Crypto has evolved from a speculative asset class into a capital management tool. In 2026, many holders seek ways to make their crypto savings productive.

A crypto savings account addresses that directly. It allows users to earn interest on crypto without trading, staking, or locking assets for fixed periods.

This article explains how crypto savings accounts work, how yield is generated, what risks exist, and which platforms offer most convenient solutions without lock-ups or staking.

What Is a Crypto Savings Account

A crypto savings account is a service that lets users deposit digital assets—such as BTC, ETH, USDT, or USDC—and earn yield over time.

Mechanically, it functions similarly to a traditional bank savings account:

- You deposit funds

- The platform deploys those funds

- You receive interest

The key difference lies in how yield is generated and how flexible access to funds can be.

Modern crypto savings accounts fall into two broad categories: flexible savings and fixed-term savings. The choice depends on a particular strategy, but the volatile nature of the crypto market prompts many users to prioritize liquidity over maximum yield.

How You Earn Interest on Crypto

Crypto yield is not created out of thin air. It comes from underlying financial activity within the crypto ecosystem.

The main sources include:

- Lending markets

Platforms lend deposited assets to borrowers (traders, institutions, or retail users). Borrowers pay interest, which is shared with depositors. - Market-making and liquidity provision

Assets are used to provide liquidity on exchanges, generating fees. - Arbitrage and structured strategies

Some platforms deploy capital across markets to capture pricing inefficiencies.

In practice, users do not interact with these mechanisms directly. The platform abstracts complexity and offers a simple “earn interest” interface.

Fixed vs Flexible Crypto Savings Accounts

This is the core structural difference that defines user experience.

Fixed Savings

- Funds are locked for a defined period (e.g., 1–12 months)

- Higher advertised rates

- No access during the term

This model suits long-term holders who do not need liquidity.

Flexible Savings

- Funds can be withdrawn anytime

- Interest accrues continuously

- No lock-ups or staking requirements

This model prioritizes usability and capital efficiency.

Clapp.finance illustrates the distinction clearly:

- Flexible savings offer daily interest, instant withdrawals, and no lock-up requirements

- Fixed savings provide higher rates in exchange for commitment periods

Flexible accounts are increasingly aligned with how users actually manage capital—keeping optionality while still earning yield.

Why Flexible Yield Is Gaining Ground

Earlier crypto cycles rewarded aggressive yield strategies, but now users evaluate three variables: liquidity, transparency, and consistency. Flexible savings products address all three, as funds remain accessible, rates are clearly defined, and interest accrues daily.

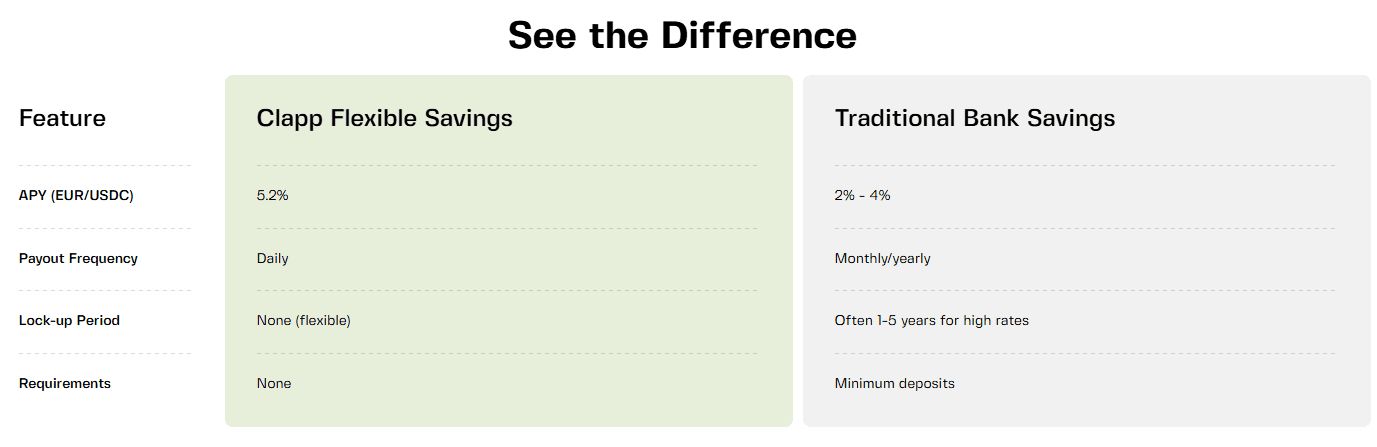

For example, Clapp Flexible Savings provides:

- Up to 5.2% APY on stablecoins

- Daily compounding payouts

- Instant deposits and withdrawals with no lock-ups

The result is closer to a liquid yield account than a traditional “earn product.”

Clapp Offers Liquid Yield Without Friction

Clapp’s savings model is built around a simple premise: yield should not compromise access to capital.

Its flexible savings product offers:

- No lock-ups

- No staking

- No token requirements

- Daily interest payouts

- Instant liquidity

Funds remain fully accessible at all times, while still generating yield. At the same time, users who want higher returns can opt into fixed terms with predictable rates. This dual structure allows users to choose between liquidity (flexible savings) and maximum yield (fixed savings) without being forced into either.

Risks of Crypto Savings Accounts

Yield always comes with trade-offs. Understanding them is critical.

1. Counterparty Risk

You rely on the platform to manage funds properly. Poor risk management can lead to losses.

2. Market Risk

If funds are deployed in volatile strategies, returns can fluctuate.

3. Liquidity Risk (for fixed products)

Locked funds cannot be accessed during market stress.

4. Rate Variability

Some platforms advertise “up to” yields that depend on tiers or conditions. Transparent models where rates are fixed or clearly defined without tiers reduce uncertainty.

Final Take

Crypto savings accounts have moved beyond experimental yield products. They now compete directly with traditional savings accounts, and the difference lies in efficiency.

Platforms that align current users’ preferences such as daily interest, instant access and no lock-ups are likely to define the next phase of crypto savings. Clapp fits squarely into this shift, focusing on flexibility as the primary value driver rather than headline rates.