing, and monitoring of algorithmic strategies. The institutions that internalised these expectations early extended them to RL deployments naturally. The institutions that did not are now retrofitting the expectations under regulatory pressure on someone else’s timeline.

The next phase of RL in U.S. trading

The next phase is shaped by the integration of foundation models with RL pipelines, the maturation of simulation environments, and the continuing tightening of supervisory expectations around algorithmic trading. The institutions that built strong RL foundations in execution, market making, and adaptive hedging will absorb the changes cleanly. The institutions still chasing the alpha-generation use case will continue to face the structural challenges that have made that use case difficult since the early days of the technique.

Read across the full picture, reinforcement learning for U.S. financial trading in 2026 is a productive technique in specific categories with specific disciplines. Realistic simulation environments, careful reward design, integrated risk management, and honest selection of use cases are the patterns that compound. The institutions that respect them deliver real trading capability. The institutions that miss any one usually deliver impressive backtests and disappointing production results.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.