The US financial system is held up by four overlapping pillars: chartered commercial banks, credit unions, securities broker-dealers, and the federal regulator constellation that governs all of them. Reading the size, shape, and recent trajectory of each pillar is the most reliable way to understand where systemic strength sits, where consolidation pressure is most active, and where new entrants can realistically expect to compete.

The numbers across the four pillars tell a consistent story. Banks and credit unions are slowly consolidating into fewer, larger institutions while serving roughly the same total population. Broker-dealers are stable in number but increasingly concentrated by assets. The regulator constellation has expanded its reach without meaningfully simplifying its structure. The article that follows reads each pillar against its 2025 numbers and pulls out what founders, policy thinkers, and incumbent operators should take from the underlying patterns.

What makes the institutional landscape worth reading carefully is that the structural shape determines what new product strategies can actually scale. A fintech with a brilliant retail banking experience still has to plug into one of the existing pillars to clear payments, custody assets, or hold deposits, and the shape of that landscape sets the realistic ceiling on which strategies work and which never reach commercial scale.

The shape of the US financial institution landscape

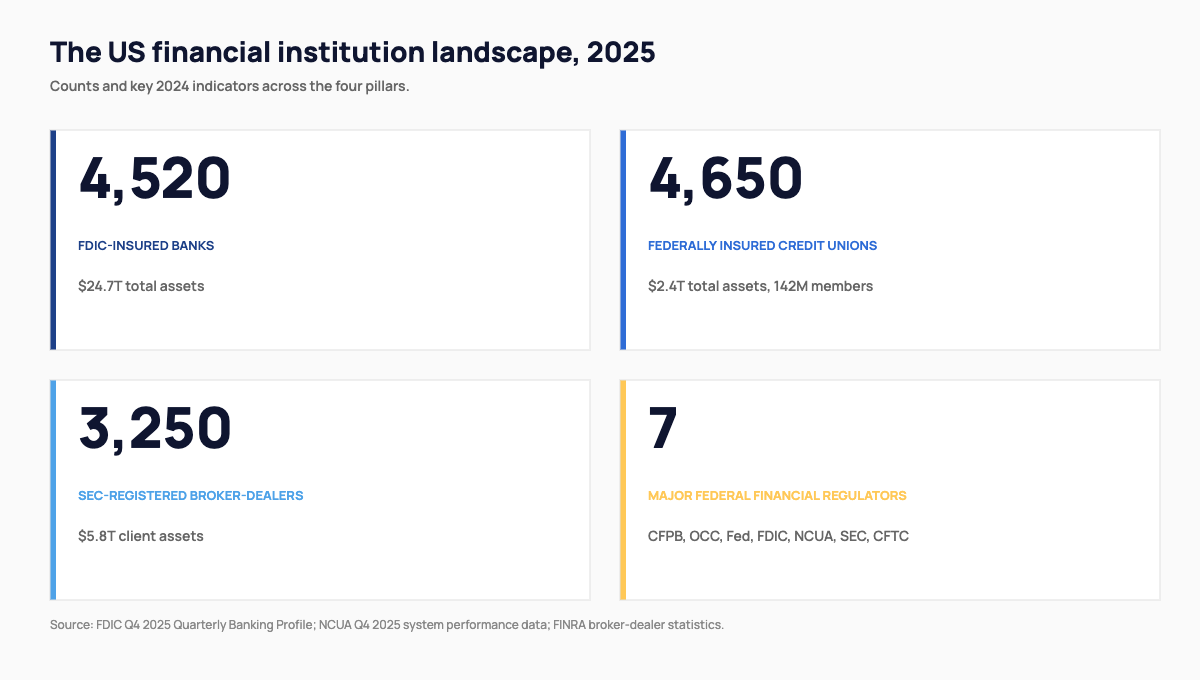

At the end of 2025, the US had approximately 4,470 FDIC-insured commercial banks at the most recent quarterly release, approximately 4,500 federally insured credit unions per NCUA, and approximately 3,300 SEC-registered broker-dealers per FINRA. Together those institutions held more than $30 trillion in total assets and served essentially the entire US adult population in some form. The headline counts hide significant concentration. The top 10 US banks hold roughly two-thirds of total bank assets. The top 50 credit unions hold roughly one-third of total credit-union assets. The top 25 broker-dealers manage the majority of broker-dealer client assets. That concentration is consistent across pillars and is one of the central features of the modern US financial system.

Below the largest institutions sits a long tail of community banks, regional credit unions, and smaller broker-dealers that collectively serve geographies, customer segments, or product niches the largest institutions do not prioritise. That long tail has been thinning for forty years through M&A activity and operational pressure, and the rate of thinning has accelerated since 2008. The smallest community banks and credit unions face technology, compliance, and talent costs that are functionally fixed, which makes consolidation the dominant economic option for institutions below a certain scale threshold.

What the FDIC and NCUA 2025 numbers show

The FDIC’s Q4 2025 Quarterly Banking Profile reports total bank assets of $24.7 trillion, total deposits of $19.8 trillion, and net income of roughly $290 billion for the year. Loan growth ran at about 4 percent for the year, deposit growth at about 3 percent, and the industry-wide net interest margin held steady at around 3.2 percent. Those are healthy numbers by historical standards but compressed compared with the 2018-2022 cycle, reflecting the higher interest-rate environment and the deposit competition that has come with it.

The NCUA’s Q4 2025 release shows credit unions held about $2.4 trillion in assets and served roughly 142 million members at year-end. Credit union loan growth ran at 5 percent for the year, slightly outpacing banks, and net income reached approximately $18 billion. Membership grew at about 2 percent, in line with the long-term trend. Credit unions continue to maintain their structural advantage on consumer deposit pricing and member-relationship economics, but they face the same technology and compliance cost pressures that are reshaping the bank pillar.

Combined, banks and credit unions hold around $27 trillion in assets and serve effectively the entire US adult population. The most-watched metric across both is the cost of compliance and core technology relative to asset base, which is what determines whether a smaller institution can remain independent or whether merger becomes the dominant economic option. That cost ratio has been climbing steadily for the past decade, and the implication is that the bottom of the long tail will continue to thin through forced consolidation rather than orderly retirement.

The regulator constellation, and the broker-dealer numbers

The US has seven major federal financial regulators (CFPB, OCC, Federal Reserve, FDIC, NCUA, SEC, and CFTC), plus state-level banking, insurance, and securities regulators in every state. That constellation is dense by international standards. The UK, by comparison, runs most of the same supervisory functions through two regulators (FCA and PRA). The dense US structure produces overlapping mandates and occasional jurisdictional friction, but it also creates redundancy that arguably contributes to systemic resilience. The conversation about whether to consolidate the constellation has been ongoing for thirty years and is unlikely to resolve soon.

The 3,250 SEC-registered broker-dealers manage approximately $5.8 trillion in client assets and produced revenue of roughly $470 billion in 2024. Like the bank pillar, the broker-dealer pillar is concentrated. The top 25 firms account for the majority of revenue and client assets, while the long tail of smaller broker-dealers serves regional, retail, or specialty-product niches. The number of broker-dealers has shrunk by roughly 25 percent since 2010, reflecting the same operational and compliance cost pressures that drive bank and credit union consolidation. The capital-markets fintech wave has produced new entrants in selected niches (zero-commission retail, alternative-asset brokerage, digital-native institutional platforms), but the overall directional trend is consolidation rather than fragmentation.

Why consolidation has been the dominant trend for forty years

The US had roughly 14,000 commercial banks in 1985. Today it has about 4,500. The reduction did not come from systemic failure on any meaningful scale; it came from steady M&A activity driven by the economics of scale in financial services. Three structural drivers keep that consolidation engine running. The first is technology cost. Core banking systems, compliance platforms, and cybersecurity infrastructure all carry roughly fixed costs that smaller institutions cannot amortise efficiently. The second is regulatory cost. Each new regulation adds compliance overhead that hits all institutions roughly equally in absolute terms but disproportionately in relative terms.

The third driver is talent. Smaller institutions cannot compete with larger ones for engineering, risk-management, and senior leadership talent at current compensation levels, which means they accumulate operational deficits over time that eventually force consolidation. Those three drivers have been reinforcing each other for forty years and show no sign of weakening, so the directional consolidation trend will continue. The interesting policy question is at what scale that consolidation becomes destabilising for community banking access, particularly in rural and underserved geographies, and the CFPB and FDIC are both watching that question carefully.

What founders and policy thinkers should take from the data

For founders, the practical lesson is that the institutional landscape is consolidating, which creates both opportunity and constraint. Opportunity, because consolidating institutions accumulate technology debt and compliance gaps that fintechs can address through partnership or product. Constraint, because the surviving institutions are larger, slower, and more procurement-driven than the institutions of a decade ago, which raises the bar for what fintech operators need to deliver to win serious distribution. The strategic question is which segment of the institutional landscape your product actually fits, and whether the consolidation pressure works for or against your commercial timing.

For policy thinkers, the lesson is that the US financial system’s structural shape (concentrated at the top, long-tail at the bottom, dense regulator constellation overlaying both) is unlikely to change quickly. Policy interventions that assume rapid restructuring tend to underperform, while interventions that work with the existing concentration and consolidation gradient tend to land. Open innovation patterns across US finance are increasingly the channel through which institutional innovation actually reaches consumers and businesses, and policy thinking that engages with that channel directly is more likely to produce durable improvements than top-down restructuring proposals that ignore it.