DevOps in FinTech is rarely the discipline the marketing decks describe. The standard pitch features continuous deployment, full automation, and confident cultural transformation. The reality inside U.S. financial firms is more constrained. Change windows still exist. Supervisory expectations require evidence trails. Production deploys touch systems that move money and that supervisors care about. The teams that work effectively in this environment have figured out how to capture the speed benefits of modern DevOps without losing the discipline that the regulatory environment requires.

This piece looks at where DevOps practice in U.S. FinTech has actually settled in 2026, the patterns that work inside regulated environments, the cultural traps that defeat teams who borrow practices wholesale from non-regulated tech, and what mature programs look like at scale.

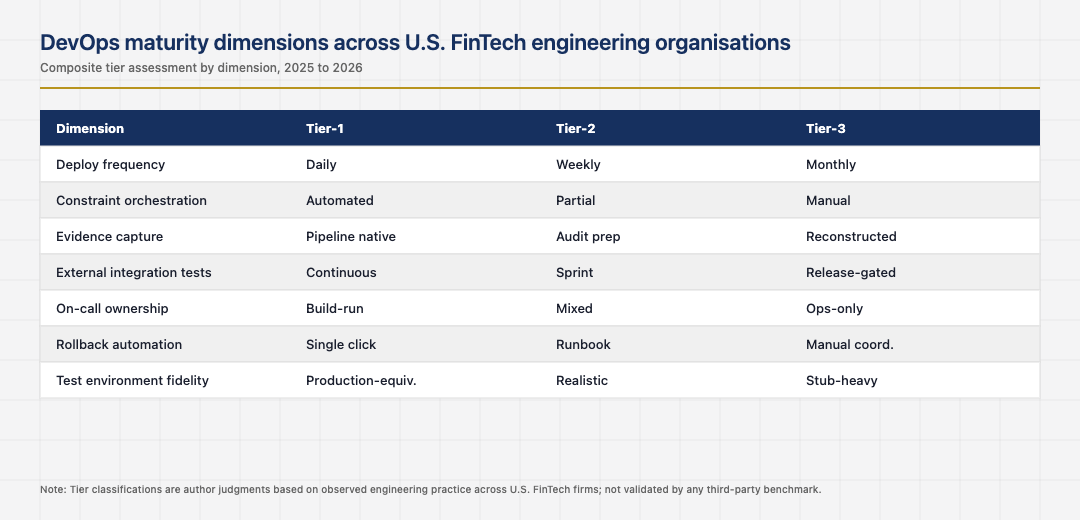

Continuous deployment without continuous risk

The first hard reset for DevOps in finance is recognising that not every change can be safely deployed at any time. Posting engines have settlement windows. Card processors have peak-hour caps. Sponsorship-bank partnerships sometimes require pre-deployment notification. Treating these constraints as obstacles to deployment automation usually means working around them through manual processes that defeat the automation’s value. Treating them as first-class inputs to deployment orchestration produces a deployment system that respects them automatically.

The mature pattern is automated deployment that knows about the constraints, schedules around them, and gates itself when conditions are not met. The teams that work this way deploy frequently in safe windows and quietly during constrained windows. The teams that ignore the constraints either deploy unsafely or do not deploy frequently. The middle path, where the deployment system itself enforces the constraints, is where the most successful U.S. FinTech engineering teams have landed.

Evidence trails as a deployment requirement

U.S. financial supervisors expect to see evidence of how a change was tested, who approved it, and what the rollback plan was. Generating that evidence after the fact is expensive and unreliable. Generating it as a side effect of the deployment pipeline is cheap and reliable. The teams who design the pipeline to produce supervisory-grade evidence as a standard output find their next exam considerably easier. The teams who treat evidence as an audit-prep activity find their exam considerably harder.

The pattern that works is automated capture of every step in the pipeline, persisted in a tamper-evident store, with clear linkage between the change, the approvals, the test results, and the deployment events. The pattern that does not work is logs that are sufficient for engineering troubleshooting but not structured for supervisory consumption. The cost difference between the two patterns shows up every time a regulator asks how a change was made.

Test discipline as the alternative to caution

The DevOps mindset that high-quality automated testing is the alternative to manual gating works as well in finance as anywhere else, with one caveat: the test pyramid in finance includes integration testing against external systems that the team does not control. Card networks, payment rails, sponsorship-bank APIs, and regulatory data submissions all introduce external dependencies that need realistic test environments.

The teams that succeed here invest in sandbox environments and synthetic transaction frameworks for every external dependency. The teams that try to substitute manual gating for that investment usually underperform on both speed and quality. The investment is significant. It also pays back many times over across the lifetime of the platform, and the U.S. operators who built it early are running circles around the ones who deferred it.

Cultural traps from borrowed practices

Several DevOps practices that work well in non-regulated tech translate poorly to finance without modification. Blameless postmortems work, but the supervisory environment may require attribution of root cause that goes beyond the engineering team’s preferred internal framing. You-build-it-you-run-it works, but the on-call expectations may collide with regulatory requirements about who can access production data and under what conditions. Continuous deployment of database schema changes works in many systems, but rarely in core banking ones.

The U.S. FinTech engineering leaders who navigate these tradeoffs well usually adapt the practices rather than adopting them wholesale. They keep the underlying intent of modern DevOps, accelerate the change cycle, increase deployment confidence, and reduce manual coordination cost while modifying the implementation to fit the regulatory and operational environment they actually live in. The leaders who try to import the practices unmodified usually find themselves either operating outside the supervisory expectation or being slowed down by friction that the practice was supposed to remove.

What mature programs look like at scale

The mature U.S. FinTech DevOps program at scale shares a small set of properties. Deployments are frequent and automated, with constraints encoded in the orchestration layer rather than enforced manually. Evidence is produced continuously and is supervisory-grade by default. Test discipline includes external dependencies and runs against production-equivalent environments. Cultural practices are adapted to fit the regulatory environment without losing the underlying intent. On-call rotations are aligned with both engineering ownership and supervisory access expectations.

None of this is exotic, but every element of it requires discipline to maintain. The U.S. FinTech operators who treat DevOps as the operational layer of their financial system rather than as a separate engineering practice produce more reliable systems, recover more quickly from incidents, and pass exams more cleanly. The ones who keep DevOps in a separate organisational silo from the financial-product teams continue to struggle, and the gap between the two patterns has grown wide enough that it now visibly differentiates the strongest U.S. FinTech engineering organisations from the weaker ones.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.