How Australia Built One of the World’s Most Active Real-Time Payment Networks

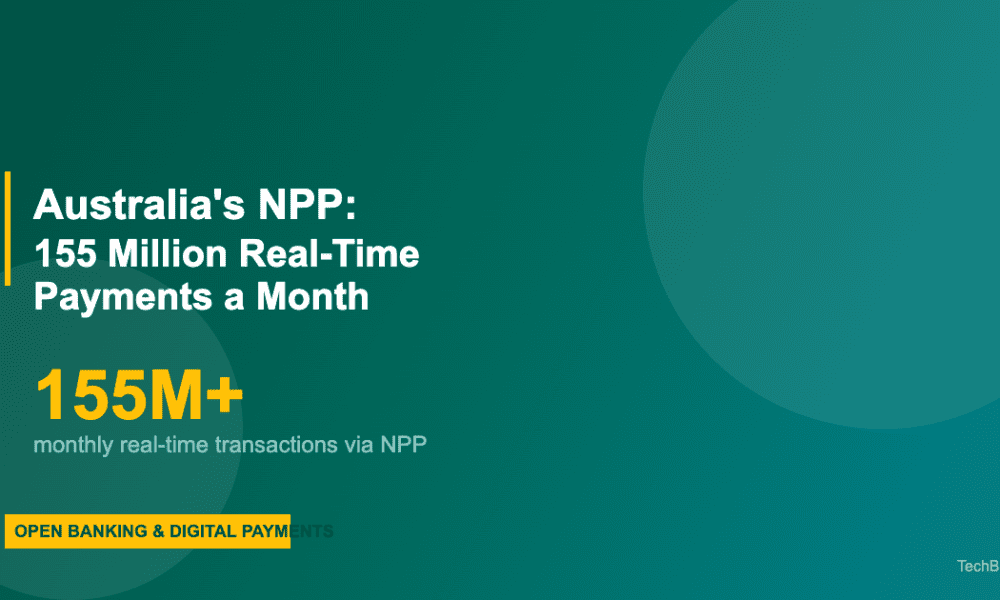

Australia’s New Payments Platform, known as the NPP, has reached a milestone that places it among the most active real-time payment infrastructures globally. The platform now processes more than 155 million real-time payments every month, a figure that reflects both the system’s technical maturity and the Australian public’s rapid embrace of instant digital transfers. Since its launch in February 2018, the NPP has fundamentally altered how money moves between individuals, businesses, and institutions across the country.

Built as a collaborative effort between major Australian financial institutions and the Reserve Bank of Australia, the NPP was designed to provide a modern, fast, and data-rich alternative to the legacy batch-processing systems that had underpinned Australian payments for decades. Seven years later, the platform has exceeded initial adoption projections and continues to grow as new use cases and overlay services expand its reach.

The Scale of NPP Adoption

The 155 million monthly transaction figure represents a dramatic increase from the NPP’s early days. In its first full year of operation, monthly volumes hovered around 15 to 20 million transactions. Growth has been driven by a combination of factors, including expanding institutional participation, consumer familiarity with the PayID addressing system, and the integration of NPP rails into mobile banking applications offered by all major Australian banks.

For more coverage on related topics, explore our dedicated section on fintech developments.

The Boston Consulting Group projects fintech revenues will reach $1.5 trillion by 2030, with embedded finance and digital lending accounting for the largest share of projected growth.

According to CB Insights’ 2024 fintech report, global fintech funding declined 40 percent between 2022 and 2024, pushing the sector toward consolidation and a sharper focus on profitability over growth at all costs.

Readers interested in this space may also find value in our reporting on digital payments.

PayID, the NPP’s user-friendly addressing service that allows payments to be sent using a mobile phone number, email address, or ABN rather than a BSB and account number, has been central to driving consumer adoption. More than 16 million PayIDs have been registered across Australian financial institutions, covering a significant proportion of the adult population. The simplicity of the PayID experience has made real-time transfers the default method for person-to-person payments among younger demographics in particular.

Transaction values have also scaled substantially. While the NPP was initially perceived primarily as a retail and consumer payment channel, business-to-business and government payment volumes have grown steadily. The platform now handles a diverse mix of transaction types, from small peer-to-peer transfers to larger commercial payments, salary disbursements, and government benefit distributions.

Stay informed with TechBullion’s latest coverage of technology trends.

Technical Architecture and Performance

The NPP operates on a centralised basic infrastructure developed by SWIFT, which provides the real-time clearing and settlement backbone. Transactions settle individually in real time through the Reserve Bank of Australia’s Fast Settlement Service, which operates around the clock, 365 days a year. This architecture eliminates the settlement risk inherent in batch-based systems and ensures that funds are available to recipients within seconds of a payment being initiated.

The platform supports the ISO 20022 messaging standard, which allows significantly richer data to accompany each transaction compared to older payment formats. This capability is particularly valuable for business payments, where remittance information, invoice references, and structured data can travel alongside the payment itself, reducing reconciliation effort and enabling straight-through processing.

System reliability has been a defining characteristic. The NPP consistently maintains availability rates exceeding 99.9 per cent, a critical requirement for a payment system that operates continuously without maintenance windows. Peak transaction volumes, which typically occur during payroll processing periods and major online shopping events, are handled without degradation in processing speed.

Overlay Services Expanding Functionality

One of the NPP’s distinguishing architectural features is its overlay service model, which allows third-party services to be built on top of the basic infrastructure. The most widely used overlay service is Osko, operated by BPAY Group, which provides the consumer-facing real-time payment experience available through participating financial institutions’ banking apps.

The Mandated Payments Service represents a newer overlay that enables businesses to initiate payments from customer accounts with pre-authorised consent. This service supports use cases such as subscription billing, loan repayments, and utility payments, providing an alternative to direct debit that offers real-time confirmation and richer data capabilities.

The PayTo service, which launched in 2022 and continues to expand its institutional reach, allows merchants and billers to initiate real-time payments with customer pre-authorisation. PayTo is positioned as a modernised replacement for the ageing direct debit system, offering consumers greater visibility and control over recurring payments while giving businesses faster access to funds and reduced dishonour rates.

Competitive Position in the Global Real-Time Payments Landscape

Australia’s NPP sits within a global wave of real-time payment infrastructure development, but its per capita transaction volumes place it among the leading systems worldwide. India’s UPI processes vastly higher absolute volumes, exceeding 14 billion transactions per month, but operates across a population roughly 50 times larger. On a per capita basis, Australia’s 155 million monthly transactions across a population of approximately 27 million represent a penetration rate that ranks alongside the most advanced real-time payment markets globally.

Compared to the United States, where the FedNow service launched in July 2023 and is still building institutional participation, Australia benefits from a seven-year head start and near-universal bank connectivity. The United Kingdom’s Faster Payments Service, launched in 2008, processes comparable per capita volumes but operates on older technology that lacks the rich data capabilities of the NPP’s ISO 20022 foundation.

Challenges and Future Development

Despite its success, the NPP faces several ongoing challenges. The expansion of PayTo adoption among merchants and billers has been slower than initially projected, partly due to the technical integration effort required and partly due to competing payment methods that merchants are already comfortable with. Driving merchant-side adoption remains a priority for NPP Australia, the entity that manages the platform.

Cross-border payment connectivity represents the next major frontier. The NPP was designed primarily as a domestic system, but increasing demand for fast and transparent international transfers has prompted exploration of bilateral connections with real-time payment systems in other countries. Pilot programmes linking the NPP with systems in Southeast Asia and the broader Asia-Pacific region are under development.

The Reserve Bank of Australia has also signalled interest in exploring how a potential central bank digital currency could interact with or complement the existing NPP infrastructure. While a retail CBDC remains in the research phase, any future digital Australian dollar would likely need to integrate with the NPP rails to achieve meaningful adoption.

With 155 million monthly transactions and growing, the NPP has established itself as one of the world’s most successful real-time payment platforms. For payment technology providers, financial institutions, and businesses operating in the Australian market, the platform’s continued evolution presents both integration opportunities and competitive imperatives that will shape the country’s payment landscape for years to come.