AI for financial decision making in U.S. finance has moved past the demo stage and into the operational stage. The institutions deploying AI in production are now answering harder questions than whether the technology works. They are answering questions about model risk management, supervisory expectations, the explainability burden, and the integration of AI decisions into existing approval and audit workflows. The institutions that are answering these questions cleanly are pulling ahead. The institutions still treating AI as an experimental capability are quietly falling behind.

This piece looks at where AI for financial decision making has settled in U.S. finance, the categories where AI is genuinely productive, the categories where it is a distraction, the supervisory environment that is shaping deployment, and the disciplines that distinguish operationally mature AI programs from the demo-driven ones.

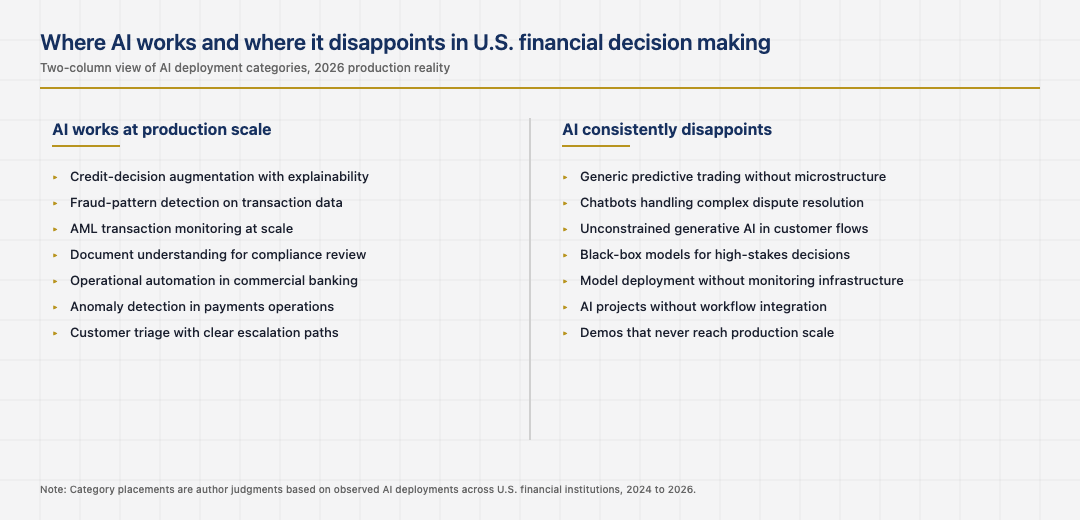

Two columns of where AI actually works

The cleanest way to think about AI in U.S. financial decision making is as two columns: where it produces real value at production scale, and where it consistently disappoints. The where-it-works column includes credit-decision augmentation, fraud-pattern detection, AML transaction monitoring, document understanding for compliance, and operational automation in commercial banking workflows. Each of these has clear ground truth, dense data, and a measurable cost-benefit calculation that AI can improve.

The where-it-disappoints column includes generic predictive trading models that ignore market microstructure, customer-facing chatbots that try to handle complex disputes without escalation, and unconstrained generative AI deployed where deterministic rules would be safer. The institutions that respect this division build AI programs that produce real value. The institutions that ignore the division usually have a portfolio of AI projects with mixed results, where the failures dilute the credit the successes deserve.

Model risk management as the binding constraint

Model risk management is the binding constraint on AI deployment in U.S. finance. The Federal Reserve’s SR 11-7 guidance on model risk management was published in 2011 and continues to define the supervisory expectation. AI models, regardless of their technical novelty, are subject to the same model risk management discipline as traditional statistical models: independent validation, ongoing monitoring, documentation of intended use, and clear governance of model changes.

The institutions that built model risk management infrastructure that scales to AI deploy AI faster than the institutions that did not. The cost of building the infrastructure is real and front-loaded. The benefit accumulates across every model the institution deploys. The institutions that treated model risk management as a check-the-box compliance exercise usually find that their first AI model exposes the gaps in the program, often in supervisory exams.

Explainability and the supervisory expectation

Explainability has become the most contested topic in financial AI. Supervisors expect models that affect customers to be explainable. Many AI models, particularly large neural networks and ensemble methods, are not explainable in the same sense as traditional statistical models. The institutions that built explainability tooling, including SHAP-based attribution, surrogate models, and structured rationale generation, satisfy the supervisory expectation while still using modern AI techniques. The institutions that did not build explainability tooling usually find themselves restricted to simpler models that the supervisory environment will accept without specific evidence of explainability.

The institutions that took explainability seriously also produce better internal model behaviour, since explainability tooling exposes biases and edge-case behaviour that black-box deployment would have hidden. The discipline pays back twice: once in supervisory defensibility and once in model quality. The institutions that treated explainability as an external constraint rather than an internal benefit usually deliver weaker models alongside their weaker supervisory position.

Operational integration and the workflow question

The fourth challenge is operational integration. An AI model that produces a recommendation is not useful unless the recommendation reaches the human who needs to act on it, in the system where they do their work, with the context they need to act on it confidently. The institutions that built strong workflow integration around their AI models capture the operational benefit. The institutions that built strong models without the workflow integration usually find that the models are technically successful but operationally underused.

The discipline of workflow integration is unglamorous and expensive. It requires understanding the existing operational processes, the existing tools used by frontline staff, and the existing approval workflows. The institutions that invest in this discipline alongside their model development capture the value. The institutions that defer the integration work usually deliver model demos to executives and very little operational change to the actual business.

The next phase of AI for financial decision making

The next phase is shaped by the maturation of large language models for specific financial tasks, the integration of vector databases into model serving infrastructure, and the continued tightening of supervisory expectations around model deployment. The institutions that built strong foundations in model risk management, explainability, and workflow integration will absorb these changes cleanly. The institutions that have not will find each new capability harder to integrate.

Read across the full picture, AI for financial decision making in U.S. finance in 2026 is a settled operational discipline with specific patterns that distinguish productive programs from disappointing ones. Respecting where AI fits and where it does not, building strong model risk management, taking explainability seriously, and investing in workflow integration are the patterns that compound. The institutions that respect them deliver real operational benefit. The institutions that miss any one usually have AI programs that produce demos rather than business outcomes.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.